January 11, 2019

January 11, 2019 (Prices Byte)

By Dean Baker

The pace of core inflation has been slowing slightly in recent months.

The overall Consumer Price Index (CPI) fell 0.1 percent in December due to a 3.5 percent drop in energy prices. This was the second consecutive sharp drop in energy prices. This drop held the overall inflation rate to just 1.9 percent over the last year, leading it to come in under the core’s 2.2 percent year-over-year rate. In December, the core CPI increased by 0.2 percent for the third consecutive month.

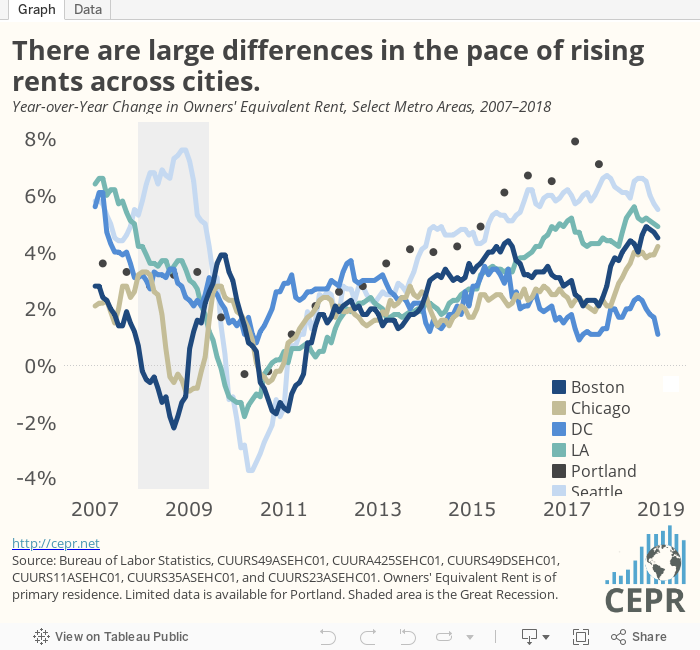

Rents continue to be, by far, the largest cause of inflation in the core. The shelter index rose by 0.3 percent in December and is up 3.2 percent over the last year. The core index, excluding shelter, was up just 1.5 percent over the last year.

As before, there are sharp differences in the rate of rental inflation across cities. The West Coast cities continue to be the big problem areas with Seattle and Portland both seeing rental inflation in the 5–6 percent range and Los Angeles having inflation in a 4–5 percent range. In the last year there has been a sharp increase in the rate of rental inflation in both Boston and Chicago, which has gone from near 2.0 percent to close to 4.0 percent. In contrast, rental inflation in the DC area has remained near 2.0 percent.

Inflation in most other areas of the CPI seems well under control. New vehicle prices and apparel prices were both flat in December. Over the last year, they are down 0.3 percent and are flat, respectively. Even prescription drug prices seem under control, falling 0.4 percent in December and dropping 0.6 percent over the last year. It is important to remember that the CPI shows the change in the price of drugs already on the market. It is not affected by new drugs being introduced at high prices.

Auto insurance prices, which had been a major factor driving inflation, fell 0.2 percent in December, the second consecutive decrease. They are now up 4.6 percent over the last year. The drop in energy costs sent airline fares down by 1.5 percent, following a drop of 2.4 percent in November. They are down 2.6 percent over the last year.

Tuition costs, which had been well contained earlier in the year, are showing some evidence of acceleration. They rose 0.2 percent in December and are up 2.7 percent over the last year. College tuition is up 2.8 percent over the last year.

There also is some evidence that medical care services are returning as a problem area. The price of services increased 0.4 percent for the second consecutive month. They are now up 2.6 percent over the last year. Inflation in hospital services has been even higher, coming in at 0.5 percent the last two months and 3.7 percent over the last year.

Health insurance costs (these are purely administrative costs, net of payments to providers) also are becoming a bigger problem. They rose 1.3 percent in December and are up 5.4 percent over the last year. This is the highest year-over-year rate of increase in two years.

However, in spite of the evidence of some acceleration of inflation in the traditional problem areas of education and health care, there is zero evidence of increasing inflation in CPI as a whole. While the sharp drop in energy prices is a onetime occurrence that will not be repeated, inflation is not accelerating at all in the core. The annualized rate, comparing the last three months (October, November, December) with the prior three (July, August, September), is just 2.0 percent, down slightly from the 2.2 percent rate over the last year.

On the whole, this report shows a very positive picture. Inflation is well-contained almost everywhere, with the important qualification that health care services and education may be returning as major problem areas. The fact that inflation appears to be slowing, rather than accelerating, indicates that the Federal Reserve has little to fear about out-of-control inflation in the immediate future. And, the slower rate of overall inflation is translating into healthy real wage growth.