July 30, 2014

July 30, 2014 (GDP Byte)

GDP grew at a 4.0 percent annual rate in the second quarter after shrinking at a 2.1 percent rate in the first quarter. Much of the shift was due to a considerably more rapid pace of inventory accumulation. Inventory changes, which had subtracted 1.16 percentage points from first quarter growth, added 1.66 percentage points to growth in the second quarter. New car sales added another 0.42 percentage points to growth, after adding just 0.13 percentage points in the first quarter.

Equipment investment, which grew at a 7.0 percent rate, added another 0.4 percentage points to growth for the quarter. Investment in structures rose at a 5.3 percent rate, while investment in intellectual property products increased at a 3.5 percent rate. After declining in the prior two quarters, residential investment rose at a 7.5 percent annual rate.

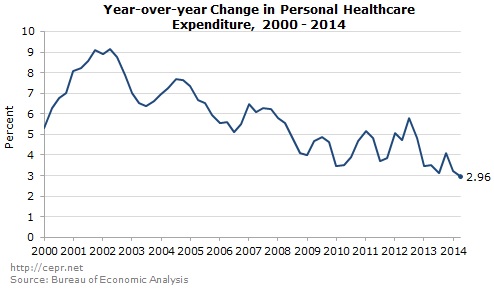

Another positive item in this report was continued slow growth in health care costs. After a reported drop in the first quarter, health care costs grew at a 2.6 percent annual rate. They stand just 3.0 percent above their year-ago level. While there were likely some errors in the data leading to a sharp reported rise in spending in the fourth quarter of 2013, followed by a nominal drop last quarter, taken together these numbers indicate there was no surge in spending associated with the implementation of Obamacare.

On the negative side, the trade deficit expanded again last quarter, rising to an annual rate of $564.0 billion, as imports grew at an 11.7 percent annual rate. The deficit subtracted 0.62 percentage points from growth in the quarter.

Government spending grew at a 1.6 percent rate, adding 0.3 percentage points to growth. A 3.1 percent rise in state and local spending more than offset a 0.8 percent rate of decline in federal spending. It is likely that the government sector will be a modest positive for growth for the next several years

The core personal consumption expenditure deflator hit 2.0 percent in the 2nd quarter. This is the first time it has been at or above the Fed’s 2.0 percent target since it was 2.1 percent in the first quarter of 2012. The overall GDP price index also increased at a 2.0 percent rate.

This report included annual revisions to prior years’ data. The revisions show a somewhat slower pace of growth for 2011 and 2012, with growth being revised down by an average 0.35 percentage points. Growth for 2013 was revised up slightly to 2.2 percent from 1.9 percent. This leaves average growth for the past three years at just 2.0 percent.

There were also modest upward revisions to national income in the last two years, primarily due to higher interest payments. The upward revision to income, coupled with the downward revision to GDP led to a larger negative statistical discrepancy. For 2012 and 2013 the statistical discrepancy in the revised data stands at $209.2 billion and $211.9 billion, or roughly 1.3 percent of GDP in both years.

The movement toward a large negative statistical discrepancy is consistent with past patterns in which large increases in stock and house prices were associated with a rise in income relative to output. This is what would be expected if a portion of realized capital gains get reported as normal income. One implication is that the savings rate (5.3 percent in the second quarter) is actually lower, since disposable income is being overstated.

While the 4.0 percent growth for the quarter is a sharp turnaround, it was very much in line with expectations. It means that for the first half of the year, the economy grew at less than a 1.0 percent annual rate. The economy will have to sustain a growth rate of more than 3.0 percent over the second half of the year just to reach 2.0 percent growth for the year as a whole. This means 2014 will likely be another disappointing year for growth.

It also difficult to see how an economy growing at just a 2.0 percent rate can sustain a rate of job creation in excess of 200,000 a month. Presumably, GDP growth will speed up or employment growth will slow.