Article

The Federal Reserve’s Federal Open Market Committee continues to debate whether it should raise short-term interest rates to prevent inflation. The effects of raising these interest rates cascade throughout the economy: rates for automobile loans and mortgages will rise and the economy will generally slow. But a slower economy means that fewer people have jobs and workers will have less bargaining power to demand higher wages. With inflation already low and the economy still recovering from the Great Recession, there are good arguments for the Fed keeping rates low.

Looking into the future, low rates will help the most marginalized and disadvantaged. For example, the gains from lower unemployment will disproportionately help black workers. History provides more reasons for keeping rates low: black workers were hit much harder than whites, Asians, or Hispanic/Latinos in both the 2001 and 2007 recessions. In addition, the incomplete recovery from the 2007 recession is on top of an incomplete recovery following the 2001 recession.

This is evident looking at the unemployment rate and employment rate (or EPOP ratio, employment-to-population ratio) of prime-age (25 to 54) blacks and whites for the 2001 and 2007 recessions. (Looking at prime-age workers, who are in an age group likely to be working, helps eliminate any demographic effects that might be also happening.)

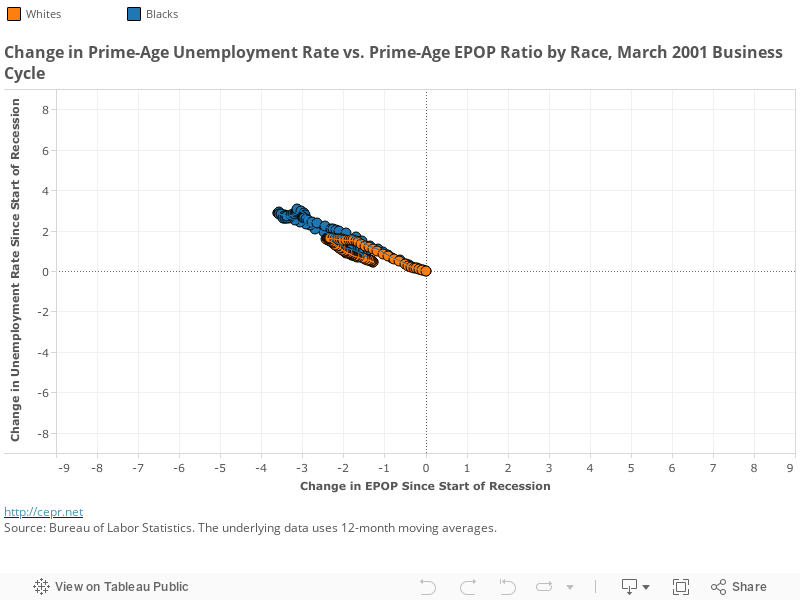

The graph below shows the change in the unemployment rate on the y-axis and the change in the EPOP on the x-axis for the 2001 business cycle. As the recession progresses, the graph moves up and to the left (i.e. the employment rate declines and the unemployment rate increases); during the recovery, it moves down and to the right.

The peak increase in the unemployment rate for blacks was during October 2003; the unemployment rate was up 3.1 percentage points at that point in the recession. In March and April 2005, the black EPOP ratio reached its nadir, a loss of 3.6 percentage points. During the period October 2003 to May 2004, the white unemployment rate peaked with a 1.6 percentage point increase. The white EPOP was at its low with a loss of 2.4 percentage points.

It’s clear that black workers had a more difficult experience during the 2001 recession, as they had a greater increase in unemployment and decrease in the EPOP ratio. It’s also worth noting that for blacks, the recession was a lot longer. Both measures for blacks started to improve in April 2005, a year after both measures started to improve for whites.

The recovery from the 2001 recession was also incomplete. For whites, the unemployment rate was 0.6 percentage points higher and the EPOP was still down 1.4 percentage points at the end of the business cycle. For blacks, it was worse: at the brink of the 2007 recession, the unemployment rate was still 0.8 percentage points higher, and the EPOP was down 1.6 percentage points.

We see the same story for the 2007 recession, except the 2007 recession was much, much more severe. The worst point for blacks was around October 2011, where the unemployment rate was 7.9 percentage points higher than before the recession. The EPOP had lost 8.1 percentage points at this point.

For whites, the worst point was from August 2010 to November 2010. The increase in the unemployment rate peaked at 4.7 percentage points, while the EPOP ratio lost 4.5 percentage points. Not only was the recession much worse for blacks it was, again, longer. These measures started to improve for whites about a year before they did for blacks.

The recovery is still incomplete for both blacks and whites, and blacks have much more ground to make up. In addition, since many prime-age workers left the labor force during the recession, the unemployment rate has recovered faster than the EPOP ratio, which is still way down since the beginning of the recession.

Considering that there were incomplete recoveries for both of the last two recessions, and that blacks fared much worse during the recessions and recoveries, the Fed should reconsider any plans to raise interest rates, which would slow any additional improvements in the labor market and give workers less bargaining power.