April 26, 2019

April 26, 2019 (GDP Byte)

By Dean Baker

The annualized rate of inflation shown by the core PCE deflator has actually fallen 0.9 percentage points over the last year.

Gross Domestic Product (GDP) grew at a 3.2 percent annual rate in the first quarter, driven by a large rise in inventories. Pulling out the increase in inventories, final demand grew at a 2.5 percent annual rate in the quarter. The other major factor propelling growth in the quarter was a decline in the trade deficit, which added 1.03 percentage points to the quarter’s growth. A rising trade deficit had been a drag on growth for most of the last two years.

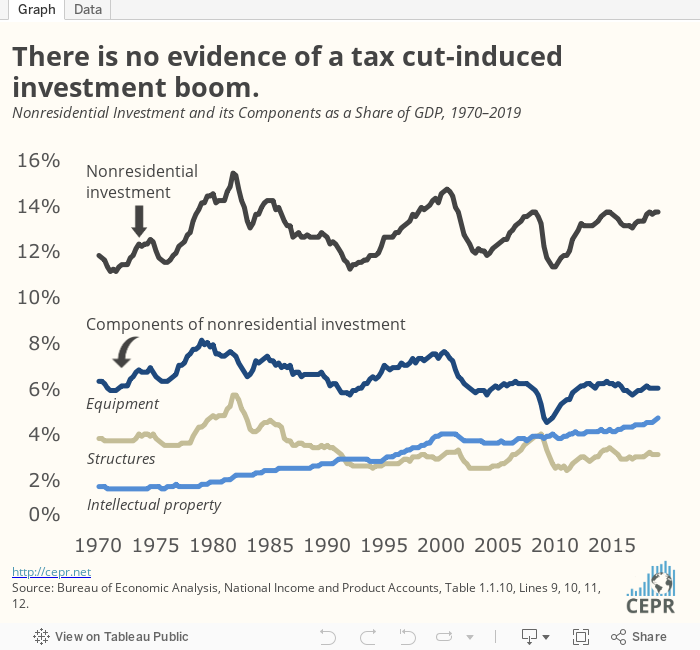

The other big item in the GDP data was the weakness of investment in the quarter, which grew at just a 2.7 percent annual rate. The performance on investment has been notably weak over the last year, growing at a modest single-digit rate. The administration’s projections of the impact of its tax cut imply growth in the neighborhood of 30 percent. We clearly are not seeing anything like this.

Consumption demand was especially weak in the first quarter, growing at just a 1.2 percent annual rate. A plunge in auto sales was the big factor here, with durable goods purchases dropping at a 5.3 percent annual rate. Non-durables rose at a 1.7 percent annual rate, while services increased at a 2.0 percent rate.

One encouraging item in the report is that health care spending still seems to be under control. Nominal spending on health care services, by far the largest component of health care, increased 4.3 percent over the last year, somewhat less than the 5.1 percent rise in nominal GDP. On the other hand, spending on prescription drugs continues to outpace growth, rising 7.1 percent over the last year.

The weak investment figure for the quarter was due to a drop of 0.8 percent in structure investment, its third consecutive decline, and a modest 0.2 percent rise in equipment investment. Investment in intellectual products, mostly software, rose at an 8.6 percent rate. While this pace is respectable, it is not especially fast. Investment in intellectual products increased 7.5 percent in 2016.

Residential investment fell at a 2.8 percent annual rate, its fifth consecutive decline. This subtracted 0.11 percentage points from the quarter’s growth rate. The drop in interest rates this year may turn this around in the second quarter, with construction at least remaining flat.

The fall in the trade deficit was attributable to a modest 3.7 percent rise in exports, coupled with a 3.7 percent drop in imports. This was the sharpest decline in imports since a 3.8 percent drop in the fourth quarter of 2012.

Inventories rose at an unusually rapid $128.4 billion annual rate. This is especially surprising since it was associated with a decline in imports. Since such a large share of our goods consumption is imported, usually large rises in inventories are associated with a large increase in imports. This could be a bad sign for growth in the rest of the year, as inventories are likely to be a drag on growth, even as the trade deficit rises again.

Higher defense spending was again a contributor growth in the quarter, rising at a 4.1 percent rate and adding 0.16 percentage points to growth for the quarter. Due to the government shutdown, non-defense spending fell at a 5.9 percent rate, subtracting an offsetting 0.16 percentage points from growth.

Inflation remains very much under control. The core personal consumption expenditures (PCE) deflator rose at just a 1.3 percent annual rate in the quarter, well below the Fed’s 2.0 percent target. This figure has been trending downward over the last year; inflation is clearly not accelerating in spite of the low unemployment rate.

Overall, this report is pretty much in line with a picture of continued modest growth, once the impact of inventories and the drop in imports are removed. The underlying growth rate is likely near 2.0 percent, now that the boost from the tax cut has faded. Growth is likely to be under this figure for the next two quarters, as slower inventory growth and rising imports are a drag on growth.

A major positive in this report is the slowing of the inflation rate. This suggests the economy is still not hitting any capacity constraints, in spite of the low unemployment rate and large budget deficit. There is still room for further expansion.