October 28, 2016

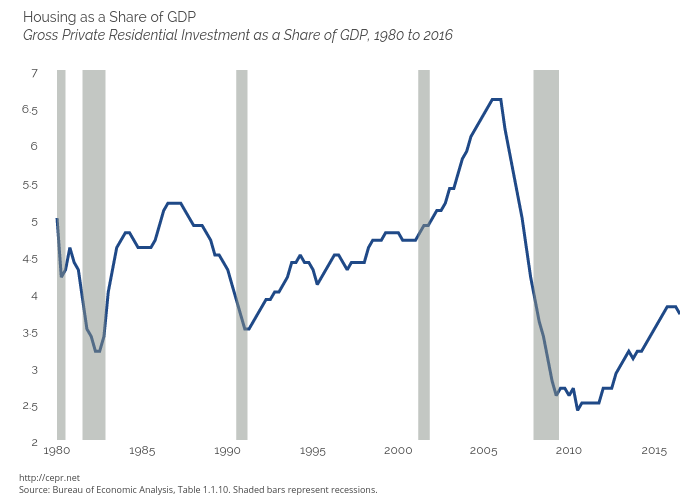

Residential investment fell at a 6.2 percent annual rate, its second consecutive decline. Residential investment now stands at 3.7 percent of GDP, close to its average for the decade prior to the housing bubble. While it may increase somewhat from this current level, the difference from the bubble peak of more than 6.5 percent and its current level creates a gap in aggregate demand of more than $500 billion. This is not easily filled. For more, read the latest GDP Byte.