Article • Expose the Heist: Power and Policy in Unprecedented Times

Don’t Believe the Ads! Medicare Advantage Propaganda

Article • Expose the Heist: Power and Policy in Unprecedented Times

Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

In recent weeks, supporters of Medicare Advantage (MA) have paid for misleading and patently untrue advertisements about the program. In the greater District of Columbia area – home to many federal workers, congressional staff members, and key stakeholders who impact policy – waves of advertisements have falsely pushed the narrative that MA is more cost effective than traditional Medicare.

A key group behind these advertisements is the Taxpayers Protection Alliance (TPA), a 501(c)(4) nonprofit organization. As the Internal Revenue Service defines them, these are tax-exempt nonprofits that serve the primary purpose of promoting “social welfare” rather than profit. These organizations can also lobby government officials and are conduits for dark money, an unofficial term for political spending made to influence elections and/or public policy that the spenders do not publicly disclose. Accordingly, the funders of TPA are private.

The TPA exists alongside the Taxpayers Protection Alliance Foundation (TPAF), a research group which is a 501(c)(3) charitable organization that cannot engage in lobbying as a substantial part of its operations. The TPA describes its mission as holding “politicians accountable for the effects of their policies on the size, scope, efficiency and activity of government and offer real solutions to runaway deficits and debt.” However, its recent blitz of Medicare Advantage advertisements does the opposite.

TPA advertisements claim that Medicare Advantage saves taxpayers $144 billion over 10 years compared to traditional Medicare. The $144 billion comes from an industry study conducted by insurance company Elevance Health, which offers MA plans and happens to be where the study authors work. The analysis suggests anywhere between $59-$144 billion in decade-long savings.

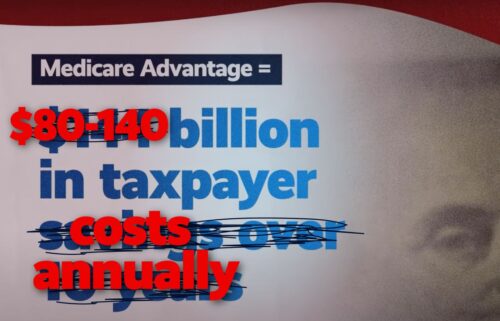

Yet, the government’s Medicare Payment Advisory Commission (MedPAC) – which officially supports the MA program – has repeatedly documented that MA has never saved taxpayers money compared to traditional Medicare. In fact, MedPAC estimated that insurance companies in the MA program will receive $84 billion in overpayments just in 2025. MedPAC estimates are consistent with other analyses by independent experts. Estimates of MA overpayments have ranged from roughly $80 billion to as high as $140 billion annually.

The ads falsely claim that traditional Medicare is rife with waste, fraud, and abuse due to improper payments that are supposedly “twice as likely” in traditional Medicare than MA. In Fiscal Year 2024, traditional Medicare had an improper payment rate of 7.66% compared to 5.61% in MA. 7.66% is not twice the rate of 5.61% – although the absolute improper payment amount is 1.66 times more in traditional Medicare than MA ($31.7 billion versus $19.07 billion). More importantly, improper payments are largely not due to fraud. According to the Centers for Medicare and Medicaid Services (CMS):

The vast majority of improper payments occurred in situations where a reviewer could not determine if a payment was proper because of insufficient documentation from a state, provider, or the Medicare Advantage Organization (MAO). While fraud and abuse are one cause of improper payments, not all improper payments represent fraud or abuse. Improper payment estimates are not fraud rate estimates.

The advertisements also state that Medicare Advantage companies provide more benefits at lower costs. While it’s true that most MA plans offer supplemental benefits (such as coverage for vision, dental, and hearing care) that traditional Medicare does not, taxpayers pay at least $80 billion more annually for the MA program than if everyone were in traditional Medicare – so it does not lower costs overall.

MedPAC itself cannot verify the quality of these benefits at all, and some publicly available information suggests the benefits are quite poor. For example, a 2023 article in Health Affairs analyzed a sample of nearly 100,000 adults, finding that Medicare Advantage enrollees did not use dental services more than seniors in traditional Medicare. MA plans that offer dental coverage commonly provide high coinsurance rates of 50% for expensive procedures (ex: dental fillings) and even low caps on how much insurance will spend annually to cover someone’s care ($160 on average in 2021).

Additionally, the lack of vision, hearing, and dental coverage in traditional Medicare is a policy choice that can change. Overpayments to the MA insurance companies like United Healthcare are sufficient to pay for comprehensive vision, dental, and hearing care coverage in traditional Medicare.

In its advertisements, TPA also claims that Medicare Advantage leads to better health outcomes. The MA program functions by giving capitation or lump sum payments to insurance companies per patient based on their risk level. These companies – predominantly UnitedHealthcare, Humana, Blue Cross Blue Shield, and Aetna/CVS – profit by spending as little as possible on patient care. Theoretically, this system incentivizes them to keep patients as healthy as possible, but there is not robust evidence to support this claim.

As the Kaiser Family Foundation (KFF) found in 2022 through examining 62 different studies, there is not strong evidence that enrolling in Medicare Advantage makes patients achieve significantly better health outcomes. There is no randomized study – the gold standard to determine causality – where patients randomly sorted into the MA program achieve better health outcomes (higher life expectancy, lower cancer rates, etc.). Instead, researchers conduct observational analyses, which are not strong methods to determine causation. Although, it would be difficult for researchers to ethically conduct a study randomly sorting patients into MA or traditional Medicare.

KFF noted that MA plans push their patients to more preventative care visits and they have lower hospital readmission rates. The former aligns with the financial incentives that MA insurers have. But the differences between patients that choose to use MA versus traditional Medicare mean that it’s not possible to conclude that MA actually causes lower hospital readmissions.

KFF also pointed out that traditional Medicare patients tend to receive care in the higher-rated cancer facilities, nursing facilities, and home health agencies. As traditional Medicare reimburses providers more than Medicare Advantage, many doctors and providers have declined to accept MA patients. Given this reality, and that 98 percent of non-pediatric doctors accept traditional Medicare patients, it makes sense that traditional Medicare patients are able to go to more expensive, high-quality providers.

Another key aspect of Medicare Advantage that does not exist in traditional Medicare is the restriction, delaying, and denial of care that is inherent to MA’s managed care model. In 2023, physicians filed over 50 million prior authorization (PA) requests for MA patients (almost two per enrollee) where the insurance companies ultimately denied 3.2 million (6.4 percent). While most claims got accepted, physicians have voiced how PAs delay care, as 93 percent of 1,000 physicians in a 2024 American Medical Association survey reported that PAs sometimes (36 percent), often (42 percent), or always (15 percent) delayed access to necessary care.

Additionally, 11.7 percent of denied PA requests got appealed, with insurers overturning 81.7 percent – meaning that more than eight in ten denied requests that physicians/patients chose to appeal were incorrectly denied. The overturn rate has been consistently above 80 percent from 2019-2023.

While TPA advertisements are pushing insurance company propaganda under the guise of “protecting” Medicare Advantage, it’s not clear what the threat to the program would be. The Trump Administration recently more than doubled the payment rate increase to insurance companies in Medicare Advantage for 2025 from what the Biden Administration had proposed.

Why would an organization dedicated to curbing government spending want to protect a program that wastes billions of dollars? MA has never saved taxpayers money and costs anywhere from $80 billion to $140 billion in overpayments. If TPA truly wants to rein in waste, fraud, and abuse, then it should advocate against ripping off hardworking taxpayers by shoveling tens of billions of their dollars to giant health insurance companies.

Article

Article

Article

Article

Article

Article

Article

Article