November 03, 2016

With open enrollment for health insurance exchanges for 2017 starting soon, the news has been saturated with articles on exploding rates. However, after accounting for the subsidies individuals are eligible for through the Affordable Care Act, a close look at the actual cost for individuals purchasing insurance on the marketplace paints a very different picture.

The Kaiser foundation created a calculator that uses insurance premiums from exchanges in each state, along with available subsidies to estimate the actual costs for those buying insurance. These costs depend on age, family size, income, and location.

Health insurance costs for a silver plan for three types of families in each state were examined. First, estimates for a family of three were obtained, with one 35-year-old and two children and an income of $40,000 per year. Estimates for a family of four were gathered next, with two 35-year-olds and two children, earning $60,000 per year. The last estimate is for a single 60-year-old, with a yearly income of $60,000. All the estimates assume that all those purchasing insurance are non-smokers. For each state, we used a random zip-code from the most populated city.

For a family of three, with one 35-year old adult and two children and an income of $40,000, the cost of health insurance would be about $213 per month in most states, with the exception of Alaska and Hawaii, where it would be slightly cheaper. Overall, for most states, the family would only be spending about 6 percent of their income on health insurance.

The family of four, with two 35 year-old adults and two children and a yearly income of $60,000 would be paying about $400 per month for insurance in most states, except for Alaska and Hawaii where they would be paying $317 and $347 respectively. This family would be spending about 8 percent of their income on insurance premiums.

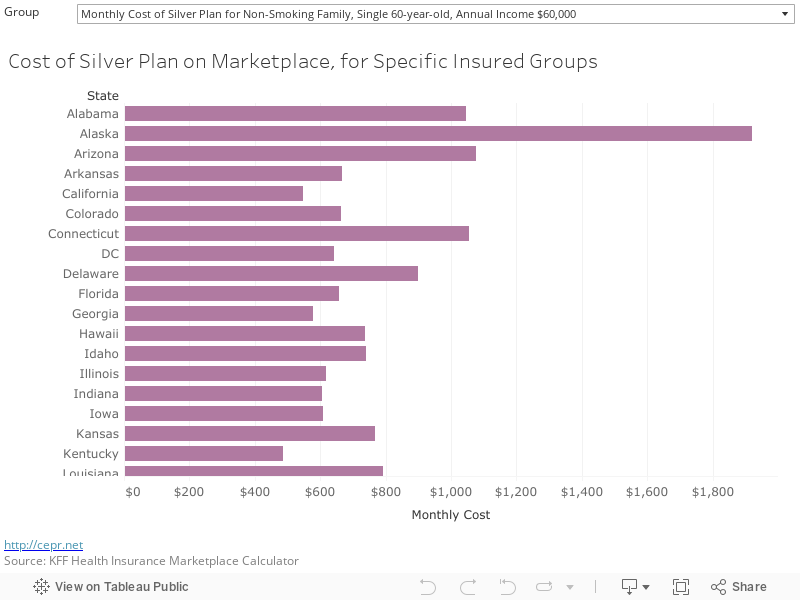

The biggest variations in price for insurance premiums are seen by the single 60-year old with a yearly income of $60,000. This person does not qualify for any type of subsidy and depending on the state they reside in, they may have to spend anywhere between 8 and 38 percent of their income on health insurance premiums. It is worth noting that a person who would have to pay more than 8 percent of their income for insurance is exempted from the penalty for not being insured.

While these premiums might seem high, the underlying issue is that health care costs are expensive. A 60-year-old is in the oldest pre-Medicare age bracket (ages 55 to 64), which has the highest health care costs. These costs are reflected in the premiums. The vast majority of middle-income people in this age group are getting insurance through an employer. The cost of employer-provided insurance averaged more than $6,400 for a single worker in 2016. Most workers don’t directly see this expense since employers cover most of the cost. However, this expense, on average, comes out of workers’ wages. This means that most workers were already effectively paying large amounts for their health care insurance, even if they may not have recognized this fact.

The single 60-year old would have to pay the highest premiums in Montana, South Dakota, Wyoming, Alabama, Oklahoma, Connecticut, Arizona, West Virginia, North Carolina, and Alaska. It is interesting to note that out of these states only Connecticut has a state legislature controlled by the Democrats, with Republicans having the majority of seats in all other states mentioned.