Article • Dean Baker’s Beat the Press

Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

I see that I have to disagree with Brad DeLong again. Brad wants to see the 2008 downturn as a uniquely bad event due to the overextension of credit and the ensuing financial collapse. I see it as overwhelmingly a story of a burst housing bubble and the resulting fallout in the real sector.

First off, in this piece Brad seems to want to attribute the worldwide downturn to the collapse of the housing bubble in the U.S. This seems more than a bit bizarre, since countries like Spain and Ireland arguably had bigger bubbles and bigger collapses than the U.S.

The collapse in the U.S. may have happened first and triggered the collapse in other countries, but this would only be in the sense that the U.S. collapse might have alerted lenders to the possibility that house prices can fall. Presumably the bankers would have discovered this basic economic fact at some point regardless of what happened in the United States.

If we recognize that the collapse in Europe and elsewhere had its own dynamic, then we take away some of the drama from Brad’s story of a small bubble causing a massive downturn. But I want to take away some more. First, the bubble was much larger than Brad implies. Second, we have seen this story before, specifically in 2001.

On the size of the bubble, Brad sees a relatively small amount of overbuilding due to the uptick in construction in the years 2003-2006 compared to 2002. The problem with this assessment is that 2002 was a year in which we were already well into the bubble. If we use the period 1994-1996 as a base, construction was already 10 percent above its population adjusted trend path by 2002. It rose further in the peak bubble years, but we should not compare it to a year in which construction was already inflated by the bubble.

If we need further evidence of overbuilding, the Census Department gives it to us in data showing that vacancy rates were already at a record high in 2002. This meant that when the bubble burst, we would not only see a fall back in construction to trend levels, but a plunge well below trend levels in order to work off the massive oversupply from the bubble years.

In addition to the lost construction, it was totally predictable that we would also see a sharp drop in consumption, which had been driven by ephemeral housing bubble wealth. It is bizarre that the wealth effect seems to have disappeared from economists’ radar screens. We have lots of economists running around telling us that people don’t spend because of debt, but somehow it doesn’t matter whether or not they have wealth.

Well, way back in the old days of 2002-2006 it was common to believe that people spent money based on their housing wealth. In fact, some guy named Alan Greenspan put out several papers that argued that cash out refinancing was a major factor boosting consumption. Since rising home equity surely caused some people to spend more, and almost certainly did not cause anyone to spend less, it does seem likely that the housing bubble added to consumption. If the housing bubble was not responsible, it would be interesting to hear another explanation for why the saving rate dipped to a record low 2.5 percent in 2005.

These factors matter, because if we expect the end of the bubble to lead to a collapse in construction on the order of 4.0 percentage points of GDP and the loss of housing wealth to lead to a drop in consumption in the neighborhood of 2-3 percentage points of GDP, then we don’t have to look to the fun in the financial sector as being the driving force in the recession. It can be mostly attributed to a loss in demand originating in the real sector of the economy.

For this reason the story of the 2001 recession matters a great deal. The 2001 recession was also due to a collapsed bubble, in this case the stock bubble. It also led to a sharp falloff in real demand as the investment boom that had been caused by the bubble quickly dissipated and consumption fell back to more normal levels after the disappearance of the stock wealth that had raised it to then record levels.

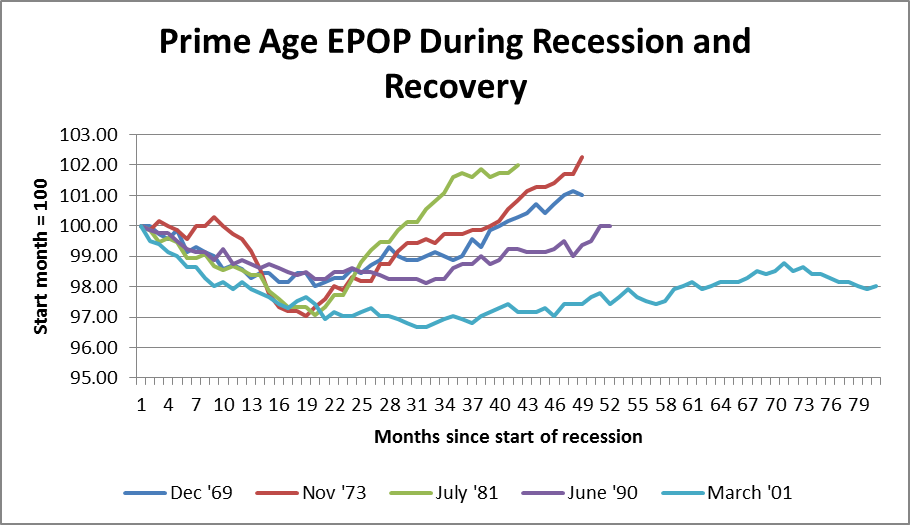

Brad sees the 2001 recession as short and mild, fitting his story that the financial crisis caused the deep downturn in 2008-2009 and the subsequent weak recovery. I would argue that the 2001 recession was actually quite severe based on the performance of the labor market. The figure below shows the trend in employment rates of prime age workers (ages 25-54) in the 2001 recession and the four preceding recessions. (I use prime age workers to control for demographic changes over this period.)

Source: Bureau of Labor Statistics.

As can be seen, in three of the four prior recessions the employment to population ratio for prime age workers had fully recovered by the 40th month since the onset of the recession. In the case of the 1990 recession it took 50 months. In the 2001 recession, the prime age EPOP had still not recovered to its pre-recession level by the 81 month, at which point the 2008-2009 recession had already begun. From this perspective, the 2001 recession was very bad news.

Brad doesn’t see this because he is looking at growth data. Growth did resume and was reasonably healthy in 2002 and 2003 even as employment continued to fall. The difference is of course productivity growth. This productivity growth looks like the dividend from the investment boom at the end of the 1990s and 2000. It should not be surprising that it took 2-4 years to realize the full benefits.

Whether the 2001 recession was a big deal matters in my telling of the story, since I see it as a simple point that recessions caused by bubbles are not easy to recover from. It is not easy to find some alternative source of demand to fill the gap when the demand driven by the bubble disappears. We can do it with big-time stimulus, but politicians get scared away from going this route since the deficit scolds will yell at them. By contrast, the normal Fed induced recession is easily corrected by the Fed reversing its course and lowering interest rates.

My take-away is to be wary of situations in which a bubble is driving the economy. This was easy to see in the late 1990s, as consumption soared and spending by dot.nonsense pushed investment to its highest share of GDP in two decades. It was also easy to see in the housing bubble years. It is a good idea to crack down on nonsense promulgated by the financial sector, but the basic story really is a simple one. When an asset bubble is causing large and unusual spending patterns, you’ve got a problem.