March 27, 2012

March 27, 2012 (Housing Market Monitor)

By Dean Baker

Adjusted for inflation, rents are below their pre-recession level.

The Case-Shiller 20-City Index showed signs of stabilizing in January after falling for six consecutive months, with the index remaining virtually flat. However, there were sharp divergences in price paths across cities, with four (Phoenix, Washington, D.C., Miami, and Minneapolis) showing gains of more than 1.0 percent in January. San Francisco and Portland each had price declines of 0.6 percent. Prices in Cleveland fell by 0.7 percent and prices in Atlanta fell by 1.1 percent.

The sharp price rises in Phoenix and Minneapolis are likely being led by speculators picking up lower-end homes at rock-bottom prices. The price of homes in the bottom tier in the two cities rose by 2.3 percent and 1.4 percent, respectively. Over the last three months, the prices of homes in the bottom tier rose at a 45.6 percent annual rate in Phoenix and a 23.1 percent rate in Minneapolis.

These increases reverse sharp declines from earlier in 2011. Prices of bottom-tier homes in Phoenix are up by less than 8.6 percent from year-ago levels and in Minneapolis by less than 0.1 percent. In both cases, prices are still below the peaks they reached as a result of the first-time homebuyers tax credit (12.8 percent in the case of Phoenix and 21.1 percent for Minneapolis). It is likely that other sharply depressed markets are seeing similar run-ups.

Offsetting these price increases, all three California cities had price declines, although the drop was just 0.3 percent from 0.2 percent in Los Angeles. It is likely that prices will still drop somewhat further in these markets, as they still seem to have air left in their bubbles, especially Los Angeles.

The three other Midwestern cities in the index all saw price declines. The 0.5 percent drop in Chicago is perhaps the most worrisome, with prices falling at a 13.5 percent rate over the last three months. Prices are likely to continue to decline for the immediate future. In Cleveland and Detroit, where prices have already fallen more sharply, it is likely that prices will bump around their new bottom.

Prices were flat in Boston, while falling 0.4 percent in New York. It is likely that prices will edge lower in these cities in 2012.

Other news in the housing market has been similarly mixed over the last month. The pending home sales data for February showed a small drop. Existing home sales also showed a small drop, but this followed a large increase in February. The price data for both the new and existing home series both show a clear downward trajectory.

It is important to remember that new homes sales are recorded when they are contracted whereas existing home sales are recorded when the sale is completed. This means that the new home series is giving more current data on the state of the housing market. In this context, the drop in new homes sales for both January and February may provide some grounds for concern, especially given the unusually good weather in both months in the Northeast and Midwest.

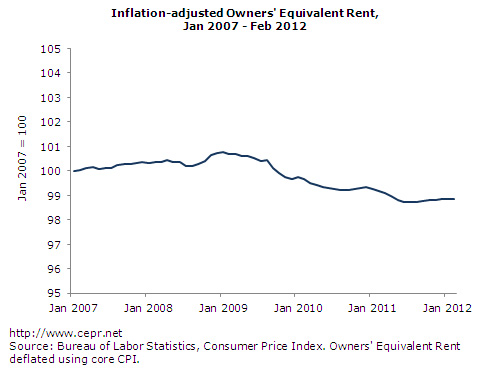

There have been some reports that rents have been rising in many areas, ostensibly due to the fact that people who have lost their homes are now being forced to find rental housing that is in short supply. This really does not make sense as a national phenomenon. Rental vacancy rates continue to be at near-record levels, exceeded only by the peaks reached in 2009 and 2010 near the trough of the recession.

There also is zero evidence of upward pressure on rents in the CPI series. The owners’ equivalent rent series, which pulls out the impact of utilities and exclusively measures rent of shelter, is below its pre-recession level after adjusting for inflation. If anything, it has trended slightly downward over the last two years. This index includes all housing units, not just those on the market, so it will have more inertia than an index that just measured market rents, but it is difficult to imagine that market rents could have risen too rapidly if the CPI series is showing a real decline.