Issue Brief

The Cost of Debt in a Time of Overlapping Crises

Issue Brief

The authors thank Jake Johnston, Rebecca Ray, David Rosnick and Mark Weisbrot for helpful contributions, suggestions and editorial work.

The global debt outlook for developing countries remains highly precarious after years of successive shocks to the world economy. The US-Israeli war on Iran has intensified pressures on global energy markets, pushing oil prices temporarily over $100 a barrel, increasing the cost of imports, and threatening food security and balance of payments stability for many countries.1 This comes on top of the lingering effects of the COVID-19 pandemic and the commodity and supply chain disruptions triggered by the war in Ukraine, rising trade fragmentation, and weak global growth.

These conditions are especially difficult for low- and middle-income countries (LMICs) that are more exposed to energy and food price shocks, more dependent on costly external financing, and less able to absorb renewed external shocks. In March 2025, the IMF spokesperson stated that, if energy prices rise by 10 percent and remain elevated for a year, global inflation could increase by about 40 basis points.2 For developing economies, the challenge is not only the immediate impact of higher energy and food prices but also the broader dynamics that can follow: inflation persists, interest rates rise, and external financing becomes more costly.

Since the Federal Reserve began raising interest rates in 2022, global financial conditions have remained tight, thereby increasing borrowing costs for developing economies. Capital has also shifted toward safer assets, and some countries are finding it harder to roll over maturing obligations or secure new financing on affordable terms.3 For those with large shares of foreign-currency debt, depreciation of domestic currency can further raise the domestic burden of repayment.

At the same time, growth remains too weak to offset these pressures. While advanced economies have largely recovered, the recovery in emerging market and developing economies remains incomplete, with more than one-quarter still below 2019 levels of per capita GDP, particularly in low-income countries and those affected by fragility and conflict. Across emerging market and developing economies, projected per capita income growth is about 3.1 percent in 2026–27, around 1 percentage point below the 2000–2019 average, a level insufficient to reverse pandemic income losses or significantly reduce poverty.4

The COVID-19 pandemic triggered a severe global shock, particularly for developing economies, but it was met with a meaningful international response. The 2021 allocation of special drawing rights (SDRs) provided rapid support, offering balance of payments support and expanding space for countercyclical policies. However, in today’s context of multiple, overlapping crises, no comparable response has been mobilized. The current debt burden of developing countries is unsustainable and requires a comprehensive policy response, including systemic reforms and debt cancellation as well as immediate relief measures.

Debt service is absorbing resources that could otherwise support health, education, infrastructure, and climate adaptation — perpetuating a vicious cycle. The implications go beyond short-term fiscal pressure, especially in the context of the climate crisis: They include delayed investment, weaker preparedness in the face of recurring climate catastrophe, and slower progress on growth and poverty reduction.

This brief quantifies the external public debt in LMICs and presents an overview of the interconnected debt and climate crises. Using data from the World Bank International Debt Statistics updated through 2024, this brief looks at the debt burdens of 118 LMICs for which figures are available. Finally, it highlights necessary, systemic changes to the international financial architecture and the growing movement advocating for those reforms.

The total external debt stock for LMICs has expanded significantly in the last 15 years, and just as importantly, the composition of that debt has also shifted, with countries increasingly reliant on more expensive private creditors.

In LMICs excluding China, external public debt reached over $3.3 trillion in 2024,5 equivalent to about 15.5 percent of GDP, up from 10 percent of GDP in 2010 — more than a 50 percent increase.6

Figure 1

Figure 1 shows the evolution and composition of debt stocks since 2010. Since 2010, private creditors have increased their share of external public debt in LMICs from about 42 percent to more than 50 percent, making private creditors the dominant creditor group. Bilateral lending has declined significantly, from around 22 percent of total debt in 2010 to about 14–15 percent in 2024 and to roughly 10 percent when excluding China, whose role has increased but remains relatively limited despite heightened public attention. Multilateral lending has also increased, particularly during the COVID-19 pandemic, and continues to be the main source of financing for the median LMIC.

The rise in private creditor shares is driven by the borrowing of middle-income countries, especially upper-middle-income economies, where private creditors account for about 66 percent of external public debt in 2024, as shown in Figure 2. Lower-income countries rely more on multilateral financing. Because private debt carries higher interest rates and shorter maturities, this leaves middle-income countries more exposed to rising debt service burdens.

Figure 2

For low-income and lower-middle-income countries, greater reliance on multilateral creditors increases access to concessional financing but does not necessarily expand fiscal space. Although multilateral loans tend to carry lower interest rates, they are often used to repay more expensive private debt rather than finance public priorities, effectively channeling development finance toward servicing existing obligations.7

Multilateral lending can also add to debt pressures through policy conditionality. The IMF’s Resilience and Sustainability Trust, for example, requires countries to already have a large upper-credit-tranche IMF loan, potentially increasing debt burdens and reinforcing pro-cyclical constraints in climate-vulnerable economies.8 In addition, IMF surcharges continue to raise borrowing costs for its most indebted members: Developing countries are expected to pay an estimated $5.2 billion in surcharges between 2025 and 2030, and despite the 2024 reform, the policy remains a significant obstacle to reducing IMF-related debt burdens.9

As of March 2026, 75 out of the 119 LMICs with available credit assessments from the IMF and rating agencies are in or at risk of debt distress — that is, they face significant difficulties in servicing their debt or have already defaulted, limiting their ability to finance essential spending and investment. This includes LMICs classified by the IMF as being in debt distress or at “moderate” or “high” risk of debt distress as well as countries with bond ratings indicating “substantial risk” of debt distress.10

Interest rates continue to burden LMICs, resulting in mounting payments that siphon scarce resources from government budgets. This is partially due to higher risk premia for LMICs; as debt distress risks have increased, borrowing rates may not decline at a commensurate pace to international interest rates.

In 2024, LMICs excluding China owed approximately $428 billion in external public debt service, with an average of 32 percent going to interest payments.11 As shown in Figure 3, low-income countries owed about $7 billion, with 28 percent going to interest. Lower-middle- and upper-middle-income countries owed approximately $158 and $263 billion in debt service, of which interest payments represent 30 and 33 percent, respectively.

Figure 3

In periods of economic stability, states typically make interest payments on external debt while rolling over principal amounts by taking on new loans. The US Federal Reserve’s rate hikes in 2022, followed by other major economies and LMICs, significantly increased the cost of debt service.12 At the same time, worsening credit ratings and the retreat of private bondholders have made access to new financing more difficult. Net transfers from these creditors have been negative for three consecutive years, from 2022 to 2024, meaning that countries have paid more in principal and interest than they received in new disbursements.13 As a result, many developing countries face tighter budgets and little access to credit markets and are therefore at risk of not being able to roll over principal payments on external debt.

This means that some countries will be forced to make not only expected interest payments but also principal payments that would previously have been rolled over — resulting in rapidly increasing debt service payments and a greater risk of default. The IMF estimates that principal payments will increase substantially in the coming years, making refinancing more challenging, especially for Sub-Saharan African countries.14

Figure 4

As shown in Figure 4 above, the median interest payments on external public debt across LMICs increased from about 1.4 percent of government revenue in 2010 to 3.5 percent in 2024 — higher than during the COVID-19 pandemic crisis.15

Figure 5

Debt servicing costs are also high relative to export revenue, as shown in Figure 5 above. Interest payments represent approximately 2 to 2.5 percent of export revenues for low-, lower-middle–, and upper-middle-income countries, respectively.

For low-income countries in particular, the median debt service, including principal owed, amounts to over 8 percent of export revenues. This is comparable to levels seen during the debt crisis of the 1990s that prompted the IMF and World Bank to launch the Heavily Indebted Poor Countries (HIPC) Initiative and issue debt cancellation to qualifying countries. According to the IMF, the median debt service for low-income countries equaled 10 percent of exports in 1994 — just about 1 percent higher than in 2024.16

The global context has also changed in important ways since the mid-1990s. Today, the debt burdens of developing countries are siphoning resources not only from necessary investments in health, education, and economic development but also from combating climate change, whose impacts disproportionately fall on lower-income countries.

When higher global interest rates and shrinking access to credit push up external debt servicing, governments are forced to sacrifice crucial climate and development efforts in favor of meeting debt obligations. This dynamic often triggers a negative feedback loop: Tight budgets curb revenue-raising potential, leading to further borrowing, deeper indebtedness, and insufficient climate preparedness.17

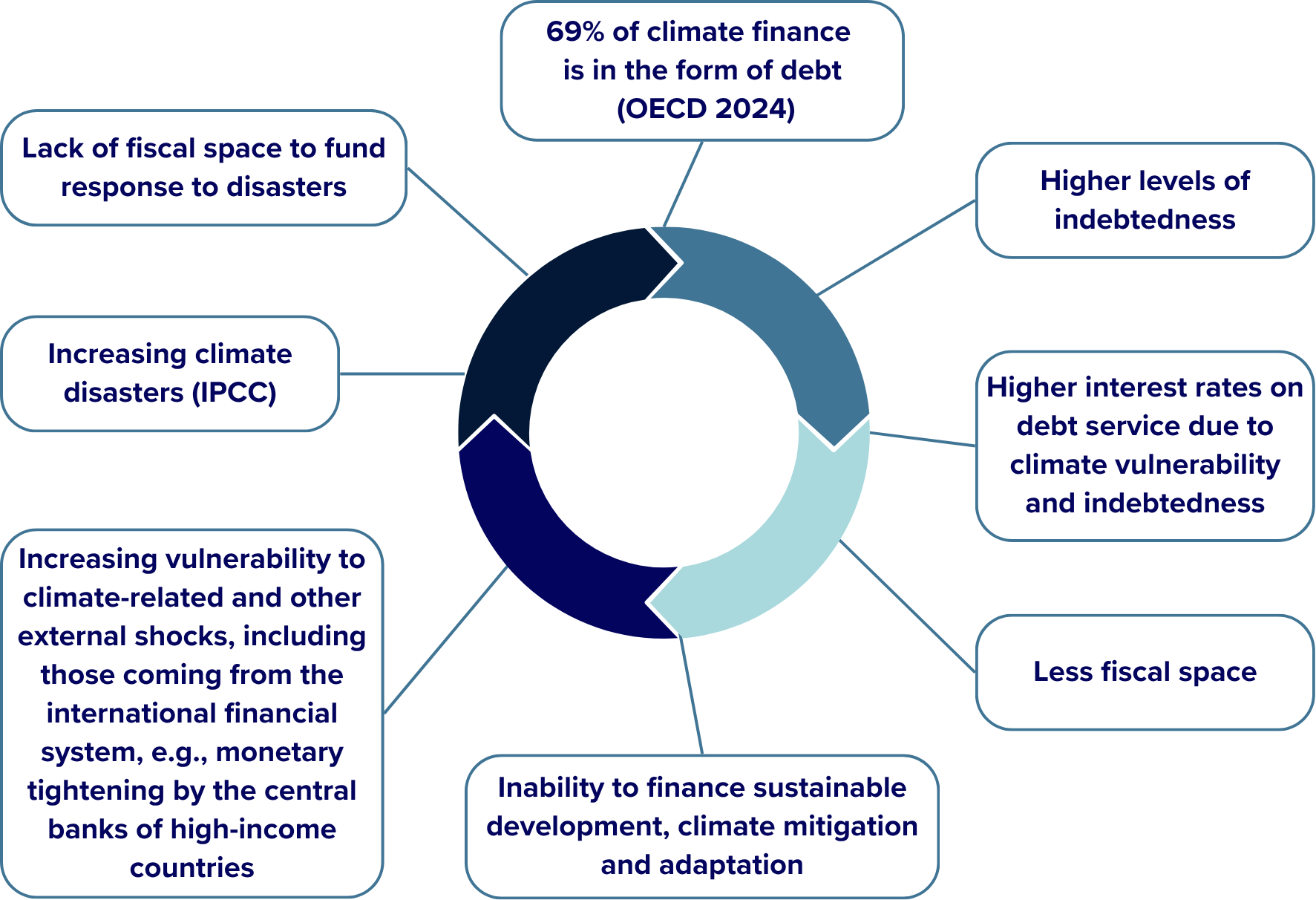

Increasingly frequent and severe climate disasters mean that LMICs have little choice but to take on more debt to finance a sufficient response.18 This heavy dependence on debt exacerbates financial strain, as a growing share of borrowing is used to repay existing loans rather than to fund new climate projects, further restricting fiscal space for much-needed adaptation and mitigation efforts.19 The lack of investment in climate preparation and public services in turn makes these countries more vulnerable to the immediate and long term effects of climate change, perpetuating a vicious cycle, as illustrated in Figure 6.

Figure 6

Although wealthy countries have largely caused the climate crisis, LMICs disproportionately face its greatest relative impacts.20 Developing countries have repeatedly called for stronger climate finance commitments, yet their demands remain unmet. The OECD estimates that in 2022, 69% of public climate finance provided to developing countries was in the form of debt, which exacerbates the intertwined crises.21

The lack of a comprehensive debt workout mechanism is a key obstacle for developing countries to access restructuring and sustainable recovery from debt distress. Typically, countries facing debt distress are forced to borrow from the IMF to prevent default and begin negotiating with other creditors in what can become a very long, costly process.22 In 2020, the G20 launched the Common Framework to coordinate restructurings, but it is only accessible to 73 lower-income countries and only coordinates restructuring for bilateral and multilateral debt, leaving private debt off the table.

Only four countries have pursued debt restructuring through the Common Framework thus far: Chad, Ethiopia, Ghana, and Zambia.23 Restructuring comes with significant risk, as it is considered to all effects a default. Ensuing credit-rating downgrades result in more expensive private debt and thus higher payments. For this reason, the Common Framework is only useful to countries that have predominantly bilateral debt; higher payments to private creditors, usually bondholders, can exceed the relief of a lower debt burden from bilateral creditors. This trade-off is not worth it to many qualifying countries.

The existing debt resolution system favors bondholders, who have delayed restructurings to achieve greater profits at the expense of other creditor groups and debt-distressed countries.24 Without ensuring equal treatment for different creditor groups, the process becomes prolonged and complex for debtor nations, ultimately providing insufficient debt relief.25

Middle-income countries, which do not qualify for restructuring under the Common Framework, are left to negotiate with different creditors individually. Absent a systemic debt resolution mechanism, restructurings can depend on political will. Ukraine, in the context of full-scale war and major economic instability, was able to negotiate a deal with bondholders within months in 2024 with the help of international pressure, while Suriname and Sri Lanka, for example, waited two to three years.26 Even after its restructuring, Sri Lanka was expected to remain one of the most indebted countries in the world.27

In most restructurings, debt-distressed countries are forced to make costly concessions against the public interest, such as deep cuts to social services and other austerity measures. Deals can also be contingent on debtor states raising revenue from extractive activities that add to the climate crisis.28 Developing countries are already forced to rely on extractive industries to service external debt, as these revenue streams are a key source of foreign currency. Restructurings can perpetuate this dynamic, and an independent, comprehensive debt resolution mechanism is necessary to break the cycle.

Developing countries continue to organize for the creation of mechanisms to battle the debt and climate crises and make progress toward the Sustainable Development Goals. The Fourth United Nations (UN) Conference on Financing for Development, which took place in 2025 in Seville, ultimately fell short of expectations — particularly by failing to establish a binding framework for debt resolution or advance a UN debt convention. Notable outcomes of the conference, however, included the creation of a UN-led working group that will set new standards and procedures to help avoid the onset and prolongation of debt crises as well as a platform for borrower countries to discuss and coordinate approaches to debt issues.29

Nevertheless, developing countries and civil society organizations continue to call for a framework convention at the UN, which would represent legally binding international guidelines and procedures to help avoid the onset and prolongation of debt crises. To break the vicious cycle, a framework convention on debt ought to include the creation of a multilateral sovereign debt resolution mechanism, an independent body through which all countries, regardless of income status, could restructure external debt owed to every creditor class in a rules-based process. To prevent “too little, too late” restructurings — insufficient debt relief after debt distress has already culminated into a crisis — the mechanism would ensure a speedy work-out process abiding by important principles, such as equal treatment for creditor classes. This would prevent private creditors from unnecessarily delaying restructurings and would bind them to the same rules followed by bilateral and multilateral creditors.

A summary of several reform opportunities to the international financial and debt architecture and additional civil-society-driven demands is provided in Table 1 below.

Table 1

While the debt crisis can only be resolved through systemic reforms, significant debt cancellation, and grant-based climate finance, developing countries can receive immediate fiscal support from a new $650 billion — or greater — allocation of SDRs.30

The profound shock of the COVID-19 pandemic led to the worst contraction in per capita GDP in 75 years in 2020, severely affecting economic activity across developing countries. The international response included an allocation of SDRs equivalent to $650 billion by the IMF in 2021, and about $209 billion went to emerging markets and developing economies, excluding China. This allocation provided liquidity without adding to debt burdens or imposing conditionality, supported recovery, and helped save hundreds of thousands of lives in developing countries, although its impact was more limited than it could have been, as the allocation was only approved in 2021 despite being proposed by the IMF in March 2020.31 In addition, unprecedented fiscal stimulus in the United States also had significant spillover effects on the global recovery.32

In an April 2026 statement, the heads of the IMF, the World Bank, and the International Energy Agency committed to assessing “potential financing needs and related provision of financial support (including through concessional financing), and use of risk mitigation tools as appropriate” in regard to the global energy shock caused by the US-Israeli war on Iran.33 A new issuance of SDRs would be the most appropriate and impactful response to address a crisis disproportionately impacting developing countries in the immediate term.

An SDR allocation would increase reserves, ease debt burdens and enable countries to access key imports in the face of rising prices. Unlike loans, SDR allocations do not require repayment, making them a unique, non-debt source of liquidity that also comes without policy conditionalities. Additionally, countries can exchange SDRs for freely usable currencies, such as US dollars or euros, ensuring immediate access to liquidity without new borrowing.34

SDRs can also be used to directly pay back IMF debt, which can be particularly onerous with regard to debt crises as the conditionalities attached to large loans can exacerbate future debt accumulation.35

The debt challenges facing LMICs are not the result of isolated shocks. They reflect deeper structural weaknesses — which amplifies volatility and raises financing costs precisely when countries are least able to absorb it — in the global financial system. After successive shocks, many LMICs now face rising debt service burdens, reduced access to external financing, and increasing difficulty in rolling over existing obligations.

The result is a self-reinforcing cycle. As financing conditions tighten, governments are diverting scarce resources toward external debt service and away from health, education, infrastructure, and climate resilience. At the same time, climate shocks and development needs are increasing financing requirements, deepening reliance on costly borrowing. For many LMICs, the problem is no longer simply one of temporary liquidity but of debt burdens that are increasingly difficult to sustain under current global conditions.

These pressures are compounded by an inadequate debt resolution system. The current architecture — fragmented and reliant on slow, case-by-case negotiations — has repeatedly delivered restructurings that come too late and provide too little relief. As creditor landscapes grow more complex and private creditors play a larger role, coordination problems are intensifying, leaving countries trapped between adjustment, arrears, and prolonged uncertainty.

Breaking this cycle requires more than incremental fixes. LMICs need faster and more effective debt restructuring, meaningful debt reduction where necessary, and a more coherent and rules-based system for sovereign debt resolution. Immediate support — including a new allocation of SDRs, expanded access to concessional and grant-based finance, and reforms to multilateral lending that reduce rather than reinforce procyclical pressures — is also essential.

The renewed momentum behind the Jubilee “Turn Debt into Hope” initiative reflects a growing recognition that the current approach is failing.36 Like earlier debt relief efforts, it points to the need for both urgent action and deeper reform — not only to address unsustainable debts but also to change the structures that continue to reproduce them. Without such action, debt will continue to constrain development and climate action across much of the developing world. With it, there is still an opportunity to build a more stable and equitable international financial system that allows countries to invest in their futures rather than sacrifice them to debt service.

Adrian, Tobias, Jihad Azour, Nigel Chalk et al. 2026. “How the War in the Middle East Is Affecting Energy, Trade, and Finance.” IMF Blog, March 30. https://www.imf.org/en/blogs/articles/2026/03/30/how-the-war-in-the-middle-east-is-affecting-energy-trade-and-finance

Cashman, Kevin, Andrés Arauz, and Lara Merling. 2022. “Special Drawing Rights: The Right Tool to Use to Respond to the Pandemic and Other Challenges.” Washington, DC: Center for Economic and Policy Research, April. https://cepr.net/publications/special-drawing-rights-the-right-tool-to-use/

Chuku, Chuku, Prateek Samal, Joyce Saito et al. 2023. Are We Heading for Another Debt Crisis in Low-Income Countries? Debt Vulnerabilities: Today vs the pre-HIPC Era. IMF Working Paper No. 2023/079, April 4. https://www.imf.org/en/publications/wp/issues/2023/04/04/are-we-heading-for-another-debt-crisis-in-low-income-countries-debt-vulnerabilities-today-531792

Debt Justice. 2024. “Sri Lanka’s bondholders to get repaid 20%-45% more than governments.” Debt Justice, July 26. https://debtjustice.org.uk/press-release/sri-lankas-bondholders-to-get-repaid-20-45-more-than-china

Diwan, Ishac, Brendan Harnoys-Vannier, and Martin Kessler. 2025. “The Pain of a High-Interest Rate Environment.” Financial Development Lab (FDL) Short notes. January. https://findevlab.org/wp-content/uploads/2024/12/FDL_Short-Note_The-pain-of-a-high-interest-rate-environment_7Jan25_FINAL.pdf

European Network on Debt and Development (Eurodad). 2024. “Financing Development? An Assessment of Domestic Resource Mobilisation, Illicit Financial Flows and Debt Management.” European Network on Debt and Development, May 23. https://www.eurodad.org/financing_development_an_assessment_of_domestic_resource_mobilisation_illicit_financial_flows_and_debt_management

Fill the Fund. 2025. “Developing Countries Decry ‘Problematic’ Loss and Damage Finance Gap as Global ‘Fill The Fund’ Campaign Launched to Demand Rich Nations #PayUp.” July 10. https://www.fillthefund.org/post/fill-the-fund-campaign-launched-to-demand-rich-nations-payup

Galant, Michael. 2025. “FfD4 at Sevilla Plants the Seeds of Debtor Unity.” Inter Press Service News Agency, July 4. https://cepr.net/publications/ffd4-at-sevilla-plants-the-seeds-of-debtor-unity/

Galant, Michael, and Ivana Vasic-Lalovic. 2025. “Tinkering with a Broken Policy: The IMF’s 2024 Surcharge Reform.” Washington, DC: Center for Economic and Policy Research, January. https://cepr.net/publications/tinkering-with-a-broken-policy-the-imfs-2024-surcharge-reform/

Gallagher, Kevin P, and Franco Maldonado Carlin. 2023. “Climate Vulnerability and Balance of Payments Problems in Developing Countries.” Working Paper. https://drive.google.com/file/d/15cYLzpsi1xEvcgnmZqd3Ey6Ukv_NxisV/view

Girshova, Polina, and Iolanda Fresnillo. 2024. “Why do we need a Framework Convention on Sovereign Debt?” European Network on Debt and Development, November. https://www.eurodad.org/un-debt-qa

Global Debt and Climate Working Group. 2024. Debt Demands & Debunking Distractions for Climate Action. June. https://www.eurodad.org/debt_demands_and_debunking_distractions_for_climate_action

Guzmán, Martín, and Joseph E. Stiglitz. 2025a. “How New York State Lawmakers Can Help Address Debt Crises in the Global South.” Initiative for Policy Dialogue (IPD) and Columbia SIPA Institute of Global Politics (IGP), January. https://ipdcolumbia.org/wp-content/uploads/2025/01/IPD_IGP_SovereignDebt_FINAL.pdf

———2025b. The Jubilee Report: A Blueprint for Tackling the Debt and Development Crises and Creating the Financial Foundations for a Sustainable People-Centered Global Economy. The Pontifical Academy of Social Sciences, June.

Initiative for Policy Dialogue (IPD). 2024. “Addressing the Debt and Development Crises in Countries from the South in the Year of the Jubilee.” Final statement, December. https://ipdcolumbia.org/wp-content/uploads/2024/12/FINAL-PASS-IPD-Statement-Dec-2024.pdf

International Monetary Fund (IMF). 2025a. “Debt Vulnerabilities and Financing Challenges in Emerging Markets and Developing Economies—An Overview of Key Data.” IMF Policy Paper No. 2025/002, February 20. https://doi.org/10.5089/9798229002264.007

———. 2025b. “List of LIC DSAs for PRGT-Eligible Countries.” September 31. https://www.imf.org/external/pubs/ft/dsa/dsalist.pdf.

International Monetary Fund (IMF), World Bank Group, and International Energy Agency (IEA). 2026. “Joint Statement by the Heads of the International Energy Agency, International Monetary Fund, and World Bank Group.” April 1. https://www.imf.org/en/news/articles/2026/04/01/pr-26100-joint-statement-by-the-heads-of-the-iea-imf-and-wb-group

Meattle, Chavi , Anna Balm, Jose E. Diaz et al.. 2024. Landscape of Climate Finance in Africa 2024. Climate Policy Initiative, October 22. https://www.climatepolicyinitiative.org/publication/landscape-of-climate-finance-in-africa-2024/

Merling, Lara. 2024. “‘Greenwashing’ Structural Adjustment.” Phenomenal World, October 22. https://www.phenomenalworld.org/analysis/greenwashing-structural-adjustment/

Merling, Lara, Ivana Vasic-Lalovic, Angelica Huerta Ojeda et al. 2024. “The Rising Cost of Debt: An Obstacle to Achieving Climate and Development Goals.” Center for Economic and Policy Research (CEPR), May. https://cepr.net/wp-content/uploads/2024/06/The-Rising-Cost-of-Debt-An-Obstacle-to-Achieving-Climate-and-Development-Goals-Merling_Vasic-Lalovic_Valle-Cuellar_Huerta-Ojeda-2024-1.pdf

Organisation for Economic Co-operation and Development (OECD). 2024. Climate Finance Provided and Mobilised by Developed Countries in 2013-2022. OECD Publishing. https://doi.org/10.1787/19150727-en.

Panizza, Ugo. 2024. “The Pitfalls of Value Recovery Instruments in Sovereign Debt Restructuring.” Finance for Development Lab (FDL) Policy Note 17. September. https://findevlab.org/wp-content/uploads/2024/09/FDL-Policy-Note-17_The-Pitfalls-of-Value-Recovery-Instruments-in-Sovereign-Debt-Restructuring-Sept24_Ugo-Panizza_Final.pdf

Pontifical Academy of Social Sciences (PASS) and Columbia University Initiative for Policy Dialogue (IPD). 2025. The Jubilee Report: A Blueprint for Tackling the Debt and Development Crises and Creating the Financial Foundations for a Sustainable People-Centered Global Economy. June. https://ipdcolumbia.org/wp-content/uploads/2025/06/Jubilee-Report-7.17.pdf

Shalal, Andrea, and Rodrigo Campos. 2026. “IMF says prolonged increase in energy prices could boost inflation, lower growth.” Reuters, March 19. https://www.reuters.com/world/imf-says-prolonged-increase-energy-prices-could-boost-inflation-lower-growth-2026-03-19/

Strohecker, Karin, and Libby George. 2024. “Ukraine reaches preliminary deal with bondholder group on $20-billion debt restructure.” Reuters, July 22. https://www.reuters.com/markets/rates-bonds/ukraine-reaches-preliminary-deal-with-bondholder-group-20-bln-debt-restructure-2024-07-22/

Táíwò, Olúfẹ́mi O., and Patrick Bigger. 2022. Debt Justice for Climate Reparations. Climate and Community Project, April. https://climateandcommunity.org/research/debt-justice-for-climate-reparations/

Trading Economics. 2026. “Country Credit Ratings.” https://tradingeconomics.com/country-list/rating

United Nations. 2025. “Sevilla Commitment.” Fourth International Conference on Financing for Development, Seville, Spain, UN Doc. A/CONF.227/2025/L.1, June 18. https://docs.un.org/en/A/CONF.227/2025/L.1

United Nations Economic Commission for Africa (ECA) and Economic Commission for Latin America and the Caribbean (ECLAC). 2022. Special Drawing Rights (SDRs) and the COVID-19 Crisis. COVID-19 Report, April. https://repositorio.cepal.org/server/api/core/bitstreams/a4d76467-4802-421e-bb51-207cdb91bccf/content

United Nations Trade & Development (UNCTAD). 2025. A World of Debt 2025. United Nations. https://unctad.org/publication/world-of-debt

Vasic-Lalovic, Ivana. 2022. “The Case for More Special Drawing Rights: Rechanneling Is No Substitution for a New Allocation” Washington, DC: Center for Economic and Policy Research, October 13. https://cepr.net/publications/the-case-for-more-special-drawing-rights/.

———. 2025. “Debt and Climate Dashboard.” Center for Economic and Policy Research,. July 29. https://cepr.net/publications/debt-and-climate-dashboard/

Weisbrot, Mark. 2023. “Immediate Help for Developing Countries Is Available, But the US Treasury Department Is Blocking It.” The Nation, July 12. https://cepr.net/publications/immediate-help-for-developing-countries-is-available-but-the-us-treasury-department-is-blocking-it/.

Weisbrot, Mark, Joe Sammut, John Schmitt et al. 2025. “The United States, the IMF, and Special Drawing Rights.” Washington, DC: Center for Economic and Policy Research. October 14. https://cepr.net/publications/the-united-states-the-imf-and-special-drawing-rights-2/

World Bank. 2025a. International Debt Report 2025. World Bank Group. https://doi.org/10.1596/978-1-4648-2262-9

———. 2025b. International Debt Statistics (IDS). World Bank DataBank. https://databank.worldbank.org/source/international-debt-statistics

———. 2026. Global Economic Prospects. World Bank Group, January. https://openknowledge.worldbank.org/server/api/core/bitstreams/a9e24256-baf8-45bb-9075-75e437e1d6f7/content

Zucker-Marques, Marina. 2023. “Winner Takes All — Twice: How Bondholders Triumph, Before and After Debt Restructuring.” Debt Relief for Green and Inclusive Recovery, November 16. https://drgr.org/news/winner-takes-all-twice-how-bondholders-triumph-before-and-after-debt-restructuring/

Event Recap

Article

Article

Report