Article • Expose the Heist: Power and Policy in Unprecedented Times

Private Equity is Breaking out the Champagne. What Do They Know That We Don’t?

Article • Expose the Heist: Power and Policy in Unprecedented Times

President Trump’s August 7 Executive Order (EO), Democratizing Access to Alternative Assets, raised the possibility that the nearly $9 trillion in workers’ 401(k) accounts could be used to bail out struggling private equity funds. This looked like a slam dunk for an industry that has lobbied hard for this policy change. But the real story might be hiding in the fine print.

For more than three years, these investment funds have found it challenging to make good on their promise to pension funds and other investors to show a profit and return cash to them. Access to workers’ retirement savings would save the struggling PE industry, and they are looking to the EO to open wide retirement funds that they have mostly been denied access to.

First, it’s important to understand the backstory: On June 3, 2020, the Trump Administration Department of Labor (DOL) issued an Information Letter making private equity (PE) investments available to participants and beneficiaries in 401(k) plans. The Information Letter explicitly recognized that employers still had the fiduciary duty to ensure that these investments were made in the best interest of participants and beneficiaries. In December 2021, though, the Biden administration DOL issued a supplemental statement which noted that, except in a few cases, employers and other plan fiduciaries of small 401(k) plans lack the skills necessary to evaluate PE retirement assets.The Supplemental Statement further noted that an employer or other plan fiduciary was still subject to the prudence requirements in the Employee Retirement Income Security Act of 1974 (ERISA) that apply to the selection and monitoring of investment assets, investment managers and investment advice service providers.

Trump’s EO instructs the Secretary of Labor to consider rescinding Biden’s cautionary guidance on private equity investments in workers’ retirement accounts. On August 12, to great celebration by private equity and other alternative asset firms, the Labor Secretary did just that. PE investments in workers’ 401(k)s as part of a professionally managed, suitably diversified Target Date fund, is once again acceptable under ERISA.

But despite the PE industry hoopla, this is likely to lead to at most a small increase in investment in private assets, as employers continue to be wary of fiduciary liabilities and lawsuits challenging high fee investments that eat into returns.

The EO instructed the Labor Secretary to develop rules consistent with ERISA that would make it possible to include a wider array of private market investments as well as real estate, commodities, infrastructure, and crypto in employees’ retirement savings. The Secretary is also instructed to create a description of appropriate investment opportunities for including these assets in retirement accounts. The Secretary has 180 days to complete these tasks. We can expect to see a flurry of announcements from the Labor Department between now and early February.

But as many observers are well aware, all this will have little effect expanding access to alternative investments in workers’ 401(k)s unless employers can be granted safe harbor against legal suits by employees disappointed with high fees and lackluster returns. To address this, the Trump EO instructs the Labor Secretary to “prioritize actions that may curb ERISA litigation that constrains fiduciaries’ [employers] ability to apply their best judgment in offering investment opportunities to relevant plan participants [workers].”

ERISA sets a high bar for fiduciary responsibility of employers, and includes strong protections for the interests of workers. It may not be possible to water these down enough to provide employers with the protections they need to feel comfortable making alternative assets available to their employees. Anticipating this potential difficulty, the EO also instructs the Labor Secretary to “consult with the Secretary of the Treasury, the Securities and Exchange Commission (SEC), and other Federal regulators as necessary to carry out the policy objectives of this order, including as to parallel regulatory changes that may be incorporated by such other Federal regulators.”

Still, even taking all of these measures may not be sufficient to fundamentally weaken employers’ fiduciary responsibility for investments by employees. The president and lobbyists for PE and crypto have pushed to persuade workers that they should have the same right as pension funds and wealthy individuals to include high risk, high return financial assets in their 401(k)s. But reluctance of employers may mean that alternative investment assets capture a trickle and not a flood of the nearly $9 trillion in workers’ retirement accounts that the private equity, crypto and other alternative investment firms have been eyeing so eagerly.

Why, then, is there so much excitement about the president’s EO?

A little-discussed paragraph in the EO may hold clues to this. The president directs the SEC to “consider ways to facilitate access to investments in alternative assets by participants in participant-directed defined-contribution retirement savings plans” – that is, in Individual Retirement Accounts, or IRAs (emphasis added). “Such facilitation,” the EO continues, “may include, but not be limited to, consideration of revisions to existing SEC regulations and guidance relating to accredited investor and qualified purchaser status.” This is something the SEC can do. The current SEC requirements for an individual to be deemed an accredited investor and allowed to invest in risky assets is an annual income of $200,000 a year ($300,000 for a married couple) plus a net worth of a million dollars, not counting the home they live in.

These income and wealth standards are designed to protect the retirement savings of individuals who cannot absorb potential losses associated with risky investments without endangering their retirement nest egg. Removing those guidelines may result in great harm to the living standards of workers with IRAs when they retire. Since passage of the Dodd-Frank Act in 2010, individuals with specific knowledge of finance have been awarded accredited investor status even if they don’t meet the financial requirements.

Lawmakers have been making other moves to expand the reach of risky investing. In late July 2025, the House of Representatives unanimously passed the Equal Opportunity for All Investors Act, which directs the Securities and Exchange Commission (SEC) to allow all individuals to take a test that would qualify them to be ‘accredited investors’ and enable them to invest in private equity, hedge funds, and other alternative assets without meeting the income and wealth requirements.

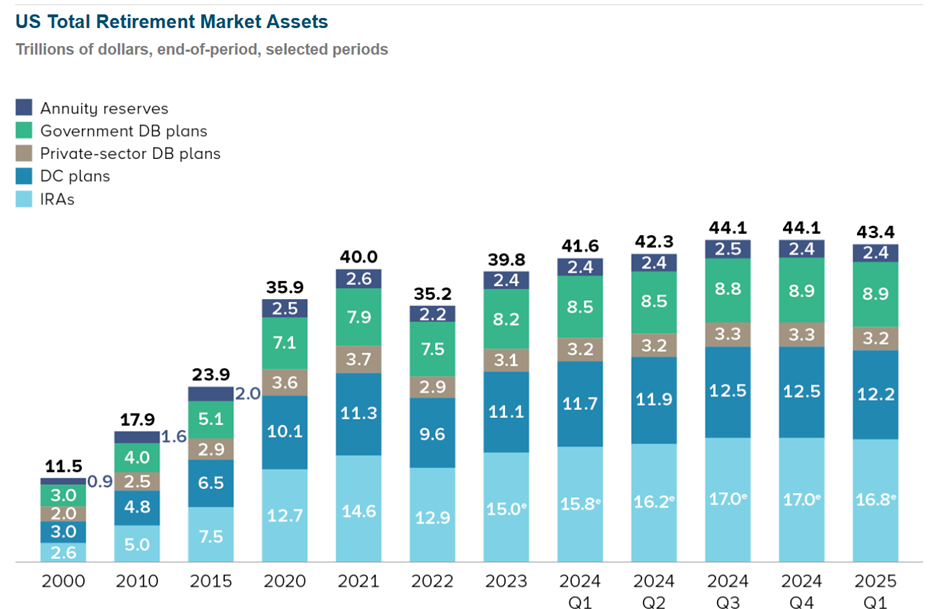

So could this be what the alternative investment funds are so happy about? This chart, from the Investment Company Institute shows the trillions of dollars in retirement market assets by asset class:

Individual retirement accounts (IRAs) hold $16.8 trillion, compared to $12.2 trillion in all direct contribution (DC) plans of which 401(k)s hold $8.9 trillion. Is it the $16.8 trillion in IRAs that is the real pot of gold that the alt investment industry has its eye on, the real point of the EO?

Is all the talk about boosting workers’ retirement income a cover to generate enthusiasm for risky high-fee investments? Will a fear of missing out on something big be enough to encourage individuals with IRAs to make these investments?

We won’t know the answer until February 7, 2026. But it is a plausible explanation for all the partying as the EO moves forward. A claim on retirement riches that doesn’t involve exposing employers to fiduciary liabilities may well be attractive to PE and other investment funds seeking to attract investors. And around the edges, there will be employers that make investments in alternatives accessible to their employees, allowing President Trump to take credit for enabling ordinary workers to invest like pension funds and wealthy people.

Article

Article

Article

Article

Podcast

Article

Article

Testimony