March 31, 2010

March 31, 2010 (Housing Market Monitor)

By Dean Baker

Mortgage applications are running below the depressed levels of 2009.

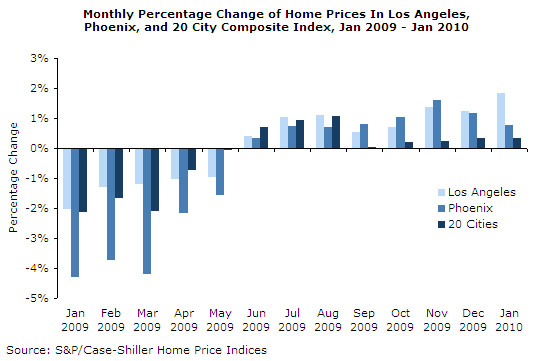

The Case-Shiller index showed house prices continuing to rise at a modest pace in January, with the 20-city index rising by 0.3 percent. Over the last quarter, the index has risen at a 3.2 percent annual rate. The index is almost flat over the last year, down by just 0.7 percent.

There are sharp differences in the price movements across the cities in the index. Eight of the 20 cities showed price declines. The sharpest drop was in Chicago, where prices fell 0.8 percent. Prices in Seattle dropped 0.6 percent, while prices in both Atlanta and Portland fell by 0.5 percent. Over the last three months, prices in Chicago have fallen at an 8.5 percent annual rate. The annual rate of decline in Seattle over the last three months was 0.7 percent, and in Atlanta, 1.3 percent. Prices in Portland rose at a 3.0 percent rate.

On the other side, the biggest rises in price were in the West. Prices in Los Angeles rose by 1.8 percent in January, by 0.9 percent in San Diego, and 0.8 percent in Phoenix. Over the last three months, prices in these cities have risen at 19.4 percent, 13.2 percent, and 15.0 percent annual rates, respectively.

These cities are at very different points in the process of bubble deflation. Over the last year, prices have fallen by 4.5 percent in Phoenix. This puts house prices in the area below their February 2002 level. They are 3.8 percent and 5.9 percent above their year ago level in Los Angeles and San Diego, respectively. Prices in both cities are down sharply from their bubble peaks, but are still 74.0 percent and 58.9 percent above their levels 10 years earlier.

The bottom tier of houses continues to sustain prices in most cities. In San Diego and Phoenix, prices for homes in the bottom third of both markets rose by 1.7 percent in January. They have risen at a 24.7 percent and 42.2 percent annual rate over the last three months, respectively. Prices for homes in the bottom tier in Los Angeles rose by 1.8 percent in January and have risen at a 28.0 percent annual rate over the last quarter. Prices for homes in the bottom tier rose by 2.9 percent in Minneapolis and have risen at a 45.7 percent annual rate over the last quarter. The relatively faster increase in house prices for lower-end homes is consistent with the first-time buyers’ tax credit having a substantial impact on prices, since the $8,000 credit is a much larger share of the sale price for homes in the bottom third of the market.

The purchase mortgage applications index increased by 6.8 percent last week, rising to its highest level since the end of October. This is likely attributable to efforts to buy homes before the expiration of the extended homebuyers credit at the end of April. It is remarkable how little activity seems to have been supported by this credit. Even with last week’s jump, applications were still 9.3 percent below their year ago level.

There is virtually certain to be somewhat of a surge in home buying over the next month. Anyone who qualifies for the credit and is considering buying a home in 2010 has a substantial incentive to sign a contract before the expiration date on the credit. However, this means that the sales rate in subsequent months will be considerably lower as sales will have been pulled forward. The sales rate was already very low in the first three months of the year.

Given the natural rate of turnover in the housing market, and the large number of homes coming on the market due to foreclosures and distressed sales, in all likeliehood there will be a glut of supply later in the year. At the same time, the end of the Fed’s program of purchasing mortgage-backed securities is likely to push interest rates higher, which will further depress demand. This should lead to a renewed decline in prices. Prices still have another 10-15 percent to fall before returning to their long-term trend level.