April 1, 2016

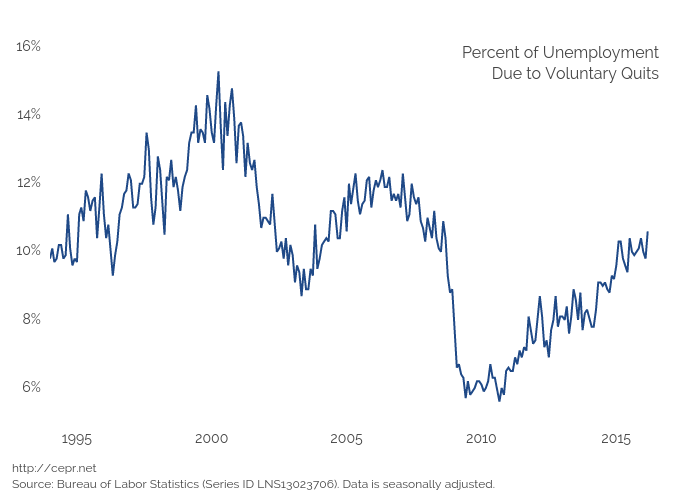

One positive item in the household survey was a large jump in the percentage of unemployment due to voluntary quits. This sign of confidence in the labor market rose to 10.5 percent, the highest level in the recovery to date, although it’s still more than a percentage point below the pre-recession peaks and almost five percentage points below the peak reached in 2000. For more, see the accompanying Jobs Byte.