The hit to Europe’s economy from the collapse of its housing bubbles has been larger than the downturn it suffered in the Great Depression. So naturally the assessment of columnist Charles Lane on the Post op-ed page is:

“So far, Merkel has managed the crisis of the euro zone well.”

It’s not clear what would count as managing the crisis poorly, although Lane does tell us in the next sentence that in his view the breakup of the euro would be the ultimate disaster. If keeping the euro together is the sole criterion, regardless of how many trillions of dollars of lost output results, and however many millions of lives are ruined by prolonged unemployment, then I guess the euro crew is a winner.

Lane’s piece is deeply mired in confusion. Early on he tells readers;

“Two contradictory fears threaten these Germans’ contentment: what might happen if the government spends their hard-earned national savings on a bailout for Greece or Italy, and what might happen to Europe if someone doesn’t prop up those spendthrifts.”

Of course the most obvious route to restarting Europe’s economy would be to have the European Central Bank (ECB) act like a central bank and agree to underwrite the sort of deficits that will be needed to bring Europe’s economy back to full employment. This does not require using any of Germany’s savings. In fact, by boosting Europe’s growth it is likely to increase Germany’s “hard-earned national savings.”

Lane is also confused about the nature of budget deficits in Europe when referring to Greece and Italy as “spendthrifts.” While the former characterization has some real foundation, this description of Italy might seem a bit dubious to folks familiar with the data. Here’s a chart showing the primary deficits (this excludes interest payments) of two euro zone countries since 2000.

Source: International Monetary Fund.

Source: International Monetary Fund.

If you guessed that Country B, the one that has generally had the larger primary budget surplus, is that spendthrift Italy, you got it right. In fact, Italy has had substantial primary budget surpluses for most of this century. It did have a large debt built up over prior decades which gives it a large interest burden now. The other reason that it has a large interest burden at present is the decision by the ECB to maintain a degree of ambiguity as to whether it would stand behind Italy’s debt. If it ended this ambiguity, the interest rate on Italy’s debt would be little different than the interest rate on German debt. This would make the country’s debt burden easily manageable.

Note: Country reversal corrected, thanks Joe.

The hit to Europe’s economy from the collapse of its housing bubbles has been larger than the downturn it suffered in the Great Depression. So naturally the assessment of columnist Charles Lane on the Post op-ed page is:

“So far, Merkel has managed the crisis of the euro zone well.”

It’s not clear what would count as managing the crisis poorly, although Lane does tell us in the next sentence that in his view the breakup of the euro would be the ultimate disaster. If keeping the euro together is the sole criterion, regardless of how many trillions of dollars of lost output results, and however many millions of lives are ruined by prolonged unemployment, then I guess the euro crew is a winner.

Lane’s piece is deeply mired in confusion. Early on he tells readers;

“Two contradictory fears threaten these Germans’ contentment: what might happen if the government spends their hard-earned national savings on a bailout for Greece or Italy, and what might happen to Europe if someone doesn’t prop up those spendthrifts.”

Of course the most obvious route to restarting Europe’s economy would be to have the European Central Bank (ECB) act like a central bank and agree to underwrite the sort of deficits that will be needed to bring Europe’s economy back to full employment. This does not require using any of Germany’s savings. In fact, by boosting Europe’s growth it is likely to increase Germany’s “hard-earned national savings.”

Lane is also confused about the nature of budget deficits in Europe when referring to Greece and Italy as “spendthrifts.” While the former characterization has some real foundation, this description of Italy might seem a bit dubious to folks familiar with the data. Here’s a chart showing the primary deficits (this excludes interest payments) of two euro zone countries since 2000.

Source: International Monetary Fund.

If you guessed that Country B, the one that has generally had the larger primary budget surplus, is that spendthrift Italy, you got it right. In fact, Italy has had substantial primary budget surpluses for most of this century. It did have a large debt built up over prior decades which gives it a large interest burden now. The other reason that it has a large interest burden at present is the decision by the ECB to maintain a degree of ambiguity as to whether it would stand behind Italy’s debt. If it ended this ambiguity, the interest rate on Italy’s debt would be little different than the interest rate on German debt. This would make the country’s debt burden easily manageable.

Note: Country reversal corrected, thanks Joe.

Read More Leer más Join the discussion Participa en la discusión

That is undoubtedly the question that many NYT readers were asking when they read an article warning that insurance companies in the exchanges were not paying enough money to attract many doctors. At one point the piece told readers;

“Dr. Barbara L. McAneny, a cancer specialist in Albuquerque, said that insurers in the New Mexico exchange were generally paying doctors at Medicare levels, which she said were ‘often below our cost of doing business, and definitely below commercial rates.'”

The claim that Medicare payments are “below our cost of doing business” might seem rather dubious to readers since most doctors accept Medicare patients. The median earnings of physicians are well over $200,000 a year (net of malpractice insurance), which means they are heavily represented in the one percent. Given their extraordinary incomes, which they vigorously protect by excluding foreign and domestic competition, it seems implausible that many doctors are willing to lose money by treating Medicare patients.

It is more likely that doctors are getting less than their desired pay when they treat Medicare patients, but still pocketing far more money than the overwhelming majority workers for their time. It would have been useful to clarify this point for readers rather than letting Doctor McAneny’s assertion pass unchallenged.

That is undoubtedly the question that many NYT readers were asking when they read an article warning that insurance companies in the exchanges were not paying enough money to attract many doctors. At one point the piece told readers;

“Dr. Barbara L. McAneny, a cancer specialist in Albuquerque, said that insurers in the New Mexico exchange were generally paying doctors at Medicare levels, which she said were ‘often below our cost of doing business, and definitely below commercial rates.'”

The claim that Medicare payments are “below our cost of doing business” might seem rather dubious to readers since most doctors accept Medicare patients. The median earnings of physicians are well over $200,000 a year (net of malpractice insurance), which means they are heavily represented in the one percent. Given their extraordinary incomes, which they vigorously protect by excluding foreign and domestic competition, it seems implausible that many doctors are willing to lose money by treating Medicare patients.

It is more likely that doctors are getting less than their desired pay when they treat Medicare patients, but still pocketing far more money than the overwhelming majority workers for their time. It would have been useful to clarify this point for readers rather than letting Doctor McAneny’s assertion pass unchallenged.

Read More Leer más Join the discussion Participa en la discusión

Robert Samuelson used his column to tell readers that people in the United States really are different than in other countries. Samuelson wrote:

“One standard question asks respondents to judge which is more important — ‘freedom to pursue life’s goals without state interference’ or ‘state guarantees [that] nobody is in need.’ By a 58?percent to 35 percent margin, Americans favored freedom over security, reported a 2011 Pew survey. In Europe, opinion was the opposite. Germans valued protections over freedom 62 percent to 36 percent. The results were similar for France, Britain and Spain.”

There are many people in the United States who do not recognize that Medicare is a government program. (Hence the frequent demand from Tea Party conservatives that the government keeps its hands off their Medicare.) It is likely they believe the same about Social Security. These people may highly value the security provided by these programs while at the same time denigrating the importance of state guarantees because they don’t recognize the connection of these programs to the state.

Insofar as this is the case, the difference in polling on this question may reflect differences in knowledge rather than differences in values.

Robert Samuelson used his column to tell readers that people in the United States really are different than in other countries. Samuelson wrote:

“One standard question asks respondents to judge which is more important — ‘freedom to pursue life’s goals without state interference’ or ‘state guarantees [that] nobody is in need.’ By a 58?percent to 35 percent margin, Americans favored freedom over security, reported a 2011 Pew survey. In Europe, opinion was the opposite. Germans valued protections over freedom 62 percent to 36 percent. The results were similar for France, Britain and Spain.”

There are many people in the United States who do not recognize that Medicare is a government program. (Hence the frequent demand from Tea Party conservatives that the government keeps its hands off their Medicare.) It is likely they believe the same about Social Security. These people may highly value the security provided by these programs while at the same time denigrating the importance of state guarantees because they don’t recognize the connection of these programs to the state.

Insofar as this is the case, the difference in polling on this question may reflect differences in knowledge rather than differences in values.

Read More Leer más Join the discussion Participa en la discusión

This is an impressive accomplishment that deserves some attention.

This is an impressive accomplishment that deserves some attention.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

The Washington Post had an interesting article on the sharp rise in disability rates in the downturn. It would have been helpful to include some additional information.

One important reason for the rise in disability not connected to the recession, is the increase in the normal retirement age. This was increased from 65 for people who turned 62 before 2002, to 66 for people who turned 62 after 2008. The rise in the normal retirement age means that people on disability can collect benefits for an extra year before they have to turn to their Social Security retirement benefits, which will typically be less. The increase in the retirement age would have led to a substantial rise in disability rates even if there had been no underlying change in the incidence of disability.

A second point that would have been worth noting is that it is not easy to get disability. More than 60 percent of applicants are originally ruled ineligible. While many successfully appeal their rejection, the final approval rate is still below 50 percent. It is reasonable to believe that the vast majority of frivolous claims are rejected.

At one point the article discusses the notion put forward by economists David Autor and Mark Duggan that workers with little education may have substantial incentives to turn to disability:

“Benefits are hardly generous. They average $1,130 a month, and recipients are eligible for Medicare after two years. But with workers without a high school diploma earning a median wage of $471 per week, disability benefits are increasingly attractive for the large share of American workers who have seen both their pay and job options constricted.

“In 2004, nearly one in five male high school dropouts between ages 55 and 64 were in the disability program, according to a paper by economists David Autor and Mark Duggan. That rate was more than double that of high school graduates of the same age in the program and more than five times higher than the 3.7 percent of college graduates of that age who collect disability.”

While the difference between median earnings and the average disability payment is considerably lower for less-educated workers there are two other important factors that affect disability rates. First, less educated workers are far more likely to have worked at physically demanding jobs that could result in a disability. For example, someone who works as a mover is more likely to develop back problems than an office worker with a desk job.

The other difference is that the jobs that are available to less educated workers are likely to be more physically demanding. A back problem that may be an inconvenience for a desk worker may make it impossible for someone to find work as a custodian or some other low-paying job. These differences undoubtedly explain much of the difference in disability rates by education.

The Washington Post had an interesting article on the sharp rise in disability rates in the downturn. It would have been helpful to include some additional information.

One important reason for the rise in disability not connected to the recession, is the increase in the normal retirement age. This was increased from 65 for people who turned 62 before 2002, to 66 for people who turned 62 after 2008. The rise in the normal retirement age means that people on disability can collect benefits for an extra year before they have to turn to their Social Security retirement benefits, which will typically be less. The increase in the retirement age would have led to a substantial rise in disability rates even if there had been no underlying change in the incidence of disability.

A second point that would have been worth noting is that it is not easy to get disability. More than 60 percent of applicants are originally ruled ineligible. While many successfully appeal their rejection, the final approval rate is still below 50 percent. It is reasonable to believe that the vast majority of frivolous claims are rejected.

At one point the article discusses the notion put forward by economists David Autor and Mark Duggan that workers with little education may have substantial incentives to turn to disability:

“Benefits are hardly generous. They average $1,130 a month, and recipients are eligible for Medicare after two years. But with workers without a high school diploma earning a median wage of $471 per week, disability benefits are increasingly attractive for the large share of American workers who have seen both their pay and job options constricted.

“In 2004, nearly one in five male high school dropouts between ages 55 and 64 were in the disability program, according to a paper by economists David Autor and Mark Duggan. That rate was more than double that of high school graduates of the same age in the program and more than five times higher than the 3.7 percent of college graduates of that age who collect disability.”

While the difference between median earnings and the average disability payment is considerably lower for less-educated workers there are two other important factors that affect disability rates. First, less educated workers are far more likely to have worked at physically demanding jobs that could result in a disability. For example, someone who works as a mover is more likely to develop back problems than an office worker with a desk job.

The other difference is that the jobs that are available to less educated workers are likely to be more physically demanding. A back problem that may be an inconvenience for a desk worker may make it impossible for someone to find work as a custodian or some other low-paying job. These differences undoubtedly explain much of the difference in disability rates by education.

Read More Leer más Join the discussion Participa en la discusión

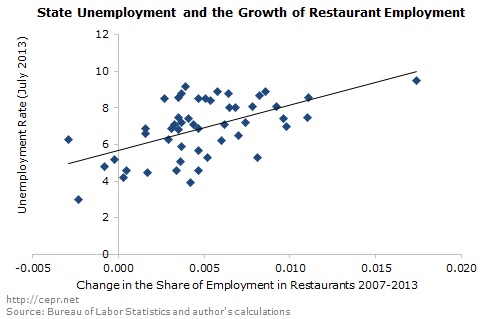

Laura Tyson used her NYT column to warn about increasing wage inequality as more middle class jobs are eliminated. The centerpiece in this argument is that most of the jobs being created in the recovery are in low-paying sectors of the economy. In effect retail and restaurant jobs are replacing manufacturing and construction jobs.

This is a serious concern, since obviously we care not just that workers have jobs, but also that the jobs pay enough to support them and their families. However, the story of job quality and the story of too few jobs are arguably the same story. There are always employers offering bad jobs, but workers don’t take them in a good economy. In a bad economy they have no choice.

The chart below shows the relationship by state between the unemployment rate and the increase in the share of restaurant jobs. The upward slope (which is significant at a 1.0 percent level), shows that a higher rate of unemployment is associated with proportionately more growth in restaurant work. (Arin Dube has a related post showing that an increasing number of college educated workers are being employed in fast food restaurants.)

Click for a more detailed version of the graph.

The point here is that the shortage of jobs and the poor quality of the jobs that are being created are not different stories, they are the same story. The fact that we see the highest rise in the share of restaurant employment in states with the highest unemployment rates indicates that these low-paying jobs are associated with weak growth rather than being the direction of the future economy. If we got more job growth, then the share of low-paying jobs would surely diminish.

As another angle on this, even the wages in low-paying jobs would likely rise if we again got the economy close to full employment levels of output. This was certainly the case in the late 1990s when even workers at the bottom of the pay ladder were seeing substantial gains in wages.

This is not to say that we don’t have structural problems in the economy. An out of control financial sector continues to siphon off hundreds of billions of dollars a year from the productive economy. Our health care system is incredibly wasteful, causing us to pay more than twice as much per person as the average for other wealthy countries. However, the bad jobs story is largely the same thing as the too few jobs story. If we can just get the forbidden topics of stimulus or a lower valued dollar back on the agenda, we could address both.

Laura Tyson used her NYT column to warn about increasing wage inequality as more middle class jobs are eliminated. The centerpiece in this argument is that most of the jobs being created in the recovery are in low-paying sectors of the economy. In effect retail and restaurant jobs are replacing manufacturing and construction jobs.

This is a serious concern, since obviously we care not just that workers have jobs, but also that the jobs pay enough to support them and their families. However, the story of job quality and the story of too few jobs are arguably the same story. There are always employers offering bad jobs, but workers don’t take them in a good economy. In a bad economy they have no choice.

The chart below shows the relationship by state between the unemployment rate and the increase in the share of restaurant jobs. The upward slope (which is significant at a 1.0 percent level), shows that a higher rate of unemployment is associated with proportionately more growth in restaurant work. (Arin Dube has a related post showing that an increasing number of college educated workers are being employed in fast food restaurants.)

Click for a more detailed version of the graph.

The point here is that the shortage of jobs and the poor quality of the jobs that are being created are not different stories, they are the same story. The fact that we see the highest rise in the share of restaurant employment in states with the highest unemployment rates indicates that these low-paying jobs are associated with weak growth rather than being the direction of the future economy. If we got more job growth, then the share of low-paying jobs would surely diminish.

As another angle on this, even the wages in low-paying jobs would likely rise if we again got the economy close to full employment levels of output. This was certainly the case in the late 1990s when even workers at the bottom of the pay ladder were seeing substantial gains in wages.

This is not to say that we don’t have structural problems in the economy. An out of control financial sector continues to siphon off hundreds of billions of dollars a year from the productive economy. Our health care system is incredibly wasteful, causing us to pay more than twice as much per person as the average for other wealthy countries. However, the bad jobs story is largely the same thing as the too few jobs story. If we can just get the forbidden topics of stimulus or a lower valued dollar back on the agenda, we could address both.

Read More Leer más Join the discussion Participa en la discusión

When it comes to issues of an aging population the Washington Post gets very arithmetic challenged. An article discussing the plight of the rural elderly noted that many can’t count on assistance from either the government or their children. It tells readers:

“The rapid aging of China’s society is one of its most profound economic challenges. By 2053, the number of senior citizens is expected to grow to 487 million, or 35 percent of the population, compared with just over 12 percent now, according to the China National Committee on Aging. There will be more retired Chinese people than the entire U.S. population by that date.

“But even before then, the country faces the prospect of growing old before it grows rich. Chinese citizens who have grown up under the one-child policy could end up caring for two parents and four grandparents each as they enter late middle age, a potentially crippling economic burden.”

These assertions are wrong on their face. According to the International Monetary Fund, China’s per capita income has increased by 4000 percent since 1980. This means that it easily has the ability to support both its retirees and its working population at standards of livings that are far higher than they would have seen in the recent past. The impact of this extraordinary growth rate dwarfs the demographics associated with the one-child policy.

If there are problems supporting China’s elderly then it is due to too much money going to the wealthy. The focus on the demographics is mistaken and misleading.

When it comes to issues of an aging population the Washington Post gets very arithmetic challenged. An article discussing the plight of the rural elderly noted that many can’t count on assistance from either the government or their children. It tells readers:

“The rapid aging of China’s society is one of its most profound economic challenges. By 2053, the number of senior citizens is expected to grow to 487 million, or 35 percent of the population, compared with just over 12 percent now, according to the China National Committee on Aging. There will be more retired Chinese people than the entire U.S. population by that date.

“But even before then, the country faces the prospect of growing old before it grows rich. Chinese citizens who have grown up under the one-child policy could end up caring for two parents and four grandparents each as they enter late middle age, a potentially crippling economic burden.”

These assertions are wrong on their face. According to the International Monetary Fund, China’s per capita income has increased by 4000 percent since 1980. This means that it easily has the ability to support both its retirees and its working population at standards of livings that are far higher than they would have seen in the recent past. The impact of this extraordinary growth rate dwarfs the demographics associated with the one-child policy.

If there are problems supporting China’s elderly then it is due to too much money going to the wealthy. The focus on the demographics is mistaken and misleading.

Read More Leer más Join the discussion Participa en la discusión

The Hill sees the onset of fall as providing support for Republican efforts to cut the budget. Okay, they didn’t quite say this, but what they did say didn’t make much more sense. It told readers:

“Republicans argue that their cost-cutting initiatives will foster the economic growth needed to reduce the stubbornly high poverty rate. Their efforts were boosted by a Congressional Budget Office report on Tuesday that shows the national debt increasing to from 73 percent to 100 percent of the economy over the next 25 years.”

The Hill sees the onset of fall as providing support for Republican efforts to cut the budget. Okay, they didn’t quite say this, but what they did say didn’t make much more sense. It told readers:

“Republicans argue that their cost-cutting initiatives will foster the economic growth needed to reduce the stubbornly high poverty rate. Their efforts were boosted by a Congressional Budget Office report on Tuesday that shows the national debt increasing to from 73 percent to 100 percent of the economy over the next 25 years.”

Read More Leer más Join the discussion Participa en la discusión