January 30, 2013

January 30, 2013 (GDP Byte)

By Dean Baker

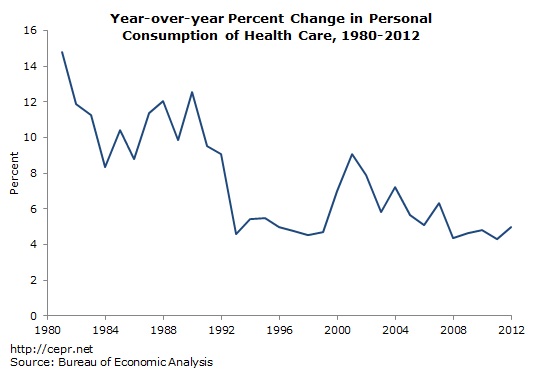

Nominal health care spending rose by just 3.7 percent over the last year.

A sharp drop in government spending, heavily concentrated in defense, coupled with a decline in inventories caused GDP to shrink at a 0.1 percent rate in the 4th quarter. Government spending fell at a 6.6 percent annual rate, driven by a 22.2 percent decline in defense spending, subtracting 1.33 percentage points from the growth rate in the quarter. A 40.3 drop in the rate of inventory accumulation reduced growth by another 1.27 percentage points. Without these factors, GDP would have grown at a 2.5 percent annual rate in the quarter.

Pulling out these extraordinary factors, the GDP data were largely in line with prior quarters. Consumption grew at a 2.2 percent annual rate, driven mostly by 13.9 percent growth in durable goods purchases, primarily cars. This number was inflated due to the effects of Sandy, which destroyed many cars, forcing people to buy new ones. Growth in this category will be substantially weaker and possibly negative in the next quarter. On the other side, housing and utilities subtracted 0.47 percentage points from growth in the quarter. This is likely a global warming effect with warmer than normal weather leading to less use of heating in the quarter. (There was a comparable falloff in the 4th quarter of 2011 when we also had unusually warm weather.)

One especially noteworthy item is the continuing slow pace in the growth of spending on health care services, which accounts for almost three quarters of all health care spending. Nominal spending grew at a just a 2.3 percent annual rate in the quarter. Over the last year, nominal spending is up by just 3.7 percent, far less than the rate of growth of GDP, and well below the projections from the Congressional Budget Office (CBO). It seems increasingly likely that we are on a slower health care cost trajectory. The deficit picture will look very different when CBO incorporates this slower growth trend into its projections.

Investment rebounded from a weak third quarter in which non-residential investment actually shrank. This quarter it added 0.83 percentage points to growth, with investment in equipment and software growing at a 12.4 percent rate. Housing continued to be a big positive in the quarter, adding 0.36 percentage points to growth.

Net exports were a modest drag on growth. While both exports and imports fell in the quarter, the 5.7 percent drop in exports more than offset the positive impact of a 3.2 percent decline in imports. The state and local sector government sector shrank at a 0.7 percent annual rate, knocking 0.08 percentage points off growth. Non-defense federal spending rose at a 1.4 percent annual rate.

The inflation hawks will be disappointed in this report with the overall price index rising at just a 0.6 percent annual rate. The core CPI rose at a 0.9 percent rate. Insofar as there is any trend in these data it is toward lower inflation.

One interesting item in the report was a $122.90 jump (85.2 percent at an annual rate) in dividend payouts. This was the result of companies deciding to pay out dividends to shareholders in 2012 when a lower tax rate was in effect on high-income taxpayers.

There is little evidence in this report to believe that the economy will diverge sharply from a 2.5- 3.0 percent growth path, except for the impact of the deficit reductions that Congress is considering or already put in place. Higher tax collections from the ending of the payroll tax holiday are likely to knock around 0.5 percentage points from growth. The sequester, or whatever cuts are put in place in lieu of the sequester, are likely to have an even larger impact on growth beginning in the second quarter.

One item worth noting is the GDP report provides zero evidence that “fiscal cliff” concerns had any impact on growth in the quarter. Consumer durable purchases and investment in equipment and software were the two strongest components of GDP. If worries over the fiscal cliff were supposed to cause people to put off purchases, consumers and businesses apparently did not get the memo.