Article

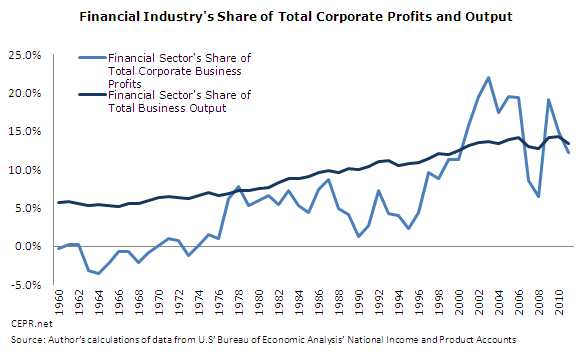

The renewed interest in breaking up too-big-to-fail (TBTF) banks may remind people about the extraordinary influence that banks and financial institutions hold over our economy. The financial industry has experienced substantial growth over the last few decades. The financial sector’s share of corporate output (gross value added less Fed profits[1]) has grown rather steadily from 5.7 percent in 1960 to 14.1 percent in 2006 (see Graph 1). Yet, the financial sector’s share of total corporate profits (net operating surplus less Fed profits) soared from slight losses to 22 percent (corresponds to an increase of $142 billion in 2006) in the same timeframe. This increase in finance’s share of profits far exceeded its gain in the share of corporate production. In the years leading up to the financial collapse (2001-2006), the financial industry enjoyed profits that were hugely disproportionate to their share of output. The disparity between the share of profits and production peaked in 2003 at a difference of 8.3 percentage points. The financial sector’s share of total corporate business profits has been very erratic over the last few decades with a general upward trend, contrasting to a more gradual increase for its share of output. It is important to remember that the high pay and bonuses of top executives and traders, which can run into the millions or tens of millions a year, do not count as profits.

Graph 1

(Click for a larger version)

The growth in the size of the financial industry provides an interesting juxtaposition to the growing inequality over the last few decades. Between 1970 and 2006, the bottom 40 percent of households’ share of aggregate income fell by almost 3 percentage points while the shares of the top 20 percent and 5 percent rose 7 and 6 percentage points, respectively. Many of the highest incomes were earned in the financial sector. (The pay of top executives and traders are counted as wages rather than profits in the National Income Accounts.)

When toxic assets threatened the operations of those prominent banks and financial institutions, bailout funds provided them liquidity. The total amount lent at below market interest rates was well over $10 trillion; although most of the loans were relatively short-term. These subsidized loans enabled the financial sector to return to its pre-recession profit levels by 2009. In contrast, American households are still recovering from income shocks, unemployment stints and wealth shocks.

This is the sort of bailout that is the basis of the TBTF subsidy to the largest firms in the sector. The assumption is that if the largest banks or non-bank financial institutions are in jeopardy of failing, the government will provide them with the money needed to stay afloat as was the case in 2008-2010.

CEPR’s Dean Baker and Travis McArthur initially explored various low- and high-cost estimates of this TBTF subsidy. In an IMF working paper, Kenichi Ueda and Beatrice Weder di Mauro concluded that the subsidy was approximately 0.8 percent for post-2009. Multiplied by the liabilities of the ten largest banks (by assets) in the U.S, this subsidy approaches $83 billion according to a recent Bloomberg editorial.

This ongoing subsidy (or in some cases, criminal amnesty) for banks and financial institutions confounds most conventional thinking. First, moral hazard issues endanger credit markets and our economy as a whole. Second, the very notion that we must protect the financial sector in order to promote economic growth is misguided. A 2012 Bank for International Settlements’ report found that an oversized financial sector is “detrimental” to aggregate growth in advanced economies like the U.S. Similarly, a study from the University of California showed that real (nonfinancial) sectors were adversely affected by financial contractions, but experience little benefits from financial expansions. This appears to be the case for the most recent financial collapse as we can see from the numbers that the financial sector has made a recovery to their pre-recession profit and production levels while much of the economy continues to struggle.

[1] Without consistent data, the author subtracted the average share of the Federal Reserve Bank’s profits as a percentage of GDP between 2000 and 2005 from the profit and production calculations (thus leaving the Fed’s operating expenses, which are minimal).