A New York Times article on the newest growth forecasts from the International Monetary Fund (I.M.F.) described the I.M.F. as “the most ardent defender of traditional free-trade policies.” This is not accurate.

The I.M.F. has been fine with ever stronger and longer patent and copyright protections. These government imposed monopolies raise the price of protected items by factors or ten or even a hundred above the free market price, making them equivalent to tariffs of hundreds or thousands of percent. These protections both have negative economic impacts, as would be predicted from any tariff of this size, and also are major factors in the upward redistribution of income that we have seen in most countries in recent decades.

The impact of these monopolies is most dramatic in prescription drugs. In the United States, we will spend more than $440 billion this year on drugs that would likely cost less than $80 billion in a free market. This gap of $360 billion is almost 2.0 percent of GDP. It is roughly five times what we spend on food stamps each year. It is more than 20 percent of the wage income of the bottom half of the workforce.

In addition, the huge gap between the protected price and the free market price leads to the sort of corruption that economists predict from tariff protection. It is standard practice for drug companies to promote their drugs for uses where they may not be appropriate. They also often conceal evidence that their drugs are not as safe or effective as claimed.

The cumulative cost of these protections in other areas is likely comparable. Anyone who supports these government granted monopolies cannot accurately be described as a proponent of free trade.

A New York Times article on the newest growth forecasts from the International Monetary Fund (I.M.F.) described the I.M.F. as “the most ardent defender of traditional free-trade policies.” This is not accurate.

The I.M.F. has been fine with ever stronger and longer patent and copyright protections. These government imposed monopolies raise the price of protected items by factors or ten or even a hundred above the free market price, making them equivalent to tariffs of hundreds or thousands of percent. These protections both have negative economic impacts, as would be predicted from any tariff of this size, and also are major factors in the upward redistribution of income that we have seen in most countries in recent decades.

The impact of these monopolies is most dramatic in prescription drugs. In the United States, we will spend more than $440 billion this year on drugs that would likely cost less than $80 billion in a free market. This gap of $360 billion is almost 2.0 percent of GDP. It is roughly five times what we spend on food stamps each year. It is more than 20 percent of the wage income of the bottom half of the workforce.

In addition, the huge gap between the protected price and the free market price leads to the sort of corruption that economists predict from tariff protection. It is standard practice for drug companies to promote their drugs for uses where they may not be appropriate. They also often conceal evidence that their drugs are not as safe or effective as claimed.

The cumulative cost of these protections in other areas is likely comparable. Anyone who supports these government granted monopolies cannot accurately be described as a proponent of free trade.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

In fact, it wasn’t even $800 billion, but the Washington Post has never been very good with numbers. The issue came up in a column by Paul Kane telling Republicans that they don’t have to just focus on really big items. The second paragraph refers to the Democrat’s big agenda after President Obama took office:

“Everyone knows the big agenda they pursued — an $800 billion economic stimulus, a sweeping health-care law and an overhaul of Wall Street regulations.”

The stimulus was actually closer to $700 billion since around $70 billion of the “stimulus” involved extensions of tax breaks that would have been extended in almost any circumstances. This was actually a very small response to the collapse of a housing bubble that cost the economy close to $1,200 billion dollars in annual demand (6–7 percent of GDP).

The Obama administration tried to counteract this huge loss of demand with a stimulus that was roughly 2 percent of GDP for two years and then trailed off to almost nothing. This was way too small, as some of us argued at the time.

The country has paid an enormous price for this inadequate stimulus with the economy now more than 10 percent below the level that had been projected by the Congressional Budget Office for 2017 before the crash. This gap is close to $2 trillion a year or $6,000 for every person in the country. This is known as the “austerity tax,” the cost the country pays because folks like Peter Peterson and the Washington Post (in both the opinion and news sections) endlessly yelled about debt and deficits at a time when they clearly were not a problem.

It is also worth noting that the overhaul of Wall Street was not especially ambitious. It left the big banks largely intact and did not involve prosecuting any Wall Street executives for crimes they may have committed during the bubble years, such as knowingly passing on fraudulent mortgages in mortgage backed securities.

Note:

Typos corrected, thanks for Robert Salzberg and Boris Soroker.

In fact, it wasn’t even $800 billion, but the Washington Post has never been very good with numbers. The issue came up in a column by Paul Kane telling Republicans that they don’t have to just focus on really big items. The second paragraph refers to the Democrat’s big agenda after President Obama took office:

“Everyone knows the big agenda they pursued — an $800 billion economic stimulus, a sweeping health-care law and an overhaul of Wall Street regulations.”

The stimulus was actually closer to $700 billion since around $70 billion of the “stimulus” involved extensions of tax breaks that would have been extended in almost any circumstances. This was actually a very small response to the collapse of a housing bubble that cost the economy close to $1,200 billion dollars in annual demand (6–7 percent of GDP).

The Obama administration tried to counteract this huge loss of demand with a stimulus that was roughly 2 percent of GDP for two years and then trailed off to almost nothing. This was way too small, as some of us argued at the time.

The country has paid an enormous price for this inadequate stimulus with the economy now more than 10 percent below the level that had been projected by the Congressional Budget Office for 2017 before the crash. This gap is close to $2 trillion a year or $6,000 for every person in the country. This is known as the “austerity tax,” the cost the country pays because folks like Peter Peterson and the Washington Post (in both the opinion and news sections) endlessly yelled about debt and deficits at a time when they clearly were not a problem.

It is also worth noting that the overhaul of Wall Street was not especially ambitious. It left the big banks largely intact and did not involve prosecuting any Wall Street executives for crimes they may have committed during the bubble years, such as knowingly passing on fraudulent mortgages in mortgage backed securities.

Note:

Typos corrected, thanks for Robert Salzberg and Boris Soroker.

Read More Leer más Join the discussion Participa en la discusión

Washington Post economics reporter Max Ehrenfreund featured a piece highlighting former Donald Trump adviser Steven Moore’s views of Trump’s recent shifts on economic policy. In particular, Moore took issue with Trump’s desire to see the value of the dollar fall. He argued that the dollar rose with strong economies under President Reagan and Clinton, while it was weak under Nixon, Ford, and Carter.

Actually, it is not especially accurate to claim the dollar rose under President Reagan. Using the Federal Reserve Board’s broad real index, it was trivially higher in January of 1989 than it was when Reagan took office in January of 1981 (91.3 in 1989 compared to 89.7 in 1981). The comparison goes the other way if we use December of 1988 (89.8) and December of 1989 (90.6), the last full month of Carter and Reagan’s terms.

As a practical matter, the run-up in the dollar in the first part of the Reagan administration led to a large trade deficit, causing serious hardship in manufacturing sectors. In response, Reagan’s Treasury secretary negotiated an orderly decline in the value of the dollar to bring down the deficit, which it did.

Also, if we are using the value of the dollar as a measure of the strength of the economy under different presidents, we find that it was virtually unchanged through President George H.W. Bush’s presidency and Clinton’s first term. The former was a period of weak growth, while the latter was a period of strong growth.

Washington Post economics reporter Max Ehrenfreund featured a piece highlighting former Donald Trump adviser Steven Moore’s views of Trump’s recent shifts on economic policy. In particular, Moore took issue with Trump’s desire to see the value of the dollar fall. He argued that the dollar rose with strong economies under President Reagan and Clinton, while it was weak under Nixon, Ford, and Carter.

Actually, it is not especially accurate to claim the dollar rose under President Reagan. Using the Federal Reserve Board’s broad real index, it was trivially higher in January of 1989 than it was when Reagan took office in January of 1981 (91.3 in 1989 compared to 89.7 in 1981). The comparison goes the other way if we use December of 1988 (89.8) and December of 1989 (90.6), the last full month of Carter and Reagan’s terms.

As a practical matter, the run-up in the dollar in the first part of the Reagan administration led to a large trade deficit, causing serious hardship in manufacturing sectors. In response, Reagan’s Treasury secretary negotiated an orderly decline in the value of the dollar to bring down the deficit, which it did.

Also, if we are using the value of the dollar as a measure of the strength of the economy under different presidents, we find that it was virtually unchanged through President George H.W. Bush’s presidency and Clinton’s first term. The former was a period of weak growth, while the latter was a period of strong growth.

Read More Leer más Join the discussion Participa en la discusión

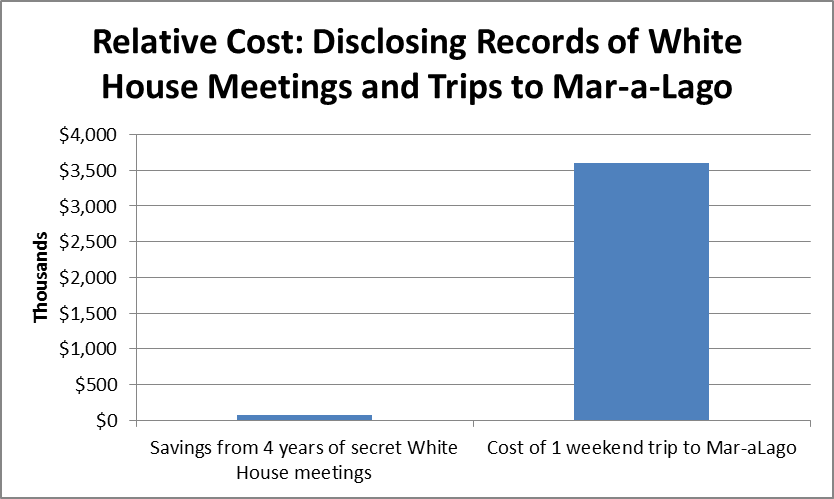

The Trump administration announced that would end the Obama administration’s practice of revealing the list of people who visit the White House. This list was useful in letting the public know who President Trump was making deals with.

The administration claimed this move was taken as a security measure and also to save the country $70,000 over the next four years. Since the government is projected to spend roughly $16 trillion over the next four years, the savings will be equal to 0.00000004 percent of projected spending. Alternatively, it will save each person in the country 0.007 cents annually over the next four years.

Another comparison that might be useful is that it costs taxpayers more than $3 million in additional security costs every time that President Trump goes to Mar-a-Lago for the weekend. This means that Trump is saving us an amount equal to 2 percent of the cost of one of his weekend trips by keeping the records of his meetings secret.

Source: See text.

The Trump administration announced that would end the Obama administration’s practice of revealing the list of people who visit the White House. This list was useful in letting the public know who President Trump was making deals with.

The administration claimed this move was taken as a security measure and also to save the country $70,000 over the next four years. Since the government is projected to spend roughly $16 trillion over the next four years, the savings will be equal to 0.00000004 percent of projected spending. Alternatively, it will save each person in the country 0.007 cents annually over the next four years.

Another comparison that might be useful is that it costs taxpayers more than $3 million in additional security costs every time that President Trump goes to Mar-a-Lago for the weekend. This means that Trump is saving us an amount equal to 2 percent of the cost of one of his weekend trips by keeping the records of his meetings secret.

Source: See text.

Read More Leer más Join the discussion Participa en la discusión

I know Donald Trump is lots of fun and everything, but people should be paying at least a little attention to inflation, or the lack thereof. Remember, last time we tuned in the Federal Reserve Board was embarked on a process of tightening through a sequence of interest rates hikes. The concern expressed by proponents of higher rates was that the economy was too strong and that inflation would soon be rising above its 2.0 percent target. (Actually, the target is supposed to be an average, which means at the peak of a recovery the inflation rate should be somewhat higher than 2.0 percent.)

The March data seems to undermine this concern. While monthly data are erratic, it was striking because both the overall and core rate were negative in the month. The core CPI dropped by 0.1 percent in March, its first decline in more than seven years.

Furthermore, even the modest inflation shown by the core index is largely due to rents. While higher rents do affect people’s cost of living, the Fed is not going to slow rental inflation by raising interest rates. In fact, by slowing construction, the near-term impact of higher interest rates could be to increase inflation in rents.

Over the last year, a core CPI that excludes rent has risen by just 1.0 percent.

Year over Year Change in Core CPI, Excluding Housing

Source: Bureau of Labor Statistics.

I know Donald Trump is lots of fun and everything, but people should be paying at least a little attention to inflation, or the lack thereof. Remember, last time we tuned in the Federal Reserve Board was embarked on a process of tightening through a sequence of interest rates hikes. The concern expressed by proponents of higher rates was that the economy was too strong and that inflation would soon be rising above its 2.0 percent target. (Actually, the target is supposed to be an average, which means at the peak of a recovery the inflation rate should be somewhat higher than 2.0 percent.)

The March data seems to undermine this concern. While monthly data are erratic, it was striking because both the overall and core rate were negative in the month. The core CPI dropped by 0.1 percent in March, its first decline in more than seven years.

Furthermore, even the modest inflation shown by the core index is largely due to rents. While higher rents do affect people’s cost of living, the Fed is not going to slow rental inflation by raising interest rates. In fact, by slowing construction, the near-term impact of higher interest rates could be to increase inflation in rents.

Over the last year, a core CPI that excludes rent has risen by just 1.0 percent.

Year over Year Change in Core CPI, Excluding Housing

Source: Bureau of Labor Statistics.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

The Federal Reserve Board has more direct control over the economy than any other institution in the country. When it decides to raise interest rates to slow the economy, it can ensure that millions of workers don’t get jobs and prevent tens of millions more from getting the bargaining power they need to gain wage increases. For this reason, it is very important who is making the calls on interest rates and who they are listening to.

Robert Rubin, who served as Treasury secretary in the Clinton administration, weighed in today in the NYT to argue for the status quo. There are a few important background points on Rubin that are worth mentioning before getting into the substance.

First. Robert Rubin was a main architect of the high dollar policy that led to the explosion of the trade deficit in the last decade. This led to the loss of millions of manufacturing jobs and decimating communities across the Midwest. Second, Rubin was a major advocate of financial deregulation during his years in the Clinton administration. Finally, Rubin was a direct beneficiary of deregulation, since he left the administration to take a top job at Citigroup. He made over $100 million in this position before he resigned in the financial crisis when bad loans had essentially put Citigroup into bankruptcy. (It was saved by government bailouts.)

Rubin touts the current apolitical nature of the Fed. He warns about:

“Efforts to denigrate the integrity of the Fed’s work, and to inject groundless opinion, politics and ideology, must be rejected by the board — and that means governors and other members of the Federal Open Market Committee must be willing to withstand aggressive attacks.”

It is important to recognize that the Fed is currently dominated by people with close ties to the financial industry. The Fed Open Market Committee (FOMC) which determines interest rate policy has 19 members. While 7 are governors appointed by the president and approved by Congress (only 4 of the governor seats are currently filled), 12 are presidents of the district banks. These bank presidents are appointed through a process dominated by the banks in the district. (Only 5 of the 12 presidents have a vote at any one time, but all 12 participate in discussions.)

It seems bizarre to describe this process as apolitical or imply there is great integrity here. Rubin’s claim is particularly ironic in light of the fact that one of the bank presidents was just forced to resign after admitting to leaking confidential information on interest rate policy to a financial analyst.

There is good reason for the public to be unhappy about the Fed’s excessive concern over inflation over the last four decades and inadequate attention to unemployment. This arguably reflects the interests of the financial industry, which often stands to lose from higher inflation and have little interest in the level of employment. It is understandable that someone who has made his fortune in the financial industry would want to protect the status quo with the Fed, but there is little reason for the rest of us to take him seriously.

The Federal Reserve Board has more direct control over the economy than any other institution in the country. When it decides to raise interest rates to slow the economy, it can ensure that millions of workers don’t get jobs and prevent tens of millions more from getting the bargaining power they need to gain wage increases. For this reason, it is very important who is making the calls on interest rates and who they are listening to.

Robert Rubin, who served as Treasury secretary in the Clinton administration, weighed in today in the NYT to argue for the status quo. There are a few important background points on Rubin that are worth mentioning before getting into the substance.

First. Robert Rubin was a main architect of the high dollar policy that led to the explosion of the trade deficit in the last decade. This led to the loss of millions of manufacturing jobs and decimating communities across the Midwest. Second, Rubin was a major advocate of financial deregulation during his years in the Clinton administration. Finally, Rubin was a direct beneficiary of deregulation, since he left the administration to take a top job at Citigroup. He made over $100 million in this position before he resigned in the financial crisis when bad loans had essentially put Citigroup into bankruptcy. (It was saved by government bailouts.)

Rubin touts the current apolitical nature of the Fed. He warns about:

“Efforts to denigrate the integrity of the Fed’s work, and to inject groundless opinion, politics and ideology, must be rejected by the board — and that means governors and other members of the Federal Open Market Committee must be willing to withstand aggressive attacks.”

It is important to recognize that the Fed is currently dominated by people with close ties to the financial industry. The Fed Open Market Committee (FOMC) which determines interest rate policy has 19 members. While 7 are governors appointed by the president and approved by Congress (only 4 of the governor seats are currently filled), 12 are presidents of the district banks. These bank presidents are appointed through a process dominated by the banks in the district. (Only 5 of the 12 presidents have a vote at any one time, but all 12 participate in discussions.)

It seems bizarre to describe this process as apolitical or imply there is great integrity here. Rubin’s claim is particularly ironic in light of the fact that one of the bank presidents was just forced to resign after admitting to leaking confidential information on interest rate policy to a financial analyst.

There is good reason for the public to be unhappy about the Fed’s excessive concern over inflation over the last four decades and inadequate attention to unemployment. This arguably reflects the interests of the financial industry, which often stands to lose from higher inflation and have little interest in the level of employment. It is understandable that someone who has made his fortune in the financial industry would want to protect the status quo with the Fed, but there is little reason for the rest of us to take him seriously.

Read More Leer más Join the discussion Participa en la discusión