September 22, 2014

Influencing the Debate from Outside the Mainstream: Keep it Simple

September 13, 2014, Dean Baker’s comments at the 2014 Rethinking Economics NYC Forum

Forum titled “The Role of Economic Models in Public Policymaking”

If people working outside of the mainstream of the profession are going to have any impact on economic policy debates in the United States it is essential that they understand the forum in which the debate is taking place. This is not a contest of ideas where the best arguments and evidence win out. If we are talking about a debate within the economics profession, think of debating the morality of abortion with the pope in front of the College of Cardinals. That is pretty much what it is like to try to challenge any of the main precepts of economics within the economics profession.

The route for making progress is to get outside of the profession. For this it is necessary to appeal to people in policy positions, to reporters, to the general public: people who might follow economic debates, but don’t have extensive backgrounds in economics. And it is important to recognize what you are asking these people to do. You are asking these people to accept your claims over the claims of the most prominent economists in the profession.

This means that you better keep what you have to say simple. It is unlikely that many people are going to take the time to consider a complex argument even if it doesn’t require a PhD in economics to understand. To my mind the gold standard is a chart with two bars, where bar A is bigger than bar B. To make this point, I will briefly recount some of the economic debates in which I have been involved where the truth, justice, and non-mainstream economists won out over the forces of accepted wisdom coming from the elites of the profession.

The first, and perhaps best, example is the debate over the famous Reinhart-Rogoff 90 percent debt cliff that was kicked off by a paper by Thomas Herndon, Michael Ash, and Robert Pollin (HAP) which showed that cliff story depended on an Excel spreadsheet error.[1] When the error was corrected the sharp falloff in growth that Reinhart and Rogoff had found at debt-to-GDP ratios above 90 percent disappeared. Instead they found a negative relationship between debt-to-GDP ratios and growth at all levels, with the sharpest trade-off actually occurring at debt-to-GDP ratios around 25 percent.[2]

These revised results were radically at odds with the conclusions from the uncorrected paper which had been widely cited in policy debates in the United States and elsewhere. The fact that an Excel spreadsheet error was something that could be widely understood allowed for the media and the general public to appreciate the nature of the debate. Even Stephen Colbert got into the act, devoting a segment of his show to ridiculing Reinhart and Rogoff.

While correcting this error did not turn around the austerity debate, it certainly did open up space. The claim that there was some immediate need for sharp cuts in public debt in order to avert the cliff disappeared from the radar screen. We went back to the more traditional arguments about the virtues of balanced budgets.

The response of the economics profession to this error and its exposure was instructive. To a large extent there was a rallying around Reinhart and Rogoff, two prominent Harvard economists who established their reputations with a long track record of publications in top journals. It was as though HAP had been wrong to drag down the names of such well-regarded economists over a simple spreadsheet error.

Betsey Stevenson and Justin Wolfers gave us an example of this attitude in a piece in which they “refereed” the debate. They told readers:

“It has been disappointing to watch those on the left seize on the embarrassing Excel errors but ignore this bigger picture.”[3]

Of course we all make mistakes and no one would like to be publicly embarrassed over having once inaccurately copied numbers in an Excel spreadsheet. But perspective is desperately needed here. The Excel spreadsheet error was the reason the debate was taking place. Reinhart and Rogoff would not ordinarily be responding to criticisms from two University of Massachusetts professors and their grad student. If this had been a debate just over the correct aggregation method or econometric techniques, it would never have gotten far beyond the PERI website. Few people without advanced training in economics would follow that debate, but everyone can understand an Excel spreadsheet error.

The other point worth noting is that even if we take the most generous possible interpretation of Reinhart-Rogoff’s behavior in this matter, it is hard to see it in a positive light. They have said that the error resulted from the fact they were rushing to finish a draft for presentation. In a later version of the paper the erroneous calculation does not appear. But this later version does not have the 90 percent cliff.

Reinhart and Rogoff are both very intelligent people who surely knew how their work was being used in public debates. They had discussed their work with members of Congress, central bankers, and finance ministers. They knew that it was the 90 percent cliff threshold that was being held up in policy debates, not the finding of a general negative relationship between debt-to-GDP ratios and growth rates. Even if they had been rushed to finish the initial draft, it is difficult to believe that they could not have found the time to check their calculations or ask a graduate assistant to do so in the nearly three and half years between when the working paper was issued and when HAP was written.

Instead of being disappointed by the conduct of Reinhart and Rogoff, Stevenson and Wolfers are disappointed by the people on the left who were highlighting the error. I don’t mean to impugn Stevenson and Wolfers, both of whom are very good center-left economists. However, their attitude in this case shows the tribalism of the profession. If there is a question of seeking out the truth versus protecting leading lights in the profession, the bulk of the profession will opt for the latter. This is the reality that those outside the mainstream must recognize and overcome.

Fortunately the Reinhart-Rogoff spreadsheet error-type situations are not all that rare in economics. I will briefly go through a few with which I have some familiarity.

The Boskin Commission Tackles Social Security

Back in the mid-1990s we also had a serious bout of deficit hysteria comparable to the one we’re seeing today. The Very Serious People of that day (some of whom are still Very Serious People) all agreed that we had to move to balance the budget. Then as now, Social Security was one of the prime targets. Then Federal Reserve Board Chair Alan Greenspan came up with the innovative approach of reducing benefits by cutting the annual cost-of-living adjustment payment. His argument was that the consumer price index substantially overstated the true rate of inflation. He argued that the government could save a vast amount of money over the next decade by reducing the annual cost-of-living adjustment to something like one percentage point less than the rate of inflation shown by the CPI. There would also be large increases in revenues since the tax brackets are indexed to inflation also, as are a number of other government benefits.

Senator Daniel Patrick Moynihan, who was then head of the Senate Finance Committee, eagerly embraced this plan. He got the committee to appoint a commission of prominent economists, headed by Michael Boskin, the chief economist in President George H.W. Bush’s administration, to review the evidence and make recommendations to the committee.[4]

The Boskin commission issued its report in late 1996 just after President Clinton and the Republican Congress had both been re-elected. (The scene was more than a little comical, with technical discussions of items like hedonic price adjustments and geometric means versus arithmetic means drawing packed crowds of reporters, many of whom probably had not heard of the CPI six months earlier.) The commission’s assessment was that the CPI overstated the true increase in the cost of living by roughly 1.1 percentage point annually. They suggested that Congress appoint a group of experts to report the “true” rate of inflation each year, which would then be the basis for the indexation of benefits and taxes rather than the CPI calculated by the Bureau of Labor Statistics.

This general plan had a great deal of support in both parties in Washington, with the Very Serious People leading the charge. It also had substantial support in the economics profession. At the 1997 AEA convention Martin Feldstein moderated a panel on the report, which in addition to the commission members also included Yale University Professor William Nordhaus and M.I.T. Professor Jerry Hausman. The only person not pushing the commission report was Katherine Abraham, who was then Commissioner of the Bureau of Labor Statistics. In this capacity she could raise some questions about the specifics of the Boskin Commission report, but she could not be an open opponent of the commission’s plan.

While the evidence for the commission’s claim was weak (many of its claims of inadequate quality adjustments were based on introspection with much of the actual research being close to three decades old), it was difficult to challenge the assessment of many of the most prominent economists in the country. However, there was a very simple logical implication of the report that was hard for many people to accept. If inflation was in fact overstated by 1.1 percentage points annually, then it meant that real wages and real income had been rising by 1.1 percentage points more rapidly than the official data indicated.

This is just definitional. If nominal wages had risen 4.0 percent and the CPI showed a 3.0 percent inflation rate, then real wages would be reported as having increased by 1.0 percent. However, if the true rate of inflation was just 1.9 percent (1.1 percentage point less than the measure shown by the CPI), then real wages actually increased by 2.1 percent. When this difference in wage and income growth is carried back thirty or forty years it implies that people in the fifties and sixties were much poorer than the data indicate. In fact, it meant that most people who grew up in middle income families in the 1950s would have had a standard of living that was roughly at the poverty level in the mid-1990s. This didn’t strike many people as being right.[5]

Ultimately what killed the Boskin Commission report was the refusal of Richard Gephardt, the leader of the Democrats in the House to go along with the plan.[6] His opposition was key, because Gephardt was the most credible challenger at the time to then Vice-President Al Gore for the Democratic Presidential nomination in 2000. There was no better issue that Gephardt could have been given in the Democratic primaries than a cut in Social Security benefits. Gephardt could point to Gore as the person who cut your Social Security benefits, while he was the guy who tried to stop him.

Without Gephardt’s buy in, Clinton was not about to go forward. It also helped that the stock bubble and faster than projected growth led the deficit to fall much more than had been projected. It is worth noting that in spite of the near unanimity of the leading lights in the economics profession on the existence of a large bias in the CPI, the Bureau of Labor Statistics did not take steps to correct most of the bias identified by the Boskin Commission. The Government Accountability Office surveyed the four surviving members of the Boskin Commission in 2000. (Zvi Grilliches had died the prior year.) In their assessment, more than 0.8 percentage points of the bias they identified in the CPI remained even after BLS had made a series of changes in the index.[7] Yet few economists take account of this bias in their work or in discussions of economics policy.[8]

Stock Returns and Social Security: No Economist Left Behind

Shortly after he won the 2004 election, President Bush said that he had just gained some political capital and that he intended to now use it. The task at hand was privatizing Social Security. Bush’s team claimed that he could give workers a much better deal if they just put their money in private accounts rather than using Social Security’s old-fashioned one-size-fits-all model.

There were many good reasons to oppose going this route. The individual accounts would add a large element of risk in what is supposed to be workers’ core retirement income. They would also increase the administrative costs of the system by an order of magnitude. But the big potential attraction to many people who were not especially political was the promise of getting a much higher benefit on average from investing their money in the stock market. This promise of a higher return in the stock market in turn rested on the assumption that stocks would provide a 7.0 percent real return, their historic average.[9]

The problem with this assumption is the price to earnings ratios in the stock market were far above their historic average. This meant that, given the profit growth assumptions that are implicit in the Social Security trustees GDP and wage growth assumptions, it would be impossible for stocks to provide their historic rate of return going forward.

Arguing this point directly on its merits required more attention from reporters and people in policy positions than they were prepared to sacrifice; so we came up with a better way to make the point. We developed the “no economist left behind test.”[10] The test is very simple. Stock returns are the sum of capital gains and dividend payouts. That’s it; there is nothing else to enter into the mix. Based on this fact, the test asked economists to write down decade by decade averages for dividend yields and capital gains that would add up to give their 7.0 percent real return over Social Security’s 75-year forecasting horizon.

This was a simple way to show the 7.0 percent assumption was nonsense. Either price to earnings ratios would have to rise into the hundreds or it would be necessary to have stories of the whole corporate sector paying out more than their 100 percent of their after-tax profits in dividends. No self-respecting economist wanted to be associated with either of these positions.

We first posted this challenge on our website, however we were already in the early days of the blogosphere. Many progressive econ bloggers soon picked it up. This led to howls of anguish and outrage by conservatives. Some threw in the towel and acknowledged that it could not be done. Others wanted to change the assumptions so that we had more rapid GDP growth or a shift in income from wages to profits.

Finally Paul Krugman blasted the test into the national debate with a column in early February.[11] This exposed the fact that the privatizers were essentially just making up numbers. By showing there was no pot of gold in the private accounts, we were able to take the money out of it for typical workers. This drove home the point that there was no real potential for gain with privatization along the lines being proposed, just additional risk. This helped prevent the privatization plan from gaining any momentum. By the spring, most Republican members of Congress were running away from privatization as fast as they could.

Exploding Deficits and Health Care Costs

The deficit hysteria business is a major growth industry in Washington. Politicians have always been anxious to exploit public fears over borrowing; but the burgeoning industry of groups dedicated to highlighting the threat posed by deficits and debt largely owes its existence to Peter Peterson. Peterson made his fortune as the founder of the Blackstone, one of the country’s largest private equity companies. Over the last quarter century Peterson has started and/or funded a large set of organizations that focused on promoting concerns over deficits, including the Concord Coalition, the Committee for a Responsible Federal Budget, and Fix the Debt.

The basis for the hysteria stems largely from projections that show rapidly rising health care costs increasing government spending though programs like Medicare and Medicaid. The impact is hugely magnified with the assumption that revenues are never increased so that we get an exploding cycle of debt and deficits. To heighten anxieties these shortfalls are always expressed in the trillions of dollars rather than as a share of GDP. This only makes sense as a strategy to promote fear since virtually no one can make any sense of a deficit of $200 trillion over the infinite horizon. The deficit hawks also like to lump in Social Security with the health care programs to imply that the issue is one of an aging population rather than a broken health care system.

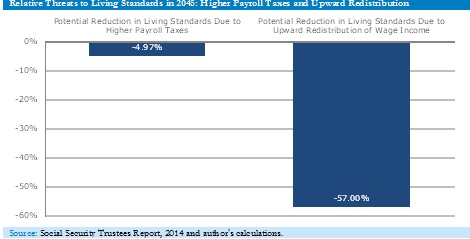

This is one of those great cases where a simple bar chart goes very far towards telling the basic story of why their deficit concerns should not be taken seriously. The projections from the Social Security and Medicare trustees give us an exact amount that we would have to raise taxes in order to keep both programs fully funded. Going three decades out to 2045 the projections show that we would have to raise the payroll tax by a total of 4.97 percentage points to keep both programs fully funded.[12] By comparison the Social Security trustees project that the average real wage will be more than 57 percent higher in 2045.[13] However, if we continue to see the same pattern of upward redistribution as we have seen in the years since 1980, then most workers will see little or none of the gains from this wage growth. All the benefits from growth will go to those in the top half of the wage distribution; with those at very top getting a grossly disproportionate share of the gains.

The point is that for most workers their prospective living standards are far more threatened by a continuing upward redistribution of income than by any plausible tax increases associated with the projected increase in the cost of Social Security and Medicare.

And of course the preferred policy in elite circles for preventing tax increases is cuts in benefits, which will leave these workers with lower living standards in their retirement years.[14] It would be difficult for anyone looking at this bar graph to explain why the prospect of an increase in payroll taxes of less than 5 percentage points over the next three decades should be of so much greater concern than an upward redistribution that costs workers an amount that exceeds 55 percent of their current wage.

There may not always be a simple story to describe every economic situation, but on many key issues the simple explanation does just fine. (We still need the simple story to explain why government debt is not a burden on our kids. The person who develops this story should get the people’s Nobel in economics.) Given that the only route for progress on economic policy issues depends on going outside the profession we have no choice but to find the simple explanation.

Economics may be too simple for economists to understand, but thankfully most of the rest of the world can pick it up with the right story. The job of non-mainstream economists is to tell that story.

[1] Herndon, Ash, and Pollin, 2013, “Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff, available at http://www.peri.umass.edu/fileadmin/pdf/working_papers/working_papers_301-350/WP322.pdf

[2] Remarkably, Reinhardt and Rogoff had not tested for causality. When subsequent work did test for causality it found the direction of causation was overwhelmingly from slower growth to higher debt (e.g. Arin Dube 2013, “Reinhart/Rogoff and Growth in a Time Before Debt,” http://www.nextnewdeal.net/rortybomb/guest-post-reinhartrogoff-and-growth-time-debt

[3] “Refereeing the Reinhart-Rogoff Debate” http://www.bloombergview.com/articles/2013-04-28/refereeing-the-reinhart-rogoff-debate

[4] In the initial set of hearings held by the finance committee, Dale Jorgenson, who was then head of Harvard’s economics department, had the equivalent of an Excel spreadsheet error. He testified that due to a mistake in the construction of CPI in the 1970s, Social Security benefits were about 10 percent higher than had been intended by Congress. He suggested that the committee design legislation to phase down the level of benefits to the level that would be in effect had there not been this mistake in the CPI in the 1970s. Senator Moynihan and others on the committee were prepared to act on this suggestion.

In reality there was much less money to be gained by correcting this CPI error than Jorgenson claimed. Social Security benefits are only indexed to the CPI after people retire. This meant that the people who had gotten excessive benefits because of the mistake in the CPI in the 1970s were in their 80s and 90s by the middle of the 1990s.

While several people (including me) tried to point this out to Professor Jorgenson and the committee, it took a study by the Treasury Department to convince Moynihan that there was little to be gained by going this route. After the Treasury issued its study Jorgenson finally corrected his testimony to the committee.

[5]The flip side of wage growth being far more rapid than the official data show is that people in the future will be far wealthier than standard projections indicate. I was once on a radio show with then Senator Alan Simpson, who was a big proponent of the Boskin Commission report. He managed to get the story exactly backwards, ranting that the 1.1 percent estimate was on the low side and saying that he has economists who tell him the overstatement might be 1.5 percent or even 2.0 percent. He then concluded that our children our going to be living in chicken coops. Of course the implication his claim was that they would be living in penthouses, enjoying living standards that are vastly higher than those of their parents and grandparents.

[6] I knew Gephardt’s former chief of staff and was able to pass along my work on the issue. He may have never looked at it, but it gave him something to hold up when he talked about the issue.

[7] Government Accountability Office, 2000. “Update of the Boskin Commission’s Estimate of Bias in the Consumer Price index,” GGD-00-50 [http://www.gao.gov/products/GGD-00-50]

[8] Many economists do argue for using the personal consumption deflator rather than the CPI since it uses chain weighting rather than a fixed weight index. This would eliminate 0.25-0.3 percentage points of the bias identified by the Boskin Commision, still leaving the bulk of their 0.8 percentage points (0.5 to 0.55 percentage points) to bias our understanding of the economy.

[9] President Clinton had made the same assumption in his proposal to invest much of the trust fund in the stock market near the peak of the 1990s bubble. I first wrote about this issue in reference to the Clinton administration’s proposal, “Saving Social Security With Stock: The Promises Don’t Add Up.” Century Foundation, 1997 [http://www.tcf.org/assets/downloads/tcf-savingSS97.pdf].

[10] This is available on the Center for Economic and Policy Research’s website at /documents/publications/noeconleftbehind_2004_11.pdf

[11] “Many Unhappy Returns,” February 1, 2005 [http://www.nytimes.com/2005/02/01/opinion/01krugman.html]

[12] This is found in Table V1.G2 of the 2014 Social Security Trustees Report [http://www.ssa.gov/OACT/tr/2014/VI_G1_OASDHI_payroll.html#170627]. In fairness, this figure does not include tax increases that might be necessary to sustain Parts B and D of the Medicare program, which are financed largely from general revenue. It also doesn’t take account of any feedback effect whereby a higher tax rate may be associated with less income.

[13] This is calculated from the projected real wage differentials shown in Table V.BI [http://www.ssa.gov/OACT/tr/2014/V_B_econ.html#292722]

[14]An alternative route for saving on Medicare would be to bring health care costs in the United States in line with costs in other wealthy countries. This would primarily mean cutting payments to doctors, hospitals, and other providers.