Article

By February 2018, many rich people have stopped paying into Social Security for the year. The essential program, which provides retirement, disability, and survivor benefits to millions every year, only taxes the first $128,400 of a salary (up from $127,200 in 2017). Any wage income above this payroll tax cap is not subject to the tax.

Since the vast majority of people in the United States make less than $128,400 per year, they pay the 6.2 percent payroll tax for the entire year. But those with incomes over the cap pay a lower effective tax rate.

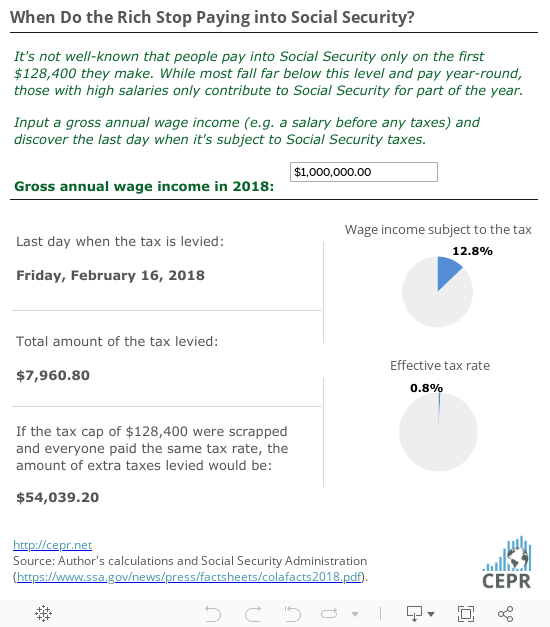

For example, someone with a salary of $50,000 pays into the program for the entire year — up until December 31st — and has a 6.2 percent effective Social Security tax rate. But someone who makes $1,000,000 in 2018 stops paying Social Security taxes on February 16th — and has an effective tax rate of just 0.8 percent. In other words, the burden of Social Security taxes falls more heavily on those who make less money.

The tax cap also has consequences for Social Security’s finances. Many commentators say that because Social Security is projected to have a shortfall in the 2030s, benefits need to be cut today. But over the last four decades, the upward redistribution of income has meant that Social Security has less of a base on which to draw. In 1983, 90 percent of wage income was under to the tax cap; in 2015, it was just 82.6 percent. This decline represents a large share of the shortfall in the program’s financing. What’s more, stagnant and increasingly unequal wages below the cap have strained the program’s finances even more. In the period since 1983, if workers’ wages had kept up with productivity growth and the payroll tax cap continuously captured 90 percent of wage income, Social Security would have an additional $1.7 trillion in its trust fund.

Yet despite these issues, modest changes to current law in order to address this unfairness — including scrapping the Social Security payroll tax cap and making everyone pay the tax for the entire year — could eliminate the shortfall entirely and even allow for increasing benefits.

To better illustrate these points, CEPR has developed the calculator below (also available here) which shows the last day when salaries, if spread evenly throughout the year, are subject to Social Security taxes.[1] It also displays how much taxes are levied based on current law, and how much would be levied if the payroll tax cap were scrapped.

Salaries which might be interesting to enter into the calculator are:

$31,099: This is an estimate of the median annual earnings of an individual in the US in 2016. (The vast majority of earnings at the level is wage income.)

$200,000: This is the upper limit of income of what former President Obama defined as “middle class,” and assumes that this income is entirely wage income.

$8,900,000: This is the estimated wage income of Larry Fink, CEO of BlackRock Inc., the largest asset management company in the world. It includes $900,000 in salary and $8,000,000 as a bonus, which is a fraction of his total pay package of $25.5 million. (Many high-earners receive a significant part of their compensation outside of wages.) Fink was recently in the news calling for businesses to serve a social purpose. In the past, however, Fink used his power to advocate for privatizing Social Security and mocked the idea of ordinary people retiring at 65. Part of those efforts included serving on the Campaign to Fix the Debt’s steering committee, which journalist David Dayen called a “stalking horse” for “reforms” to cut or privatize Social Security.

[1] It’s important to note that Social Security taxes only apply to wage income and not to other types of income, like investment income. As incomes rise, wage income often becomes eclipsed by investment income — which under current law, is not subject to Social Security taxes.