Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

April 30, 2010 (GDP Byte)

By Dean Baker

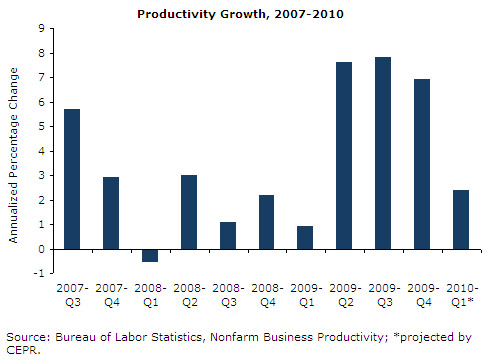

Productivity growth will be close to 2.4 percent for the quarter.

The first increase in inventories since the first quarter of 2008 raised GDP growth in the first quarter of 2010 to 3.2 percent. The 33.1 billion annual rate of accumulation added 1.6 percentage points to growth. Final demand in the first quarter grew at a 1.6 percent annual rate, almost the exact same rate as for the prior two quarters.

Consumption grew at a 3.6 percent annual rate, adding 2.55 percentage points to GDP growth. Car purchases were a big part of this story, adding 0.79 percentage points to growth for the quarter. Consumption of non-durable goods and services grew at 3.9 percent and 2.4 percent annual rates, respectively. This rise in consumption was associated with a decline in the savings rate from 3.9 to 3.1 percent.

While many analysts have portrayed consumers as being pessimistic, this is an extremely low savings rate by historical standards. With house prices resuming their decline, more homeowners are likely to recognize the loss of wealth associated with the collapse of the housing bubble. As a result, it is more likely that the savings rate will go higher than lower.

Construction of non-residential structures fell at a 14.0 percent annual rate, continuing a decline that began in the third quarter of 2008. It is likely that output in this sector will decline further, at least through 2010, given the enormous overbuilding in the sector. Investment in equipment and software grew at a respectable 13.4 percent annual rate, which was down somewhat from the 19.0 percent rate in the fourth quarter. Spending on software added 0.36 percentage points to GDP growth for the quarter. Non-residential investment as a whole added 0.38 percentage points to GDP growth.

Housing construction dropped at a 10.9 percent rate, following two consecutive quarters of growth, subtracting 0.29 percentage points from GDP. Given the current slow pace of construction, it is likely that there will be some uptick in housing, although probably not enough to have a substantial impact on growth.

Trade is again turning into a big subtraction from growth as the growth in imports far exceeds the growth in exports. Exports grew at 5.8 percent annual rate, adding 0.66 percentage points to growth, while imports grew at an 8.9 percent rate, subtracting 1.28 percentage points from growth, leaving a net effect of trade of –0.61 percentage points. Greece’s troubles have produced a flight to the dollar, raising its value against the euro and other currencies. This is likely to contribute to further increases in the trade deficit through the rest of 2010.

The state and local budget crises are leading to sharp cutbacks in spending. The state and local sector contracted at a 3.8 percent annual rate, subtracting 0.48 percentage points from growth in the quarter. Most of the cutbacks were in investment spending, which fell at a 14.7 percent annual rate. Governments apparently are opting to deal with their budget squeezes by putting off capital expenditures in order to continue to provide current services. This may be the best option at present, but in the long-term this pattern of cutbacks will slow the growth of productivity. Federal spending grew at a 1.4 percent rate, but the government sector as a whole subtracted 0.37 percentage points from growth in the quarter.

There is little reason to expect that final demand will pick up substantially from its current rate of growth. The savings rate is unlikely to decline further, which means that consumption growth will be weak, and non-residential construction, state and local government spending and foreign trade are all likely to be substantial drags on growth. If the rate of inventory growth stabilizes, then this would imply GDP growth of close to 2.0 percent, which is not enough to generate jobs.

The “positive” side of this report is that analysts who feared that rapid productivity growth was preventing job growth now have less to worry about. Output in the non-farm sector grew at a 4.4 percent annual rate. With hours having risen at close to a 2.0 percent rate, this implies a modest 2.4 percent rate of productivity growth for the quarter. The prior uptick in productivity was typical for the end of a recession and now it appears that growth has returned to normal levels.