April 26, 2019

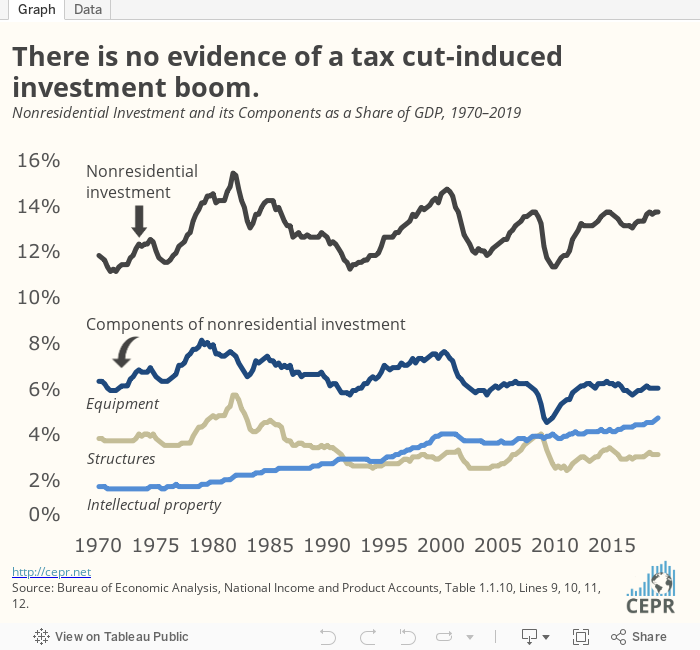

The performance on investment has been notably weak over the last year, growing at a modest single-digit rate. The administration’s projections of the impact of its tax cut imply growth in the neighborhood of 30 percent. We clearly are not seeing anything like this. For more, read the latest GDP Byte.