Article • Dean Baker’s Beat the Press

An important provision of the new federal tax code was the capping of the deduction for state and local taxes at $10,000. This was an explicit hit at states like New York and California, which have relatively high tax rates in order to provide relatively high-quality services in areas like education and health care. These states also tend to vote Democratic in national elections.

One way that these states can partially get around this cap is by replacing a portion of the state income tax with an employer-side payroll tax. This can be in such a way that almost no one would end up paying more in state taxes, but they would effectively be able to still deduct their taxes from their federal income taxes.

The way a payroll tax works is that an employer pays it on the worker’s wage. If a worker gets paid $50,000 a year and we impose a 5 percent employer-side payroll tax, then the employer would pay $2,500 on this worker’s pay.

Economists generally believe that employer-side payroll taxes come out of wages. Employers don’t care whether they have to pay the money to the worker or to the government, they will pay the same amount in either case. (To make the transition as easy as possible, it should be done in two or three steps, which would mean that workers would more likely be foregoing pay increases rather than looking at actual cuts in pay.)

In this case, the new payroll tax would lead to a reduction in this worker’s pay of $2,500 to $47,500. But if the worker had been paying 5 percent of their wage to the state income taxes, they are in the exact same position as they had been in previously. They have $47,500 income after the money paid to the state in taxes.

The big difference comes when they pay their federal income tax. If they getting paid $50,000 and are unable to deduct their state taxes from their income, they will pay federal taxes on the full $50,000. However, with the employer side payroll tax, they will only pay income tax on the $47,500 they get paid by their employer. This will save them from paying income tax on $2,500 and also Social Security and Medicare taxes on this money.

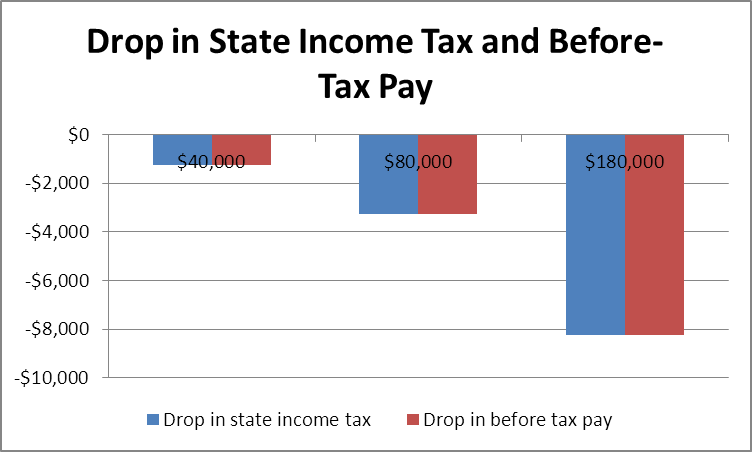

The figure below shows the change in state income taxes and before-tax income at three different wage levels — $40,000, $80,000, and $180,000 — from substituting a 5 percent employer-side payroll tax for a 5 percent income tax. In each case, it assumed that there is a zero bracket below $15,000 so very low wage workers would not be subject to the payroll tax, just as they do not pay the state income tax.

Source: Author’s calculations, see text.

As can be seen, at each wage level the drop in before-tax pay should be equal to the savings on state income taxes. This means that workers are not harmed by the shift in the tax burden from income taxes to an employer-side payroll tax. While this shift does not hurt them relative to their position with the state government, it does substantially lower their federal tax burden.

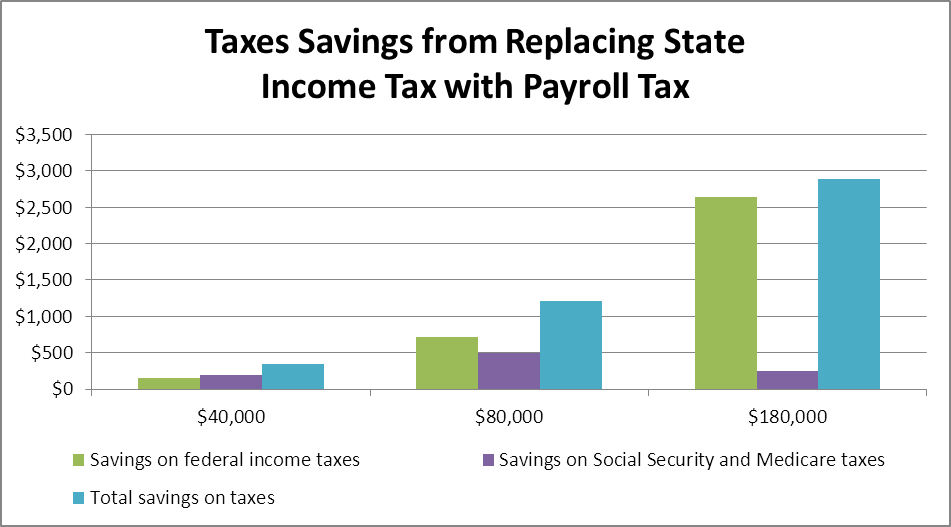

The figure below shows the savings on income taxes and Social Security and Medicare taxes at each of these three wage levels.

The worker earning $40,000 a year would save $150 a year on his income taxes and $192 a year on his Social Security and Medicare taxes for a total savings of $342. A worker earning $80,000 a year would save $715 a year on her income taxes and $499 a year on her Social Security and Medicare taxes for a total savings of $1,214. A worker earning $180,000 a year would save $2,640 a year on her income taxes and $243 a year on her Social Security and Medicare taxes for a total savings of $2,883.

The reason the savings on Social Security and Medicare taxes is so much less for this worker is that the Social Security tax is capped so that it doesn’t apply to wage income over roughly $130,000. This worker would only be subject to the 2.95 percent Medicare tax on her last $8,250 in wage income.

As can be seen, this is a relatively simple and painless way for New York to work around the Republican effort to hurt Democratic states by limiting the deduction for state and local income taxes. There are a few additional points worth making here.

First, the payroll tax should be seen a partial replacement for the state income tax. The state has a progressive income tax, which there is no reason to get rid of and replace with a regressive payroll tax. The state, however, should adjust its income tax to accommodate the new payroll tax.

For people who had been paying a 5 percent tax rate, it could be a simple replacement, but for higher brackets, the income tax should be reduced by the amount of the payroll tax. This means that if someone had been subject to a 6.4 percent income tax rate, say on income above $40,000, they would instead be subject to 1.4 percent tax rate on the income above $40,000. Millionaires, who pay an 8.8 percent tax rate on income over $1,000,000, would instead pay a 3.8 percent tax rate on income over $1,000,000.

Also, this change would only apply to wage income. The tax on income from dividends, interest, capital gains and other types of capital income can be left unchanged.

This means that some wealthy people will still lose out on the ability to deduct some of their state and local taxes. While it would be desirable to not have these people effectively penalized by the federal government for living in the state of New York, these are the biggest gainers from the tax cut, so it would be difficult to feel too bad for them.

This switch to an employer-side payroll tax also has the huge benefit of effectively allowing people who would not itemize to deduct their state income tax from their federal income taxes. That will leave most New Yorkers better off than they were before the change in the code.

It also allows for savings on Social Security and Medicare taxes. This is big savings for middle-income workers, although it does have the downside that it reduces funding for these programs and also means workers will see somewhat lower Social Security benefits when they retire. Hopefully, the state can encourage workers to put some of their tax savings into a retirement plan so they do not end up with reduced retirement income.

This sort of gaming of the tax code by states is far from ideal. The different levels of government should be working together in the public interest rather than trying to gain at the expense of each other.

However, it would be foolish for the state of New York to pretend that everything is normal when the President and Congress have effectively declared war on the Democratic states. An employer-side payroll tax can save New York’s workers more than $6 billion a year from their federal taxes, putting more money in their pockets and providing a boost to the state’s economy. It is a very effective way to fight back against the Republican tax plan.