February 24, 2010

February 24, 2010 (Housing Market Monitor)

By Dean Baker

The 30-year mortgage rate will likely rise to at least 5.5 percent by the end of the year.

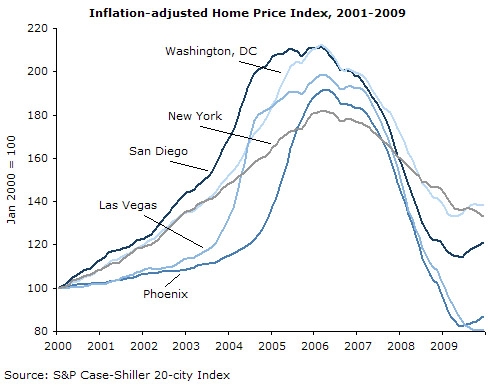

The seasonally adjusted Case-Shiller 20-city index again showed a modest 0.3 percent rise in December. This index has risen at a 3.2 percent annual rate over the last quarter, although it is down by 3.1 percent over the last year. There appears to be a growing divergence in price trends in recent data with the three California cities in the index (San Diego, San Francisco and Los Angeles) and Phoenix all seeing price increases of more than 1.0 percent in December. In contrast, prices in Chicago fell by 0.6 percent and in New York by 0.5 percent.

The seasonally adjusted Case-Shiller 20-city index again showed a modest 0.3 percent rise in December. This index has risen at a 3.2 percent annual rate over the last quarter, although it is down by 3.1 percent over the last year. There appears to be a growing divergence in price trends in recent data with the three California cities in the index (San Diego, San Francisco and Los Angeles) and Phoenix all seeing price increases of more than 1.0 percent in December. In contrast, prices in Chicago fell by 0.6 percent and in New York by 0.5 percent.

Over the last three months, prices in Phoenix rose at a 17.3 percent annual rate and in San Francisco at a 16.3 percent rate. The annual rate of increase in Los Angeles over this period was 14.5 percent and 14.0 percent in San Diego.

Prices fell at a 9.2 percent annual rate in Chicago over this three-month period and by 6.8 percent in New York. Tampa also saw a sharp price decline with prices falling at a 7.6 percent rate over the last three months.

The bottom third of the market continues to substantially out-perform the rest of the market in the tiered indexes, indicating that the first-time buyers tax credit is likely a major factor in the recent price increases. In San Diego, prices of homes in the bottom tier rose at a 27.4 percent annual rate over the last quarter, while they rose at a 27.0 percent rate in Los Angeles. In San Francisco, prices in the bottom tier rose at a 24.4 percent rate. By contrast, prices in the top tier in these three cities rose at 8.5 percent, 7.0 percent, and 13.4 percent annual rates, respectively.

In Phoenix, the prices of homes in the bottom tier rose at an incredible 51.0 percent annual rate over the last quarter. Prices in the top tier rose at just a 7.7 percent rate. This surge of prices in the bottom tier in Phoenix likely also reflects action by investors taking advantage of the plunge in prices. At their low in April of last year, prices for homes in the bottom tier had fallen by 70 percent from their peak in May of 2006, and were only slightly higher in nominal terms than they had been in June of 1995. With sale prices falling sharply relative to rents over this period, the bottom tier in the Phoenix market would have offered attractive opportunities to investors.

Going forward, there continues to be substantial grounds for questioning whether this price recovery will be sustained. The Federal Reserve Board appears likely to go through with plans to end its purchase program for mortgage-backed securities at the end of March. This will almost certainly cause the 30-year mortgage rate to rise to at least 5.5 percent by the end of the year.

More importantly, the renewal of the expanded first-time buyers tax credit is scheduled to expire at the end of April. Given the surge in sales in September and October, there can be little doubt that the initial credit boosted demand, which is also reflected in the sharper price increases in the bottom tier of the housing market in most cities. (The credit is larger relative to house prices in the bottom tier and these houses are also more likely to be bought by first-time buyers, so it would be expected that the largest impact shows up in this segment of the market.) The paring back of loans guaranteed by the Federal Housing Authority will also be a factor reducing demand in 2010, especially at the bottom portion of the market.

Interestingly, demand for new mortgage applications has continued to be extremely low following the expiration of the original tax credit. It has been consistently running below the very depressed 2009 levels through January and into February. This is consistent with many buyers having moved their purchases forward to take advantage of the initial tax credit that was expected to expire at the end of November. The implication would be that demand will be especially weak in 2010 and therefore that prices are likely to soon resume their decline.