April 24, 2012

April 24, 2012 (Housing Market Monitor)

By Dean Baker

Prices of homes in the bottom tier of the Chicago market are down 55.4 percent from their peak.

Many analysts and reporters have over-reacted to the monthly swings in housing releases such as new and existing home sales and starts. These data are always erratic. Some items, like starts of multi-family units tend to be lumpy. A large number of starts in one month, which can often be related to weather or changes in zoning, will almost inevitably lead to a falloff in the subsequent month.

The falloff in new home sales reported for March should be seen as one of these erratic movements. There was a jump in sales reported for February, primarily due to a rise in sales in the West. This was more than reversed in March, which put sales near the January level.

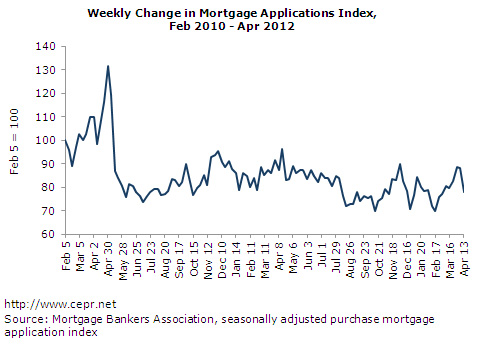

It is always best to try to use averages of several months’ data (as the Case-Shiller index does) and to factor in all the available data on the market. The mortgage application index generally provides a good gauge of the underlying strength of the market. This weekly index is also volatile, but taking a one-or two-month average shows no clear upward trend from year-ago levels. Of course, investors often will not use standard mortgages to finance house purchases, thus insofar as the percentage of investor-purchased homes rises or falls, this will not be picked up by the mortgage application index.

The Case-Shiller 20-City Index rose slightly in February, offsetting a small decline in January. Seven of the 20 cities showed price declines. The largest drop was a 2.0 percent price decline in Atlanta followed by drops of 0.7 percent in Chicago and 0.6 percent in Cleveland.

The bottom tier of the housing market continues to be the hardest hit in Atlanta. Prices in the bottom tier are now down 27.8 percent from their year-ago level and 51.2 percent from the peak reached in the fall of 2009 when the first-time homebuyers tax credit was in effect. Someone who purchased at the peak of the bubble in 2006 has seen their house price fall by 64.3 percent.

The continued weakness in the Chicago market is striking since some have touted the city’s unrestrictive housing policy. Prices overall are down 6.8 percent over the last year. Prices of homes in the bottom tier are down 15.2 percent. Prices in the city overall are down 36.5 percent from their bubble peak, while prices for homes in the bottom tier are down by 55.4 percent.

The weakness in the bottom end of the market also seems to be showing up in Boston and New York, two cities where the overall market has held up reasonably well. Prices for homes in the bottom tier fell by 1.8 percent in February in Boston and by 2.0 percent in New York. For the year, prices in the bottom tier are down by 4.6 percent and 5.3 percent, respectively. Given the sharp declines in recent months, it seems likely there will be further weakness in this segment of the market.

The biggest price increases for the month were a 2.1 percent rise in Phoenix and 1.2 percent increases in both Miami and Minneapolis. All three of these cities have seen rapid price appreciation over the last three months. Phoenix leads the way with a 25.6 annual rate of increase over this period, followed by Miami with an 11.4 percent rate and Minneapolis with a 9.6 percent rate. It is likely that investors are playing a big role in this run-up, especially in the Phoenix market, which was badly depressed.

Home prices in the bottom tier in Phoenix had fallen back to their mid-90s levels last year. They have now risen at a 64.0 percent annual rate over the last three months. It is likely that investor purchases will continue to fuel a rebound in some of the most depressed markets where prices have likely overshot on the downside.

Overall, we are probably entering a period where prices are stabilizing. Air remains in some of the bubble markets, but price declines in these markets are likely to be offset by increases in the markets where prices overshot on the downside.