February 3, 2017

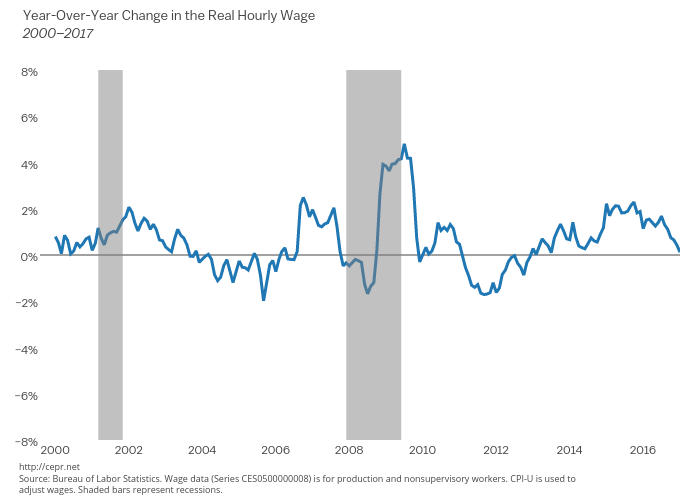

Real wage growth for production and non-supervisory workers has been positive for the last three years of the Obama administration. The sharp decline in energy prices in 2014 and 2015 produced healthy gains for those years of more than 2.0 percent. The pace of real wage growth has slowed as energy prices stabilized in the last year, but real wages are still going up even if not very fast. For more, see the latest Jobs Byte.