February 28, 2019

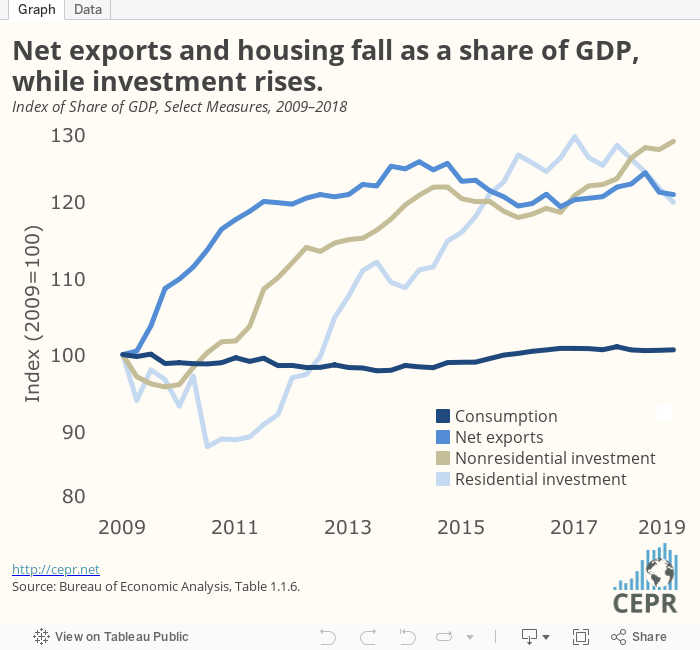

Housing continues to be a drag on growth, declining at a 3.5 percent annual rate, the fourth consecutive quarter of decline. This drop is likely to continue into 2019, given the weak data on December starts reported yesterday. Trade also continues to be a drag on growth, as the deficit rose again in the fourth quarter. Net exports subtracted 0.22 percentage points from growth in the quarter. For more, check out the latest GDP Byte.