Article • Dean Baker’s Beat the Press

By Dean Baker and Nick Buffie

The Peter Peterson gang has been hard at work lately trying to get people worried about the budget deficit. After all, with interest payments on the debt as a share of GDP at a post-war low and an interest rate on long-term Treasury bonds of almost 2.0 percent, things look pretty bleak. (That’s sarcasm.)

But the Washington deficit hawks (great name for a NFL team) have never let the real world interfere with their ranting about deficits, which invariably turn to the need to cut Social Security and Medicare. Unfortunately, they are getting some support in this effort from the folks at the Congressional Budget Office (CBO).

While the CBO forecasts don’t look exactly like the sky is falling end of the world stuff, they do show that the debt and deficit will both rise as a share of GDP. And, if the debt is rising as a share of GDP, and we never do anything, then at some point it will do real damage to the economy.

Most of this logic is beyond silly in a context where the economy is still far below its full employment level of output. Debt or deficits can only be an issue when the economy is close to full employment, until that point the only problem with deficits is that they are not large enough. Cutting deficits when the economy is below full employment means slowing growth and throwing people out of work.

But that is not the point I wanted to make. I thought it was worth showing why CBO is projecting that deficits will rise over the next decade. If we turn to Table 1-2 of the latest CBO Budget and Economic Outlook, we find that the deficit for this year is projected to be 2.9 percent of GDP. This should leave the ratio of debt-to-GDP more or less constant, depending on the exact growth and inflation numbers for the year.

However if we look out to 2026, the end of the CBO projection period, the deficit is projected to be 4.9 percent of GDP. At that level, the debt-to-GDP ratio would be rising, and we would be down the road toward higher interest payments leading to higher deficits, leading to higher interest payments and pretty soon, Zimbabwe.

The Peterson folks have made a big point of touting this 4.9 percent figure and the higher debt and interest payments associated with it, so it is worth asking how we get there. If we look at the CBO projections, they project that mandatory spending on items like Social Security and Medicare will rise by 1.7 percentage points of GDP. This is large the result of baby boomers reaching retirement age, but also includes some excess cost growth for health care in programs like Medicare, Medicaid, and the subsidies in the exchanges.

Bu the projected increase in mandatory spending is largely offset by a projected decline of 1.3 percentage points in the discretionary portion of the budget. This is the category of spending that includes the military, along with spending on infrastructure, health care research, national parks, and just about everything else we see the government do.

Let’s leave aside whether the projected cuts to this area of the budget is a good idea and just do the arithmetic. The net effect of projected changes in spending is an increase in the annual deficit of 0.4 percentage points of GDP, well short of the 2.0 percentage point rise from 2.9 percent of GDP in 2016 to 4.9 percent of GDP in 2026. The rest of the rise is due to an increase in projected interest payments from 1.4 percentage points of GDP to 3.0 percentage points of GDP. (CBO also assumes that revenue will fall by 0.4 percentage points of GDP due to the Fed rebating less money to the Treasury from its holdings of assets [see Table 4-1]).

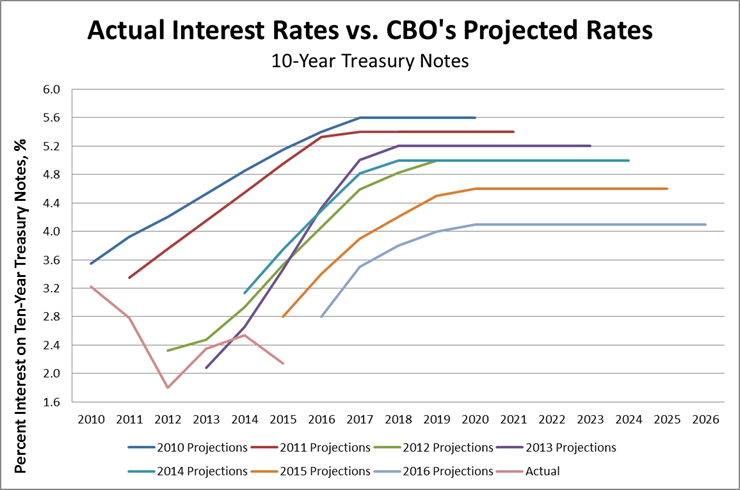

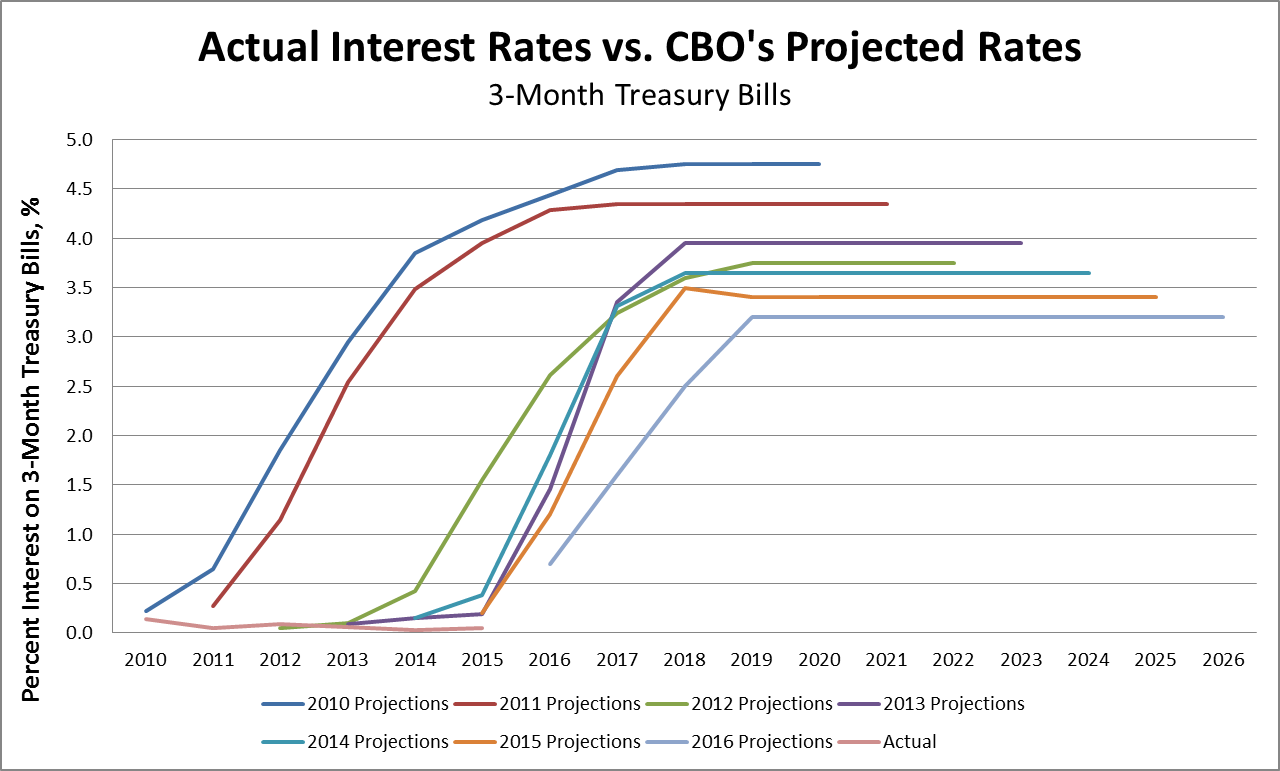

But the higher interest payments are not due to a soaring debt to GDP ratio, rather the projections of higher interest payments are due almost entirely to CBO’s assumption that interest rates will be much higher in the decade ahead than they are today. CBO projects that the interest rate on 90-day Treasury bills will rise from its current level of around 0.3 percent, to 2.0 percent next year, and 3.25 percent for 2019 and subsequent years.

They have a similar story with long-term rates. The 10-year Treasury bond rate is projected to rise from its current 1.8 percent to over 3.0 percent next year, and 4.25 percent in 2020 and subsequent years. While these projections are not obviously ridiculous, it is worth pointing out that we have seen them before.

As the figures below show, ever since 2010 CBO has consistently shown a sharp rise in interest rates for the later years in its forecast.

We can now say that for six consecutive years it has grossly overstated the future rise in interest rates, for at least the years that have passed to date. This doesn’t rule out that CBO might finally get it right, but it does suggest treating these projections as something less than the Holy Grail. And, if interest rates in 2026 look something like interest rates today, then we lose altogether the story of rising debt and deficits.

There is one other point worth making. If at some future point we find that deficits really are pulling resources away from the rest of the economy, it is not that difficult to raise taxes. In 2013, the payroll tax was raised by two full percentage points, as the payroll tax holiday put in place in 2011 ended. Less than 30 percent of the people survey in an online poll even realized that their Social Security taxes had been raised that year.

Furthermore, 20 percent of the people surveyed in 2014 (a year in which there was no tax increase) also answered that their Social Security taxes had been raised that year, suggesting that their answer might have been more attributable to their view of politicians than remembrance of any real world tax increase. This implies that only about 10 percent of the public even recognized a very large tax increase that took place in a weak labor market. This would indicate that if higher taxes were really needed to support current spending, it would be possible raise the necessary revenue.

In short, the CBO projections that we will have a deficit problem due to an ever growing interest burden are based on assumptions that have been shown wrong in each of the last six years. Furthermore, if they eventually do prove right, the situation is one that we can easily deal with.