March 8, 2019

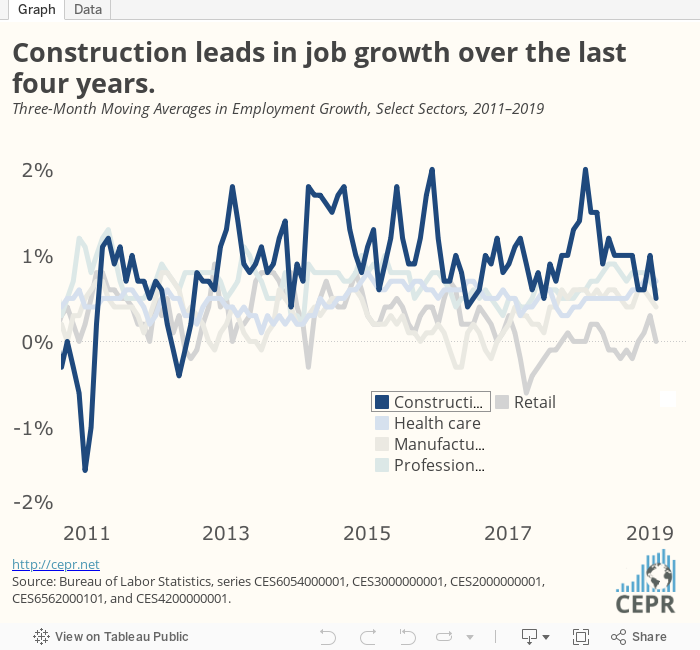

Construction employment fell by 31,000 in February after rising by 53,000 in January. While part of this drop is almost certainly a result of January’s strong number, there is evidence of weakening in both residential and non-residential construction. Mining lost 2,800 jobs, the largest drop since August of 2016, as the drop in world oil prices seems to be taking a toll. For more, check out the latest Jobs Byte.