Article

Workers Should be Wary Now that Private Equity Is Going Retail

Article

Fact-based, data-driven research and analysis to advance democratic debate on vital issues shaping people’s lives.

Center for Economic and Policy Research

1611 Connecticut Ave. NW

Suite 400

Washington, DC 20009

Tel: 202-293-5380

Fax: 202-588-1356

https://cepr.net

Eight years after passage of the 2013 JOBS Act that let private equity firms market directly to individuals to solicit their investments, retail investors – largely high net worth individuals – finally account for a significant share of assets under management (AUM) at some of the largest PE firms. Apollo claims to be “among the largest providers of alternative asset services in the retail marketplace,” according to Marc Rowan, a co-founder of Apollo Global Management. Retail investors account for about 16 percent of the Blackstone Group’s $619 billion AUM. Ares Management Corporation has identified retail as a major area of focus.

Private equity made no secret in 2014 that it was coming after people’s nest eggs. It planned to target individuals with a net worth of $5 million or more and workers’ retirement savings – 401(k)s and IRAs, a major untapped source of funds. By 2015, Carlyle, KKR and Blackstone were at the forefront of this move. David Rubinstein – Co-Founder and, at the time, Co-CEO of Carlyle – predicted that sovereign wealth funds and wealthy individuals would be important in funding private equity from 2015 to 2025.

Targeting workers’ retirement savings proved more difficult than marketing to the wealthy. President Obama’s Department of Labor resisted efforts by PE firms to allow high fee, high risk investments in 401(k) retirement plans. But the lure of access to the $6.2 trillion in these accounts did not diminish for private equity. And in June 2020, President Trump’s Labor Secretary, acting on the President’s instructions to “remove … barriers to economic prosperity,” set aside traditional concerns about the suitability of risky investments for workers’ retirement savings and issued a letter that allows investments in private equity to be included in these accounts. Workers’ retirement savings, which had been off limits to private equity, are now fair game for PE firms.

In the last few years, private equity firms have focused on the challenge of developing financial products geared to the needs of wealthy individuals who, typically, cannot afford to tie up their funds for 10 years, as is common for institutional investors such as pension funds and university endowments. And PE firms needed to develop financial products that required smaller financial commitments than the multimillion contributions that institutional investors make to PE funds. In a way, this has served as a dry run for PE to get its hands on workers’ retirement savings: workers must be able to withdraw their retirement savings as needed and to make relatively small investments in private equity.

So, what are these new financial products? After a few false starts, PE firms developed new strategies for accessing smaller investments. In one popular strategy, PE firms buy an insurance company and then market customized annuities to clients. Other strategies involve establishing a publicly-traded company – a Business Development Corporation or Real Estate Investment Trust – in which the PE firm owns nearly all of the stock and then recruits individuals as investors.

So-called “interval funds” are another popular strategy. These funds accept investments on a continuous basis. Unlike typical private equity funds, they have no end date by which assets will be liquidated and final distributions made to investors. Interval funds allow investors to redeem a portion of their investment at regularly scheduled intervals – typically quarterly or annually. This provides less liquidity than a mutual fund, which allows redemptions daily, but more liquidity than a standard PE fund. Interval funds can tie up 75 to 95 percent of assets in illiquid investments such as private equity, venture capital, or hedge funds. Investors are permitted to redeem between 5 and 25 percent of their shares at the stated intervals. The fund may not have sufficient liquid assets to honor all redemption requests, and investors may not be able to redeem as many shares as they would like. For this reason, the investments are considered illiquid by regulators, although they are marketed to individual investors as offering the advantages of more liquid assets. There are no legal requirements for investors, but most PE firms currently market them to individuals able to invest at least $250,000. Interval funds are marketed to retail investors as a way to gain access to companies owned by private equity and venture capital funds not otherwise available to them. Retail investors are promised high returns from access to companies owned by private investment funds, including an illiquidity premium, that raises returns above stock market gains.

All of these strategies – marketing annuities to wealthy individuals, selling stock in publicly-traded companies in which PE firms own nearly all the shares, and recruiting investors for PE-sponsored interval funds – offer an important advantage to PE firms. They provide them with a welcome source of permanent capital from long-term investors and reduces their reliance on 3- to 4-year cycles of fund raising from institutional investors.

For retail investors, the high fees associated with investments in interval funds may undermine the promised high returns. Andrew Park, a researcher at Americans for Financial Reform, offers the example of an interval fund set up to receive investments as small as $50,000 – more than most working families can afford, but not beyond the ability of some workers to roll over from their retirement accounts. This may offer a preview of what workers can expect if PE products are included in their retirement accounts.

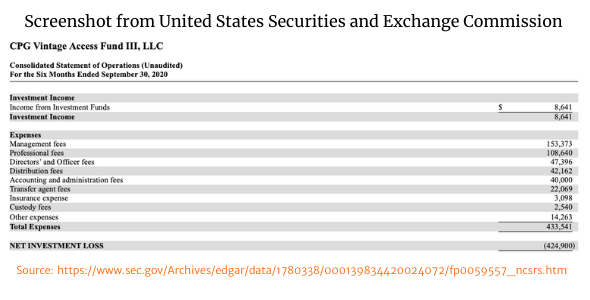

Central Park Group specializes in selling stakes in hedge funds and private equity funds to investors for a $50,000 minimum. So far, they have put investors into funds managed by Blackstone, KKR, Carlyle, Warburg Pincus, and Brookfield. The firm’s CPG Vintage Access Fund III is fairly new, so investment income is likely to increase going forward. But recent reports filed with the Securities and Exchange Commission for the first three months of 2020 and the next six months to September 30 of that year do not look promising. The reports show that the fund had $8,641 in investment income against $1,153,009 in fees collected over the 9-month period in 2021. Fees accrued in the six months from April 1 to September 30 came to $433,541, as shown in the screen shot of their SEC filing. Almost $720,000 in fees was collected in the first quarter of 2021.

The list of fees charged to the small investors in the CPG Vintage Access fund is daunting: Organizational expenses, professional fees, management fees, officer and director fees, accounting and statement fees, transfer agent fees, insurance expense, and custody fees. Even if investment returns increase in the future, as is likely, these fees will cut deeply into the returns earned by retail investors, leading to disappointing and possibly disastrous results.

The list of fees collected from retail investors should serve as a cautionary tale for workers considering opening up their 401(k)s and IRAs to private equity and hedge fund investments. The Secretary of Labor’s June 2020 letter making these investments possible acknowledged the “potential cost, complexity, [lack of] disclosure, and liquidity issues” these investments pose, but noted that they “often provide strong returns,” meaning there is no guarantee. Indeed, net of fees, the returns for the typical PE fund launched since 2006, properly measured, have tended to match the stock market’s returns with little to no premium for the lack of liquidity on other added risk. About half the funds launched in each year since then have underperformed the stock market. Indeed, there is concern among PE funds and the brokers that advise 401(k) plans that they may be sued if workers’ retirement accounts plummet unexpectedly. Workers should be very wary of these investments.