April 30, 2014

April 30, 2014 (GDP Byte)

As a result of the ACA, heath care spending rose at a 9.9 percent annual rate in the quarter.

The rate of GDP growth slowed to just 0.1 percent in the first quarter, largely as a result of sharp reversals in spending on exports and investment in equipment. In the fourth quarter, exports had grown at a 9.5 percent annual rate adding 1.23 percentage points to fourth quarter growth. Equipment investment rose at a 10.9 percent rate adding 0.58 percentage points to growth.

Both figures were extraordinarily high. Fourth quarter export growth was the highest since a 12.4 percent rate reported for the fourth quarter of 2010, while growth for equipment investment was the highest since a 20.3 percent rate in the third quarter of 2011. Therefore some reversal should not have been much of a surprise.

There was also a reversal on inventories, which showed a slower rate of accumulation in the quarter. As a result, they subtracted 0.57 percentage points from growth in the quarter. They had added 1.87 percentage points to the strong 4.1 percent growth number reported for the third quarter of 2013. It is worth noting that inventories are still accumulating at a rapid $87.4 billion annual rate. As a result, slower accumulation may be a further drag in future quarters.

Consumption grew at a strong 3.0 percent annual rate. The big story here was 4.4 percent growth in service consumption, the highest since a 4.7 percent rate back in the second quarter of 2000. This was driven by a 9.9 percent growth in health care spending that added 1.1 percentage points to growth for the quarter. This is undoubtedly the effect of the Affordable Care Act. Presumably this indicates a one-time jump and not a higher rate of growth going forward.

Other components of consumption were weak, with durable goods consumption rising at a 0.8 percent annual rate and non-durable at just a 0.1 percent rate. Weather may have been somewhat of a factor in reducing purchases, but it is unlikely we will see big jumps in these categories in future reports. At 4.1 percent of disposable income, the saving rate is unusually low. It is not therefore reasonable to expect a big surge in consumption.

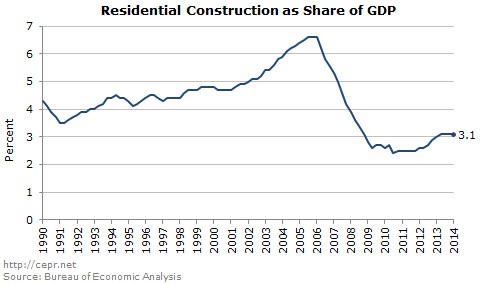

Residential construction fell at a 5.7 percent annual rate, subtracting 0.18 from growth in the quarter. Weather likely played a big role in this, as many starts were put off in the Midwest and Northeast. While construction will be contributing to growth in future quarters there will not be a big rebound. While it had averaged close to 4.5 percent of GDP in pre-bubble years (compared to around 3.0 percent now), its longer-term level is likely to be closer to 4.0 percent of GDP. This is partly due to demographics and partly due to growing cost of health care.

Health care takes up an additional 6-8 percentage points of GDP compared with the two decades before the bubble. If this growth comes at the expense of other household spending (roughly 70 percent of GDP), then we should expect residential construction to fall by around 0.4 percentage points as a share of GDP.

The plunge in exports reported for the quarter is almost certainly just a timing issue. These data are always erratic. Nonetheless, the deficit is back up to almost $500 billion in the quarter. This is demand that must be made up by the other components of GDP. This deficit is a major cause of “secular stagnation.”

The government sector was again a drag on growth as state and local spending shrank at a 1.3 percent rate, more than offsetting 0.7 growth rate at the federal level. In real terms state and local investment is down by more than 17.0 percent from its pre-recession level. Federal investment is down by roughly 5.0 percent, although this is all on the defense side. While the weakness in the first quarter number is clearly overstated by focusing on the 0.1 percent overall growth figure, this report suggests GDP growth for 2014 is likely to be closer to 2.5 percent than the 3.0 percent range used in many projections. Growth in most categories of spending will likely look like the average of the last three quarters, but that is just 2.3 percent.