December 22, 2010

Initiated in late 2007, the Term Auction Facility (TAF) was the first of the Federal Reserve’s many liquidity facilities intended to stem a financial collapse by providing financial institutions with emergency funding. The TAF was intended to alleviate some of the stigma on Wall Street against borrowing from the central bank’s discount window. The program was structured to provide low-interest, short-term loans (set to mature in either 28 or 84 days) to all eligible depository institutions, with investment-grade assets held as collateral. The terms and specific beneficiaries of the facility were kept secret until earlier this month, December 2010, when a Congressional mandate forced disclosure.

We now know that hundreds of banks, both American and foreign-based firms, accessed short-term funding through the Federal Reserve’s program. In cumulative terms, the Fed auctioned off over $3.8 trillion through the TAF, from late 2007 to early 2010. The top ten participating institutions at the TAF accounted for nearly $1.8 trillion – or nearly half – of cumulative borrowing from the Fed.

After including recent mergers and acquisitions, Wells Fargo, Bank of America and Barclays were the three largest borrowers through the TAF program. Seven of the top ten participants, in fact, were financial institutions based in Europe. Clearly, there was a strong demand for cash among all institutions during the crisis period of late 2008 and throughout the following year 2009 as well. And many banks found the Fed’s TAF program to be a good option.

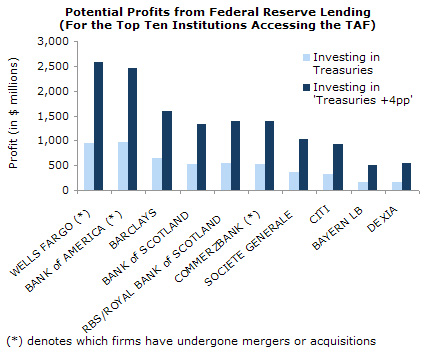

In this analysis, we looked at the effect lending through the TAF program might have had on bank profits. The analysis uses two different scenarios. The first calculated the profits the banks would have earned from Fed lending if they had taken their cash and immediately invested in Treasuries (10-yr T-bills) for the duration of the loan’s maturity. The second scenario assumed the banks invested in assets that yielded a return four percentage points higher than the rates on Treasury bonds. Such assets were not difficult to find at the peak of the crisis.

The analysis indicates (see chart below), all of the top ten borrowers would have earned well over $100 million on the borrowed funds after paying back their loans from the Fed with interest, if they invested solely in T-bills. The top borrowers, Wells Fargo and Bank of America, would have made almost $1 billion under this assumption.

The profits would have been considerably higher if they invested in assets that provided yields 4 percentage points above Treasury bonds. In this scenario, Wells Fargo and Bank of America each would have netted close to $2.5 billion through its participation in the Federal Reserve’s TAF program. Barclay’s would have turned a $1.5 billion profit.

These calculations may help to explain how troubled financial institutions were able to report near-record profits just after a recession precipitated by the collapse of an asset bubble in the housing market. As institutions and markets collapsed, the Federal Reserve may have played a key role, not only in providing emergency liquidity to depository institutions, but also in boosting the quarterly profits for financial firms both in the United States and around the world.