Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

October 26, 2018

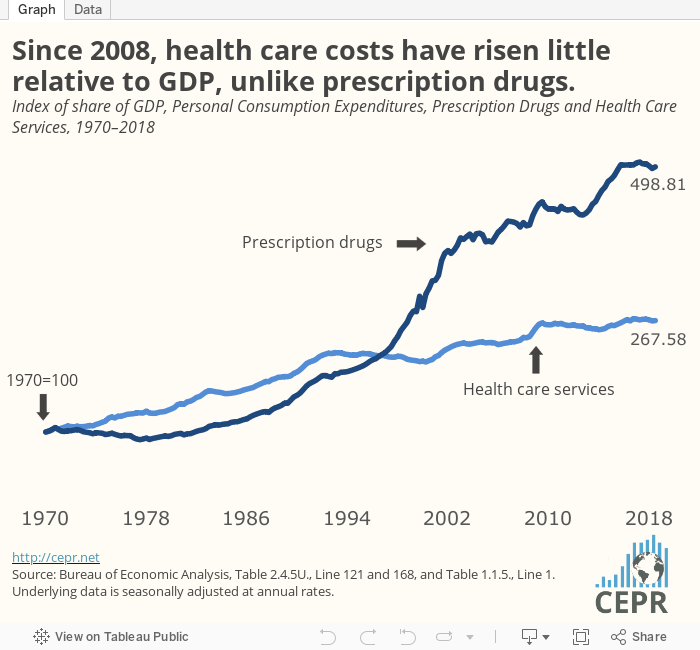

Nondurable consumption rose last quarter at a surprisingly rapid 5.2 percent rate, adding 0.72 percentage points to growth. Spending on prescription drugs was the biggest part of the story, rising in real dollars at an 8.6 percent annual rate. Spending on health care services also increased rapidly in the quarter, rising in real terms at a 4.6 percent annual rate and contributing 0.52 percentage points to the quarter’s growth.

The sharp rise in spending on health care services is somewhat of an anomaly, as growth has slowed sharply since 2008. The growth in prescription drug spending is also a jump from recent quarters, although it is less out of line. For more, check out the latest GDP Byte.