In his recent book, former Fed chair Ben Bernanke claimed that the Fed did not choose to let Lehman fail, he said that it had no choice because it could not bail it out. The NYT is insisting that this account is true.

“During his remarks, Mr. Bernanke sought to dispel a perception that the Fed and other policy makers made a conscious decision to let Lehman Brothers fail. Even today, nearly a decade after the financial crisis, the view still persists among some.

“‘The tools we had were inadequate’ to save Lehman, Mr. Bernanke said. Early efforts to line up a buyer for Lehman – first Bank of America and then the British bank Barclays — failed. The only remaining option was for the Fed to lend Lehman money. But Mr. Bernanke said that Lehman was ‘so deeply in the red’ that the Fed did not have the financial muscle to bail it out.”

The Fed absolutely did have the financial muscle to bail out Lehman. It could have lent the bank as much as it wanted. Legally, the Fed is not supposed to lend to an insolvent bank, but it almost certainly ignored this restriction in lending to Citigroup and Bank of America, as well as other banks, during the crisis.

Had the Fed opted to lend to Lehman, in spite of its being insolvent, it is difficult to imagine who would have stopped it. It is unlikely that the courts would grant legal standing to anyone trying to sue and even if they did, a suit would likely take years to resolve, at which point we would have been through the worst of the crisis.

The decision to let Lehman fail was a decision. It is unfortunate that the NYT is working to help Bernanke rewrite history on this issue.

Note: Typo corrected.

In his recent book, former Fed chair Ben Bernanke claimed that the Fed did not choose to let Lehman fail, he said that it had no choice because it could not bail it out. The NYT is insisting that this account is true.

“During his remarks, Mr. Bernanke sought to dispel a perception that the Fed and other policy makers made a conscious decision to let Lehman Brothers fail. Even today, nearly a decade after the financial crisis, the view still persists among some.

“‘The tools we had were inadequate’ to save Lehman, Mr. Bernanke said. Early efforts to line up a buyer for Lehman – first Bank of America and then the British bank Barclays — failed. The only remaining option was for the Fed to lend Lehman money. But Mr. Bernanke said that Lehman was ‘so deeply in the red’ that the Fed did not have the financial muscle to bail it out.”

The Fed absolutely did have the financial muscle to bail out Lehman. It could have lent the bank as much as it wanted. Legally, the Fed is not supposed to lend to an insolvent bank, but it almost certainly ignored this restriction in lending to Citigroup and Bank of America, as well as other banks, during the crisis.

Had the Fed opted to lend to Lehman, in spite of its being insolvent, it is difficult to imagine who would have stopped it. It is unlikely that the courts would grant legal standing to anyone trying to sue and even if they did, a suit would likely take years to resolve, at which point we would have been through the worst of the crisis.

The decision to let Lehman fail was a decision. It is unfortunate that the NYT is working to help Bernanke rewrite history on this issue.

Note: Typo corrected.

Read More Leer más Join the discussion Participa en la discusión

A NYT article on the prospects of an interest rate hike by the Federal Reserve Board at its December meeting told readers:

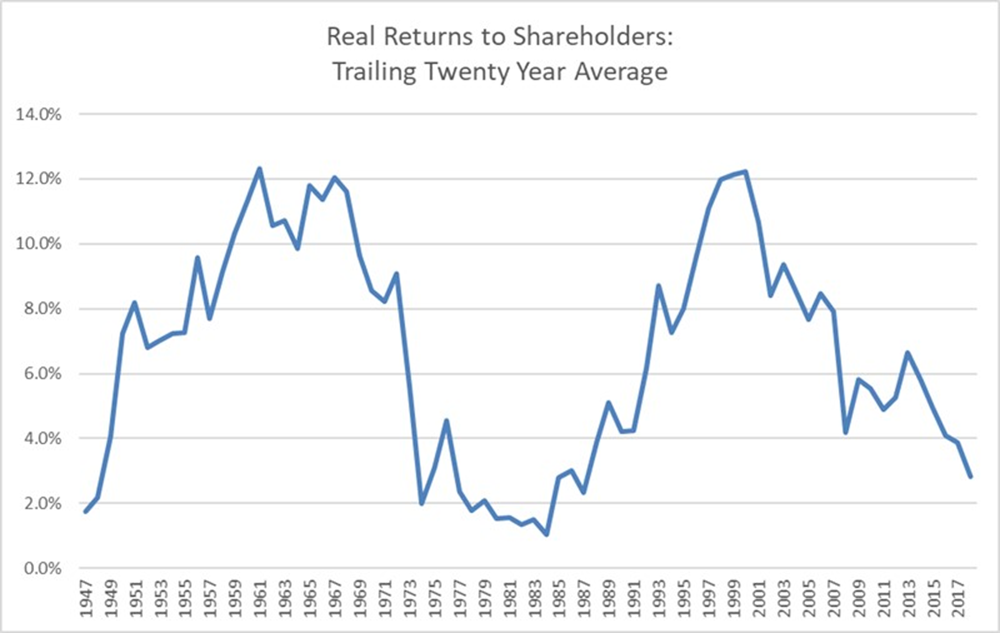

“The case for raising rates hinges in part on the Fed’s forecast that the economy will continue to add jobs at a healthy pace and that inflation will begin to rise more quickly. Moreover, some analysts argue that maintaining near-zero interest rates is now doing more harm than good by encouraging businesses to invest in things like share buybacks to lift their stock price, rather than long-term investments in equipment and developing new products.”

It’s difficult to see how low interest rates would cause firms to prefer share buybacks to long-term investment. Low interest rates make the cost of borrowing lower. This could lead some firms to carry more debt and use cash for share buybacks or dividends. But low interest rates also make it easier to borrow for long-term investment. There is no obvious mechanism through which low interest rates would lead firms to divert money from investment to share buybacks.

If low interest rates eventually led to enough growth that it pushed up the rate of inflation, then they could provide a boost to investment at the expense of buybacks (higher inflation means that the output will sell for more, raising profits, other things equal). It is difficult to see how low interest rates could cause buybacks to increase at the expense of investment.

A NYT article on the prospects of an interest rate hike by the Federal Reserve Board at its December meeting told readers:

“The case for raising rates hinges in part on the Fed’s forecast that the economy will continue to add jobs at a healthy pace and that inflation will begin to rise more quickly. Moreover, some analysts argue that maintaining near-zero interest rates is now doing more harm than good by encouraging businesses to invest in things like share buybacks to lift their stock price, rather than long-term investments in equipment and developing new products.”

It’s difficult to see how low interest rates would cause firms to prefer share buybacks to long-term investment. Low interest rates make the cost of borrowing lower. This could lead some firms to carry more debt and use cash for share buybacks or dividends. But low interest rates also make it easier to borrow for long-term investment. There is no obvious mechanism through which low interest rates would lead firms to divert money from investment to share buybacks.

If low interest rates eventually led to enough growth that it pushed up the rate of inflation, then they could provide a boost to investment at the expense of buybacks (higher inflation means that the output will sell for more, raising profits, other things equal). It is difficult to see how low interest rates could cause buybacks to increase at the expense of investment.

Read More Leer más Join the discussion Participa en la discusión

Economists constantly have difficulties figuring out what problem we are trying to solve. The NYT’s discussion of the Chinese government’s decision to switch to a policy that allows most families to have two children, instead of just one, provides an excellent illustration of this situation. At one point the piece explains the policy shift:

“Now the party leadership has acted more forcefully, apparently in the hope that a burst of children will replenish the nation’s work force and encourage more consumer spending.”

The idea of having more children to increase the size of the labor force implies that the problem facing China is inadequate supply. (This is more than a bit peculiar given the enormous growth in productivity in the last three decades. Productivity growth, means more output per worker. It has the same impact on supply as having more workers.)

However, the concern about boosting spending, expressed repeatedly throughout the article, is a concern about lack of demand. At any point in time an economy can be suffering from either supply shortages stemming from a lack of workers or demand shortages because people don’t spend enough to keep the labor force employed. It doesn’t make sense for it to be suffering from both at the same time.

Economists constantly have difficulties figuring out what problem we are trying to solve. The NYT’s discussion of the Chinese government’s decision to switch to a policy that allows most families to have two children, instead of just one, provides an excellent illustration of this situation. At one point the piece explains the policy shift:

“Now the party leadership has acted more forcefully, apparently in the hope that a burst of children will replenish the nation’s work force and encourage more consumer spending.”

The idea of having more children to increase the size of the labor force implies that the problem facing China is inadequate supply. (This is more than a bit peculiar given the enormous growth in productivity in the last three decades. Productivity growth, means more output per worker. It has the same impact on supply as having more workers.)

However, the concern about boosting spending, expressed repeatedly throughout the article, is a concern about lack of demand. At any point in time an economy can be suffering from either supply shortages stemming from a lack of workers or demand shortages because people don’t spend enough to keep the labor force employed. It doesn’t make sense for it to be suffering from both at the same time.

Read More Leer más Join the discussion Participa en la discusión

Hey, who can blame them? It’s an obscure government program with 60 million beneficiaries, with benefits that are so small that they don’t matter to anyone who is anyone.

I’m actually not joking here. The WSJ ran an article telling readers that the average baby boomer between the ages of 55-64 faces a gap of $36,371 between the $45,000 a year they expect to need as income in retirement and the $9,129 they can expect to get based on the savings they have accumulated. The incredible part of the story is that the piece never once mentions Social Security, nor does the Blackrock study on which the article is based.

While Social Security benefits will not fill this gap, they will be by far the largest part of the retirement income of most middle income retirees. The average worker’s retirement benefit is roughly $16,000 a year. If this is a couple, then the spouse can count a benefit of at least $8,000 unless his work history entitled him to a larger benefit. Together with the savings accumulations estimated by Blackrock, this is still likely to leave most middle income couples well below the $45,000 comfort level that the study found, but they are far closer than the discussion in the WSJ article implied.

Hey, who can blame them? It’s an obscure government program with 60 million beneficiaries, with benefits that are so small that they don’t matter to anyone who is anyone.

I’m actually not joking here. The WSJ ran an article telling readers that the average baby boomer between the ages of 55-64 faces a gap of $36,371 between the $45,000 a year they expect to need as income in retirement and the $9,129 they can expect to get based on the savings they have accumulated. The incredible part of the story is that the piece never once mentions Social Security, nor does the Blackrock study on which the article is based.

While Social Security benefits will not fill this gap, they will be by far the largest part of the retirement income of most middle income retirees. The average worker’s retirement benefit is roughly $16,000 a year. If this is a couple, then the spouse can count a benefit of at least $8,000 unless his work history entitled him to a larger benefit. Together with the savings accumulations estimated by Blackrock, this is still likely to leave most middle income couples well below the $45,000 comfort level that the study found, but they are far closer than the discussion in the WSJ article implied.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

The NYT had a largely negative assessment of Abenomics, implying that it had done little to improve the state of Japan’s economy in the last two and a half years. The piece never mentions the surge in employment in Japan over this period. The overall employment rate for workers age 16-64 rose by 2.4 percentage points since the fourth quarter of 2012. This compares to a rise of 1.2 percentage points in the United States in a period in which the pace of job growth has been widely touted. If the United States had the same growth in employment rates as Japan under Abenomics, it would translate into another 2.4 million jobs.

Employment growth among women has been especially impressive, rising by 3.6 percentage points over this period. The employment rate for women is now a full percentage point higher than in the United States.

The NYT had a largely negative assessment of Abenomics, implying that it had done little to improve the state of Japan’s economy in the last two and a half years. The piece never mentions the surge in employment in Japan over this period. The overall employment rate for workers age 16-64 rose by 2.4 percentage points since the fourth quarter of 2012. This compares to a rise of 1.2 percentage points in the United States in a period in which the pace of job growth has been widely touted. If the United States had the same growth in employment rates as Japan under Abenomics, it would translate into another 2.4 million jobs.

Employment growth among women has been especially impressive, rising by 3.6 percentage points over this period. The employment rate for women is now a full percentage point higher than in the United States.

Read More Leer más Join the discussion Participa en la discusión

In his review of former Fed Chair Ben Bernanke’s new book, Michael Kinsley tells us:

“Bernanke makes a compelling case that in 2007 and 2008, the world economy came very close to collapse, and only novel efforts by the Fed (cooperating with other United States and foreign government agencies) saved us from an economic catastrophe greater than the Great Depression.”

The Great Depression lasted for more than a decade because the government did not spend enough money to get the economy back to a normal level of output. It eventually did get the economy back to full employment due to the spending associated with World War II. If the government had undertaken similar spending in 1931, for example to build up the infrastructure and to expand the provision of education and health care, the depression would have ended a decade sooner.

Unless there is some reason the United States government could not have spent money in 2009 if the banks had collapsed in 2008, then we did not have to worry about a Second Great Depression. No one has yet indicated what that reason could be. Even Republicans have consistently supported stimulus during downturns. (George W. Bush signed the first stimulus package in February of 2008 when the unemployment rate was 4.7 percent.) So the story of being saved from the Second Great Depression is entirely a myth that can be used to justify the bailout of the Wall Street banks.

In his review of former Fed Chair Ben Bernanke’s new book, Michael Kinsley tells us:

“Bernanke makes a compelling case that in 2007 and 2008, the world economy came very close to collapse, and only novel efforts by the Fed (cooperating with other United States and foreign government agencies) saved us from an economic catastrophe greater than the Great Depression.”

The Great Depression lasted for more than a decade because the government did not spend enough money to get the economy back to a normal level of output. It eventually did get the economy back to full employment due to the spending associated with World War II. If the government had undertaken similar spending in 1931, for example to build up the infrastructure and to expand the provision of education and health care, the depression would have ended a decade sooner.

Unless there is some reason the United States government could not have spent money in 2009 if the banks had collapsed in 2008, then we did not have to worry about a Second Great Depression. No one has yet indicated what that reason could be. Even Republicans have consistently supported stimulus during downturns. (George W. Bush signed the first stimulus package in February of 2008 when the unemployment rate was 4.7 percent.) So the story of being saved from the Second Great Depression is entirely a myth that can be used to justify the bailout of the Wall Street banks.

Read More Leer más Join the discussion Participa en la discusión

A Washington Post editorial arguing for the adoption of a budget proposal put forward by Representative Scott Rigell applauded the plan’s call for using the chained CPI for indexing all taxes and benefits, including Social Security. It described the chained CPI as “more accurate.”

The chained CPI will typically show a lower rate of inflation than the CPI currently used since it accounts for substitutions in consumption, as people change their consumption patterns in response to changes in prices. (It changes the weights in the index assigned to different price increases, it doesn’t count savings from switching from more expensive to less expensive items.)

While there is an argument for picking up the impact of substitution, it is important to note that this may not be valid for the senior population that relies on Social Security. It is possible that seniors are less likely to change their consumption patterns by switching items or outlets in response to price increases. We could determine whether or not this is the case by constructing a full price index for the elderly, which would track the prices of the specific goods and services they consume and look at the outlets where they buy them.

This is what Congress would do if it was interested in an accurate measure of the rate of price increase experienced by seniors. Switching to the chained CPI will mean lower benefits (@ 3 percent for the average senior over the course of their retirement), the Post has no clue as to whether it would be more accurate.

A Washington Post editorial arguing for the adoption of a budget proposal put forward by Representative Scott Rigell applauded the plan’s call for using the chained CPI for indexing all taxes and benefits, including Social Security. It described the chained CPI as “more accurate.”

The chained CPI will typically show a lower rate of inflation than the CPI currently used since it accounts for substitutions in consumption, as people change their consumption patterns in response to changes in prices. (It changes the weights in the index assigned to different price increases, it doesn’t count savings from switching from more expensive to less expensive items.)

While there is an argument for picking up the impact of substitution, it is important to note that this may not be valid for the senior population that relies on Social Security. It is possible that seniors are less likely to change their consumption patterns by switching items or outlets in response to price increases. We could determine whether or not this is the case by constructing a full price index for the elderly, which would track the prices of the specific goods and services they consume and look at the outlets where they buy them.

This is what Congress would do if it was interested in an accurate measure of the rate of price increase experienced by seniors. Switching to the chained CPI will mean lower benefits (@ 3 percent for the average senior over the course of their retirement), the Post has no clue as to whether it would be more accurate.

Read More Leer más Join the discussion Participa en la discusión

I realize that this may come as a shock to the reporters and editors at the NYT, but companies are sometimes not truthful. That is why when G.E. announced that it was closing a factory in Wisconsin because it no longer had access to subsidized loans through the Export-Import Bank, the article should have said something to the effect of “G.E. claims to be closing factory because of lack of access to Export-Import Bank loans.” A serious newspaper would not take the assertion at face value and headline the article, “Ex-Im Bank Dispute Threatens G.E. Factory that Obama Praised.”

The New York Times has many outstanding reporters, but they don’t have any easy way of knowing if, for example, G.E. had plans to close this factory regardless of the fate of the Export-Import Bank. In that case, blaming the bank for the closure would be a convenient way to try to pressure Congress to renew funding.

If we try to guess the size of the subsidy that G.E. gets from the bank, if we assume that it might be $3 billion in loans or guarantees this year, with an average subsidy of 1.0 percentage point compared to the market interest rate, this comes to $30 million. By comparison, G.E. CEO Jeffrey Immelt received $37.2 million in compensation last year.

This would suggest that the subsidies that G.E. receives from the Ex-Im Bank are relatively small compared to the compensation of Mr. Immelt and other top executives. Cuts to their pay would be another possible route for keeping the Wisconsin plant operating.

Addendum:

It is worth noting that G.E.’s allegation is that the loss of a government subsidy is causing it to close a factory. It is not common for the NYT to highlight when a factory is closed due to the loss of a protective tariff. If the paper has a different attitude towards subsidies and tariffs it would be interesting to hear the basis for this position. Certainly it would not be justified in conventional economics.

Note: Typo corrected, thanks ltr and Robert Salzberg.

I realize that this may come as a shock to the reporters and editors at the NYT, but companies are sometimes not truthful. That is why when G.E. announced that it was closing a factory in Wisconsin because it no longer had access to subsidized loans through the Export-Import Bank, the article should have said something to the effect of “G.E. claims to be closing factory because of lack of access to Export-Import Bank loans.” A serious newspaper would not take the assertion at face value and headline the article, “Ex-Im Bank Dispute Threatens G.E. Factory that Obama Praised.”

The New York Times has many outstanding reporters, but they don’t have any easy way of knowing if, for example, G.E. had plans to close this factory regardless of the fate of the Export-Import Bank. In that case, blaming the bank for the closure would be a convenient way to try to pressure Congress to renew funding.

If we try to guess the size of the subsidy that G.E. gets from the bank, if we assume that it might be $3 billion in loans or guarantees this year, with an average subsidy of 1.0 percentage point compared to the market interest rate, this comes to $30 million. By comparison, G.E. CEO Jeffrey Immelt received $37.2 million in compensation last year.

This would suggest that the subsidies that G.E. receives from the Ex-Im Bank are relatively small compared to the compensation of Mr. Immelt and other top executives. Cuts to their pay would be another possible route for keeping the Wisconsin plant operating.

Addendum:

It is worth noting that G.E.’s allegation is that the loss of a government subsidy is causing it to close a factory. It is not common for the NYT to highlight when a factory is closed due to the loss of a protective tariff. If the paper has a different attitude towards subsidies and tariffs it would be interesting to hear the basis for this position. Certainly it would not be justified in conventional economics.

Note: Typo corrected, thanks ltr and Robert Salzberg.

Read More Leer más Join the discussion Participa en la discusión

In a NYT review of Roger Lowenstein’s book on the Federal Reserve Board, Robert Rubin touts the virtues of the Fed’s independence from political control. He decries efforts to make the Fed more accountable to Congress.

While the Fed may not feel as though it must directly respond to Congress, that does not mean it is not responsive to political pressures. In the last thirty five years, it has maintained policies that have on average kept the unemployment rate almost a full percentage point above the Congressional Budget Office’s estimate of the non-accelerating inflation rate of unemployment (0.5 percentage points excluding the Great Recession). By contrast, in the prior three decades the unemployment rate had averaged half a percentage point less than CBO’s estimate of the NAIRU.

Source: Baker and Bernstein, 2013.

The higher unemployment acts as an insurance policy against inflation. The higher unemployment kept millions of people from working and deprived tens of millions of workers of the bargaining power needed to secure real wage increases. While modestly higher inflation would be a matter of little concern to most workers (especially since it is being driven in part by higher wages), it would be very upsetting to the financial sector since the value of the debt they own would be reduced.

The financial industry has a grossly disproportionate influence on the Fed due to its design. They largely control the 12 district banks. In addition, the governors appointed by the president tend to be more responsive to the concerns of the financial industry than other sectors of the economy. It is certainly possible that if the Fed were not so tied to the financial industry, it would have paid more attention to the housing bubble as it was growing. The industry made huge amounts of money from the mortgages that fueled the bubble. (In this context, it is probably worth noting that Mr. Rubin made more than $100 million from his position as a top executive at Citigroup during the bubble years.)

For these reasons, the public may not be as happy about the Fed’s lack of accountability to democratically elected bodies as Mr. Rubin. Many might prefer a central bank that is concerned more about workers than bankers.

Addendum:

On this topic, it is probably worth noting that in 2014 Robert Rubin, together with Martin Feldstein, argued that the Fed should be prepared to use higher interest rates as a tool to combat bubbles.

In a NYT review of Roger Lowenstein’s book on the Federal Reserve Board, Robert Rubin touts the virtues of the Fed’s independence from political control. He decries efforts to make the Fed more accountable to Congress.

While the Fed may not feel as though it must directly respond to Congress, that does not mean it is not responsive to political pressures. In the last thirty five years, it has maintained policies that have on average kept the unemployment rate almost a full percentage point above the Congressional Budget Office’s estimate of the non-accelerating inflation rate of unemployment (0.5 percentage points excluding the Great Recession). By contrast, in the prior three decades the unemployment rate had averaged half a percentage point less than CBO’s estimate of the NAIRU.

Source: Baker and Bernstein, 2013.

The higher unemployment acts as an insurance policy against inflation. The higher unemployment kept millions of people from working and deprived tens of millions of workers of the bargaining power needed to secure real wage increases. While modestly higher inflation would be a matter of little concern to most workers (especially since it is being driven in part by higher wages), it would be very upsetting to the financial sector since the value of the debt they own would be reduced.

The financial industry has a grossly disproportionate influence on the Fed due to its design. They largely control the 12 district banks. In addition, the governors appointed by the president tend to be more responsive to the concerns of the financial industry than other sectors of the economy. It is certainly possible that if the Fed were not so tied to the financial industry, it would have paid more attention to the housing bubble as it was growing. The industry made huge amounts of money from the mortgages that fueled the bubble. (In this context, it is probably worth noting that Mr. Rubin made more than $100 million from his position as a top executive at Citigroup during the bubble years.)

For these reasons, the public may not be as happy about the Fed’s lack of accountability to democratically elected bodies as Mr. Rubin. Many might prefer a central bank that is concerned more about workers than bankers.

Addendum:

On this topic, it is probably worth noting that in 2014 Robert Rubin, together with Martin Feldstein, argued that the Fed should be prepared to use higher interest rates as a tool to combat bubbles.

Read More Leer más Join the discussion Participa en la discusión