February 28, 2019

February 28, 2019 (GDP Byte)

By Dean Baker

The slowdown in health care spending that began under Obama is continuing under Trump.

Gross Domestic Product (GDP) grew at a 2.6 percent annual rate in the fourth quarter, putting the growth from the fourth quarter of 2017 to the fourth quarter of 2018 at 3.1 percent, slightly less than the 3.3 percent projection from the Congressional Budget Office (CBO) last spring. The 10-year projections from CBO were notably more pessimistic than the projections from the White House. For at least the first year of the tax cut, the economy is performing somewhat more poorly than CBO had projected.

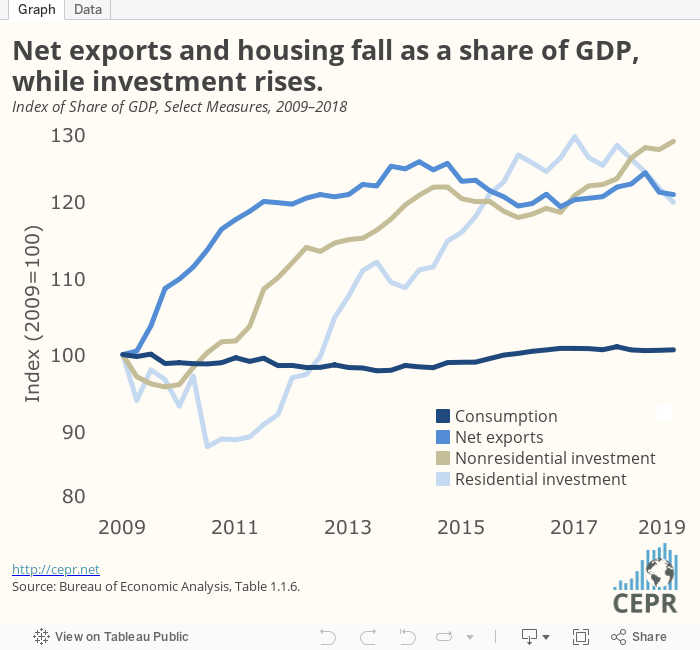

More importantly, the evidence is overwhelming that the impact of the tax cut was a conventional Keynesian demand-side stimulus, rather than the investment-led growth that was the ostensible justification for the large reduction in corporate income taxes. Investment grew at a 6.2 percent rate in the quarter, putting the Q4 to Q4 increase at 7.2 percent. While this is a respectable growth pace, it certainly is not the sort of boom the White House had projected would come from the tax cut. To get the projected impact on productivity and growth, we should be seeing increases in investment on the order of 20–30 percent.

It is worth noting that structure investment, which is long-lived and in principle the category most affected by the reduction in the tax rate, fell at a 4.2 percent rate, the second consecutive quarter of decline. It is up 4.8 percent from the fourth quarter of 2017.

It is also worth noting that there is zero evidence of the uptick in productivity that was supposed to result from the tax cut. With the strong rise in hours worked in the quarter, productivity growth is likely to remain close to the 1.3 percent trend we have seen since 2005.

Consumption grew at a 2.8 percent rate in the quarter. It is up 2.7 percent Q4 to Q4. Durable goods were the fastest growing component of consumption rising at a 5.9 percent annual rate, driven largely by a big jump in autos and parts. Consumption of services grew at just a 2.4 percent rate in the quarter.

This was partly due to slower growth in health care spending, which rose at a 4.8 percent nominal rate in the quarter, only slightly higher than the 4.6 percent rate of nominal GDP growth. Over the last year, nominal health care spending has risen 4.6 percent. This means that the slowdown in health care cost growth that began under the Obama administration is continuing.

Housing continues to be a drag on growth, declining at a 3.5 percent annual rate, the fourth consecutive quarter of decline. This drop is likely to continue into 2019, given the weak data on December starts reported yesterday.

Trade also continues to be a drag on growth, as the deficit rose again in the fourth quarter. Net exports subtracted 0.22 percentage points from growth in the quarter.

The government shutdown had a notable impact on federal spending in the quarter. Non-defense spending fell at a 5.6 percent annual rate, subtracting 0.15 percentage points from growth in the quarter. With most of the shutdown having fallen in the first quarter, there is likely to be a larger drag on growth next quarter; although there will be a bounce back in the second quarter.

One positive is that there still is no evidence of accelerating inflation in this report. The core personal consumption expenditure deflator increased at a 1.9 percent annual rate in the quarter, the same as its rate of increase over the last year.

On the whole, this is a mostly positive report. The growth rate is clearly slowing as the stimulus from the tax cut is fading. We are likely to fall back to the 2.0 percent trend growth rate over the course of 2019. There is zero evidence that the tax cut is producing the promised investment boom that was supposed to get us to a 3.0 percent growth path.

On the other hand, there also is no evidence of any major imbalances in the economy. The savings rate is at a very normal level, suggesting little downside risk to consumption if stock and/or housing prices were to fall sharply. Also, inflation remains well under control, which means that the Fed has no reason to move away from its pause. We look to be on a slow but steady growth path for the foreseeable future.