Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

January 27, 2017

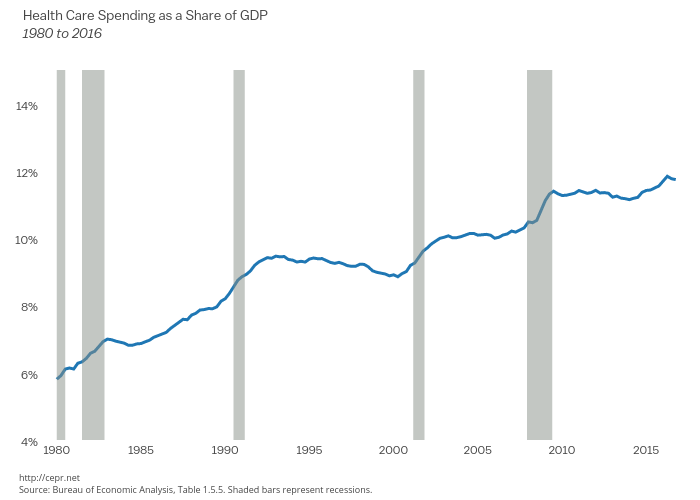

The relative stability in health care spending over the last seven years has been striking. Health care costs have risen far less than had been projected by the Congressional Budget Office and other forecasters. This has led to enormous savings on Medicare and Medicaid and also meant a shift from health care benefits to wage compensation. The slow growth in spending is especially striking since it is occurring at a time when the aging of the population should be putting substantial pressure on costs. For more, read the latest GDP Byte.