Article • Dean Baker’s Beat the Press

The collapse of the housing bubble led to the downturn. However that does not mean that housing is the road out, or at least not unless we expect to see another bubble. Ezra Klein presents this mistaken view in his column today.

The basic story is very simple. (Remember, the purpose of economics is to make simple things complicated so as to exclude most of the public from debates on the most important policy issues that affect their lives.) The economy in the bubble years was driven by the bubble. The huge run-up in house prices led to an extraordinary building boom. Residential construction, which is ordinarily 3-4 percent of GDP rose to more than 6 percent of GDP at the peak of the boom in 2005.

Bubble-inflated house prices created close to $8 trillion dollars of housing equity. The housing wealth effect implies that people would spend between 5 to 7 cents on the dollar of this additional wealth, creating between $400 billion and $560 billion in additional annual consumption. The property taxes on inflated house prices also helped support perhaps $80 billion or so in state and local government spending. For good measure there was a bubble in non-residential real estate that followed in the wake of the housing bubble, which created a boom in this sector as well.

When the bubble burst, there was nothing to replace the lost demand. Residential construction fell by more than 4 percentage points of GDP ($600 billion annually in today’s economy). It fell below normal levels because the boom of the bubble years had led to record vacancy rates. Consumption plunged because the housing bubble equity disappeared. When the wealth was gone, the consumption that it generated also vanished. And, we saw cutbacks in government spending at the state and local level in response to the lost tax revenue.

All of this seems clear and simple. We lost $1.2 trillion to $1.4 trillion in annual private sector demand. Some of this has been replaced by the federal government’s budget deficits, but not enough to fill the gap. So what would have various plans to rescue housing done?

Suppose we had instantly written off all underwater mortgages, would that have kept construction going? That’s hard to see, since the enormous oversupply of homes would still be there.

Would that have sustained house prices? It’s hard to see how or why, the problem is that the bubble had raised prices far above any level that could be justified by the fundamentals of the housing market. House prices today are pretty much in line with their long-term trend as we can see from the real Case-Shiller house prices index.

Source: Robert Shiller.

Source: Robert Shiller.

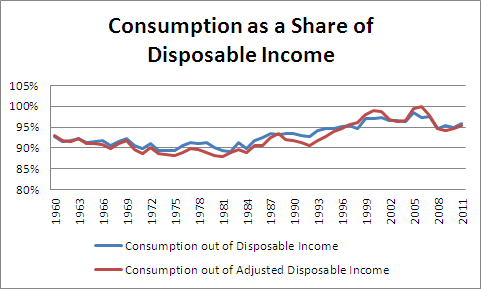

If house prices are basically right, why should we expect more consumption than we are now seeing. In fact, consumption remains unusually high, not low, relative to disposable income as shown below. (Adjusted disposable income has to do with the statistical discrepancy for those nerds out there.)

Source: Bureau of Economic Analysis, National Income and Product Accounts, Tables 2.1 and 1.7.5.

If consumption isn’t low, then what is the story of how rescuing underwater homeowners would have saved the economy? There are some economists who argue that the consumption of underwater homeowners has a hugely disproportionate impact on the economy. That seems a bit hard to imagine.

Let’s try some simple numbers. The total amount of underwater equity is estimated at around $700 billion. Suppose that we wiped that out tomorrow. If our underwater homeowners spent 15 percent of their equity each year, more than twice as large as the wealth effect more generally, this new equity would generate $105 billion a year in additional consumption, about 0.7 percent of GDP. That’s helpful, but not close to enough to get us back to full employment.

Furthermore, this impact is probably not even realistic. Let imagine someone with a median home, worth roughly $180k. We’ll give $60,000 a year in income, roughly 20 percent more than the overall median. (Homeowners have higher income on average.)

Let’s assume that they are 25 percent underwater, which means that they have a mortgage of $225,000. We now wipe that out, in effect giving them $45,000 of additional equity. If they spend 15 percent of this equity, it would translate into $6,750 a year in additional consumption. Did this family earning $60,000 a year have $6,750 in annual savings that they now can divert to consumption since we set their mortgage above water? That seems unlikely. Perhaps they will borrow to support additional consumption, but how much and for how long? On average, people do have to save over their working lifetime if we expect them to have anything other than their Social Security in retirement. (Paying down a mortgage counts as savings.)

The story is even more dramatic if we give them a loan to value ratio of 150 percent. Then their mortgage is $270,000 and they are $90,000 underwater. If we write that one off and expect them to spend 15 percent of their new equity it comes to $13,500 a year. That doesn’t seem very likely.

In short, the story of underwater homeowners holding up the recovery doesn’t hold water. It is a tragedy for homeowners facing the loss of their homes and foreclosures can devastate communities, but it is not the story of the recession.

The simple story is that we need a new source of demand to fill the gap left by the collapse of the housing bubble. In the short term that can only be the government. In the longer term it will have to be trade, which means a reduction in the trade deficit. That means first and foremost getting the value of the dollar down, but macho politicians in Washington don’t talk about a lower valued dollar. The folks on Wall Street don’t like it.