Article • Dean Baker’s Beat the Press

Looking at What People Do, Not What They Say

Article • Dean Baker’s Beat the Press

Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

Since Donald Trump took office and embarked on his strategy of slashing government and hugely increasing import taxes (tariffs), measures of both consumer confidence and business expectations have fallen through the floor. We have seen the same pattern virtually everywhere, with many measures falling below levels seen in the pandemic and the Great Recession.

When asked about this collapse in confidence this weekend, Treasury Secretary Scott Bessent said that we should look at what people do, not what they say. I am generally inclined to believe this approach is best, especially when looking at consumers.

Business people pretty much have to be reasonably well-informed about the state of the economy. They are constantly making decisions about ordering parts and equipment, expanding capacity, hiring, and wages. These all require some knowledge of the state of the economy, so we can assume their statements about business conditions have some foundation in reality.

However, consumers answering questions on a survey are in a somewhat different situation. They know whether they have a job and how much they pay on their mortgage, but they are not forced to constantly evaluate the state of the economy. Therefore, their answers to a survey could reflect what they heard in a tidbit on the news or saw on social media as opposed to a serious assessment of the economy. For this reason, Bessent is right to suggest that we focus more on what they do than what they say.

This is not as easy to sort out as Bessent suggests. Overall, inflation-adjusted consumer spending has fallen in January and February, the first two months that Trump has been in office which is not a great picture. (We get March data this week.) This decline is entirely due to a sharp falloff in spending on cars and other durable goods, after a big jump in November and December.

To my view, that’s a story where many people looked to buy these big-ticket items in advance of any tariffs that the Trump administration would impose. People who bought a car at the end of 2024 were not about to buy another one at the start of 2025, so the drop was pretty much inevitable. We can argue whether this is a good or bad story, but the decline in spending on durables doesn’t necessarily mean people were feeling bad about their economic situation in the first two months of the year.

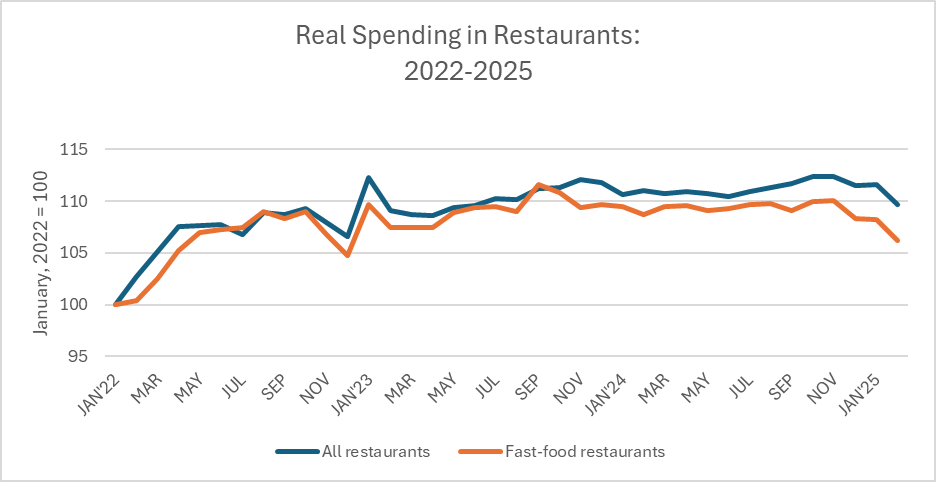

My preferred measure for a real-time assessment of people’s views about their own economic situation is real spending on restaurants. This is useful since eating at restaurants is pretty much the ultimate in discretionary spending. If you think your financial situation is deteriorating, then you likely will be going out to eat less, or at least eating at less expensive restaurants. The Bureau of Economic Analysis also breaks out fast-food restaurants (limited service) separately, so we can see a measure that is unlikely to be skewed by the behavior of high-income people. Here’s the story since January of 2022.

I chose January of 2022 as the start part since we were largely through the worst of the pandemic at that point, although the omicron strain of Covid was likely still discouraging many people from being in public more than necessary.

As can be seen, both series rose sharply through the first half of 2022, with the series up more than 7.0 percent by the summer. (Remember, this is real spending, so the data in the graph pulls out the impact of higher prices.)

After that, spending continued to edge higher, with both series being more than 10 percent above their January 2022 level by the summer of 2023. From that point forward, the series for spending at fast-food restaurants largely leveled off, while overall spending increased to more than 12.0 percent above the January 2022 level by November of 2024.

Since November of 2024 both series have fallen sharply. Real spending in restaurants overall is down by 2.4 percent as of February, a 9.4 percent annual rate of decline. Real spending in fast-food restaurants is down by 3.5 percent, a13.4 percent annual rate of decline. At least when it comes to their spending on restaurants, people are telling us that they are not doing very well.

What should we make of this? Two months of data can’t tell us all that much about the economy. Other factors, such as weather, can also affect how much people are going to restaurants. Again, we will have more data this week when the first quarter GDP data are released.

But if we want to get beyond all the surveys telling us people have a negative view of the economy, and see what people are actually doing, the picture does not look very good either.

Article

Article

Article

Article

Article

Article

Article

Article