The NYT has a nice piece on how Goldman Sachs has gotten into the aluminum business in a big way in recent years. The discussion of how it uses its control over inventories to jack up prices is fascinating. There are several interesting take-aways.

First, the piece suggests that the impact on price is limited (7 percent, if their estimates are right), but worth a huge amount given the volumes involved. This is what I had always assumed about the extent to which this sort of speculation can affect the price of products. Speculation might add 20-30 cents to the price of gas, but it can’t explain why we are paying $4.00 a gallon rather than $1.50 a gallon.

Second, there is nothing unique to financial firms that allow them to speculate in this way. Yes, Goldman Sachs has lots of money, but so does Alcoa and many other non-financial companies. If a company can corner the market in major commodities then it indicates a failure first and foremost of anti-trust regulation.

Third, this should reinforce the argument for a new Glass-Steagall. The guarantees provided by the FDIC and Fed to commercial banks reflect their unique importance in maintaining the system of payments in the economy. There is no reason that banks should be able to exploit these guarantees to assist themselves in raising the money needed to corner the aluminum market. If Goldman wants to speculate in aluminum then it should not be a bank holding company. That one should be a no-brainer, except for the corruption of the political system.

The NYT has a nice piece on how Goldman Sachs has gotten into the aluminum business in a big way in recent years. The discussion of how it uses its control over inventories to jack up prices is fascinating. There are several interesting take-aways.

First, the piece suggests that the impact on price is limited (7 percent, if their estimates are right), but worth a huge amount given the volumes involved. This is what I had always assumed about the extent to which this sort of speculation can affect the price of products. Speculation might add 20-30 cents to the price of gas, but it can’t explain why we are paying $4.00 a gallon rather than $1.50 a gallon.

Second, there is nothing unique to financial firms that allow them to speculate in this way. Yes, Goldman Sachs has lots of money, but so does Alcoa and many other non-financial companies. If a company can corner the market in major commodities then it indicates a failure first and foremost of anti-trust regulation.

Third, this should reinforce the argument for a new Glass-Steagall. The guarantees provided by the FDIC and Fed to commercial banks reflect their unique importance in maintaining the system of payments in the economy. There is no reason that banks should be able to exploit these guarantees to assist themselves in raising the money needed to corner the aluminum market. If Goldman wants to speculate in aluminum then it should not be a bank holding company. That one should be a no-brainer, except for the corruption of the political system.

Read More Leer más Join the discussion Participa en la discusión

The Washington Post has a great piece on how the American Medical Association is able to inflate doctors’ pay by hugely exaggerating the amount of time that Medicare assumes is required for a wide range of medical procedures. This increases Medicare reimbursement rates as well as the reimbursement rates paid by private insurers.

The Washington Post has a great piece on how the American Medical Association is able to inflate doctors’ pay by hugely exaggerating the amount of time that Medicare assumes is required for a wide range of medical procedures. This increases Medicare reimbursement rates as well as the reimbursement rates paid by private insurers.

Read More Leer más Join the discussion Participa en la discusión

The Post’s lead editorial on Detroit’s bankruptcy highlighted the role of pensions in the city’s finances. It warned readers that the problem of large unfunded pensions is common, telling readers:

“A new survey by scholars at Boston College finds that state and local pension plans have $3.8 trillion in unfunded liabilities, even assuming strong rates of return.”

Got that? $3.8 TRILLION in unfunded liabilities! Let’s see, I’ve $26.43 in my pockets, how does that compare? [See correction note — I was far too kind to the Post here.]

Okay, this is exactly the sort of irresponsible budget reporting that I wrote about yesterday. How many Post readers have any basis for assessing this $3.8 trillion unfunded liability figure?

It’s not hard to put this number in a context that would make it meaningful to readers. First, it is important to note that this estimate is over a 30-year period, the normal planning period for public pensions. It is also worth noting that the estimate is not based on an assumption of “strong rates of return.” Rather, the estimate assumes rates of return that are consistent with growth projections from the Congressional Budget Office and other forecasters.

If the Post wanted to make this number meaningful, the obvious point of reference would be projected GDP over this 30-year period. The discounted value of GDP over the next 30 years is roughly $447 trillion, which means that the estimated shortfall is a bit less than 0.9 percent of GDP. That’s hardly trivial, but not obviously a crushing burden either. Furthermore, many state and local governments are already contributing at rates that are consistent with filling this gap, meaning that no additional commitment of public funds will be needed to fill the shortfall, current levels of taxation are adequate.

The Post would have provided this information if the point was to inform readers. But that obviously was not the paper’s point. The Post’s point in this editorial was to scare readers to advance its agenda for cutting public pensions.

The Post’s lead editorial on Detroit’s bankruptcy highlighted the role of pensions in the city’s finances. It warned readers that the problem of large unfunded pensions is common, telling readers:

“A new survey by scholars at Boston College finds that state and local pension plans have $3.8 trillion in unfunded liabilities, even assuming strong rates of return.”

Got that? $3.8 TRILLION in unfunded liabilities! Let’s see, I’ve $26.43 in my pockets, how does that compare? [See correction note — I was far too kind to the Post here.]

Okay, this is exactly the sort of irresponsible budget reporting that I wrote about yesterday. How many Post readers have any basis for assessing this $3.8 trillion unfunded liability figure?

It’s not hard to put this number in a context that would make it meaningful to readers. First, it is important to note that this estimate is over a 30-year period, the normal planning period for public pensions. It is also worth noting that the estimate is not based on an assumption of “strong rates of return.” Rather, the estimate assumes rates of return that are consistent with growth projections from the Congressional Budget Office and other forecasters.

If the Post wanted to make this number meaningful, the obvious point of reference would be projected GDP over this 30-year period. The discounted value of GDP over the next 30 years is roughly $447 trillion, which means that the estimated shortfall is a bit less than 0.9 percent of GDP. That’s hardly trivial, but not obviously a crushing burden either. Furthermore, many state and local governments are already contributing at rates that are consistent with filling this gap, meaning that no additional commitment of public funds will be needed to fill the shortfall, current levels of taxation are adequate.

The Post would have provided this information if the point was to inform readers. But that obviously was not the paper’s point. The Post’s point in this editorial was to scare readers to advance its agenda for cutting public pensions.

Read More Leer más Join the discussion Participa en la discusión

Mary Williams Walsh seriously misrepresented the issues in discussing the debate over the discounts rates that public pension plans should use in assessing their liabilities. The goal of any formula for funding pensions should be to maintain a relatively even flow of funds into the pension in order to avoid sharp disruptions to government budgets.

The formula that pension funds typically use, which involves a smoothing process and discounts liabilities based on the expected rate of return of assets accomplished this purpose. An analysis based on the last 110 years of financial market fluctuations shows that this method rarely leads to sharp changes in the amount of required contributions. (It is important that the expected rate of return be adjusted with price to earnings ratios in the stock market. Many pension funds absurdly assumed that equities could provide a 10 percent rate of return in the 1990s stock bubble, even as price to earnings ratios crossed 30.)

By contrast, the discount formula clearly advocated in this piece would lead to sharp fluctuations in required contributions, assuming that pension funds continued to invest in stocks. This discount formula would require state and local governments to make large contributions to their pensions so that they could be fully funded using the risk free interest rate to assess liabilities, then they would be able to maintain minimal levels of payments since most of the contributions would come from the excess of the return on the fund’s assets over the assumed discount rate.

This would be similar to building up a large trust fund to pay for education in future years so that people could pay lower taxes two or three decades from now since the cost of the schools would be paid out of the trust fund. While that may be a nice thing to do, it would mean higher than necessary taxes on current workers. This is the predicted outcome of the discount method advocated in this piece assuming that pension investment patterns do not change.

Of course if the riskless discount rate was chosen as the basis for assessing these funds, then it is likely that pension managers would change their investment behavior and stop investing in stocks. There is no doubt that stock is a risky asset that provides far more volatile returns than bonds. If pensions are not allowed to factor in the increased return from stocks in assessing their financial state, there would be no reason for a pension fund manager to invest in them.

By investing in stock, pension fund managers would be taking the risk that a downturn will leave the pension plan appearing underfunded. This means that they would face the downside risk, but get none of the upside benefit. The likely outcome in this case would be that pensions would invest almost entirely in bonds or other low-yielding assets.

This would lead to an absurd situation in which collectively invested pension funds are held in safe assets, while individuals hold risky stock in their 401(k)s or other retirement accounts. These implications should have been clearly explained in any discussion of the choice of discount rates.

Mary Williams Walsh seriously misrepresented the issues in discussing the debate over the discounts rates that public pension plans should use in assessing their liabilities. The goal of any formula for funding pensions should be to maintain a relatively even flow of funds into the pension in order to avoid sharp disruptions to government budgets.

The formula that pension funds typically use, which involves a smoothing process and discounts liabilities based on the expected rate of return of assets accomplished this purpose. An analysis based on the last 110 years of financial market fluctuations shows that this method rarely leads to sharp changes in the amount of required contributions. (It is important that the expected rate of return be adjusted with price to earnings ratios in the stock market. Many pension funds absurdly assumed that equities could provide a 10 percent rate of return in the 1990s stock bubble, even as price to earnings ratios crossed 30.)

By contrast, the discount formula clearly advocated in this piece would lead to sharp fluctuations in required contributions, assuming that pension funds continued to invest in stocks. This discount formula would require state and local governments to make large contributions to their pensions so that they could be fully funded using the risk free interest rate to assess liabilities, then they would be able to maintain minimal levels of payments since most of the contributions would come from the excess of the return on the fund’s assets over the assumed discount rate.

This would be similar to building up a large trust fund to pay for education in future years so that people could pay lower taxes two or three decades from now since the cost of the schools would be paid out of the trust fund. While that may be a nice thing to do, it would mean higher than necessary taxes on current workers. This is the predicted outcome of the discount method advocated in this piece assuming that pension investment patterns do not change.

Of course if the riskless discount rate was chosen as the basis for assessing these funds, then it is likely that pension managers would change their investment behavior and stop investing in stocks. There is no doubt that stock is a risky asset that provides far more volatile returns than bonds. If pensions are not allowed to factor in the increased return from stocks in assessing their financial state, there would be no reason for a pension fund manager to invest in them.

By investing in stock, pension fund managers would be taking the risk that a downturn will leave the pension plan appearing underfunded. This means that they would face the downside risk, but get none of the upside benefit. The likely outcome in this case would be that pensions would invest almost entirely in bonds or other low-yielding assets.

This would lead to an absurd situation in which collectively invested pension funds are held in safe assets, while individuals hold risky stock in their 401(k)s or other retirement accounts. These implications should have been clearly explained in any discussion of the choice of discount rates.

Read More Leer más Join the discussion Participa en la discusión

Sorry folks, I committed the cardinal sin of accepting an assertion from a Washington Post editorial without carefully checking it myself. This morning the Post’s lead editorial used the occasion of Detroit’s bankruptcy to beat up on public sector pensions. The Post told readers:

“A new survey by scholars at Boston College finds that state and local pension plans have $3.8 trillion in unfunded liabilities, even assuming strong rates of return.”

I did actually check the study and saw the chart showing $3.8 trillion in liabilities. I then wrote up my blog post accordingly, pointing out how large $3.8 trillion was in the context of the next 30 years’ GDP, the planning horizon for pensions.

But I apparently forgot to think about this number for the necessary 10 seconds before writing. The $3.8 trillion figure should have struck me as way too large for an estimate for unfunded liabilities, and in fact it is. Here’s what the Boston College study said (page 2):

“In the aggregate, the actuarial value of assets amounted to $2.8 trillion and liabilities amounted to $3.8 trillion, producing a funded ratio of 73 percent.”

You see, the $3.8 trillion figure was an estimate of total liabilities, not unfunded liabilities. Since the pensions have $2.8 trillion in assets, their unfunded liabilities are just $1 trillion. Or, to put this in terms that may be understandable to Post readers, the unfunded liabilities are 0.22 percent of projected GDP over the next 30 years. And, as I noted in my earlier post, most state and local governments are already funding at levels that are consistent with making up this shortfall so there will no required tax increases or spending cuts to meet these future obligations.

So I apologize for accepting the Post’s $3.8 trillion figure for unfunded liabilities without looking more closely. Clearly the Post has an agenda to weaken or end public sector pensions and is perfectly happy to use bad numbers to accomplish this goal.

Addendum: The Post added a correction some time on Monday.

Sorry folks, I committed the cardinal sin of accepting an assertion from a Washington Post editorial without carefully checking it myself. This morning the Post’s lead editorial used the occasion of Detroit’s bankruptcy to beat up on public sector pensions. The Post told readers:

“A new survey by scholars at Boston College finds that state and local pension plans have $3.8 trillion in unfunded liabilities, even assuming strong rates of return.”

I did actually check the study and saw the chart showing $3.8 trillion in liabilities. I then wrote up my blog post accordingly, pointing out how large $3.8 trillion was in the context of the next 30 years’ GDP, the planning horizon for pensions.

But I apparently forgot to think about this number for the necessary 10 seconds before writing. The $3.8 trillion figure should have struck me as way too large for an estimate for unfunded liabilities, and in fact it is. Here’s what the Boston College study said (page 2):

“In the aggregate, the actuarial value of assets amounted to $2.8 trillion and liabilities amounted to $3.8 trillion, producing a funded ratio of 73 percent.”

You see, the $3.8 trillion figure was an estimate of total liabilities, not unfunded liabilities. Since the pensions have $2.8 trillion in assets, their unfunded liabilities are just $1 trillion. Or, to put this in terms that may be understandable to Post readers, the unfunded liabilities are 0.22 percent of projected GDP over the next 30 years. And, as I noted in my earlier post, most state and local governments are already funding at levels that are consistent with making up this shortfall so there will no required tax increases or spending cuts to meet these future obligations.

So I apologize for accepting the Post’s $3.8 trillion figure for unfunded liabilities without looking more closely. Clearly the Post has an agenda to weaken or end public sector pensions and is perfectly happy to use bad numbers to accomplish this goal.

Addendum: The Post added a correction some time on Monday.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

The NYT piece discussing Federal Reserve Board Chairman Ben Bernanke’s testimony before the House Financial Services Committee noted at one point the Fed’s assessment that growth is proceeding at a “modest to moderate pace.” It would have been worth noting that growth has been less than 2.0 percent for the last three years and is likely to remain below 2.0 percent at least for 2013.

This is below standard estimates of the economy’s potential growth rate, which is put at 2.2 percent to 2.4 percent. In other words, the economy is falling further behind its potential level of output at the current pace of growth. It would have been worth including the comparison to potential growth.

The NYT piece discussing Federal Reserve Board Chairman Ben Bernanke’s testimony before the House Financial Services Committee noted at one point the Fed’s assessment that growth is proceeding at a “modest to moderate pace.” It would have been worth noting that growth has been less than 2.0 percent for the last three years and is likely to remain below 2.0 percent at least for 2013.

This is below standard estimates of the economy’s potential growth rate, which is put at 2.2 percent to 2.4 percent. In other words, the economy is falling further behind its potential level of output at the current pace of growth. It would have been worth including the comparison to potential growth.

Read More Leer más Join the discussion Participa en la discusión

A New York Times article reported on the aging of Italy’s population and bizarrely implied that this was the cause of high youth unemployment. The piece tells readers:

“With older people in the Mediterranean living longer and longer lives — and with fertility rates low and youth unemployment soaring in Italy, Greece, Spain and Portugal — experts warn that Europe’s debt crisis is exacerbating a growing demographic crisis. In the coming years, they warn, there will be fewer workers paying into the social security system to support the pensions of older generations.”

This paragraph came immediately after a paragraph telling readers:

“Many of their children [of today’s elderly] have high school or university degrees and are now retired from public or private sector jobs. And their children, the ones born after 1970, generally have university degrees — and are struggling to find work.”

The claim that Italy is suffering from too few young to support the retired population and that the young cannot find jobs are directly contradictory. This is like telling us that Italy is suffering from a heat wave and sub-zero temperatures.

The problem of not enough young people is a problem of lack of supply — too few young people to provide the goods and services the country needs. This should manifest itself in a labor shortage. Companies are trying to get workers but cannot find them. There will be large numbers of jobs going unfilled with wages rising rapidly as employers bid against each other to hire the workers who are available.

By contrast the high unemployment rate, even for university grads, is evidence of lack of demand. In this situation there is no shortage of available workers, the problem in the economy is not enough demand. In this story, if Italy had a few more million centenarians, who were spending pensions without working, then it could create the demand needed to employ the young.

Of course the world is more complicated. Because of the failed policies of the European Central Bank, prices in southern Europe got out of line with prices in northern Europe. As a result, much of the demand created by the elderly in Italy goes to Germany rather than Italy. But this is a story of incompetent central bankers, not demographics.

A New York Times article reported on the aging of Italy’s population and bizarrely implied that this was the cause of high youth unemployment. The piece tells readers:

“With older people in the Mediterranean living longer and longer lives — and with fertility rates low and youth unemployment soaring in Italy, Greece, Spain and Portugal — experts warn that Europe’s debt crisis is exacerbating a growing demographic crisis. In the coming years, they warn, there will be fewer workers paying into the social security system to support the pensions of older generations.”

This paragraph came immediately after a paragraph telling readers:

“Many of their children [of today’s elderly] have high school or university degrees and are now retired from public or private sector jobs. And their children, the ones born after 1970, generally have university degrees — and are struggling to find work.”

The claim that Italy is suffering from too few young to support the retired population and that the young cannot find jobs are directly contradictory. This is like telling us that Italy is suffering from a heat wave and sub-zero temperatures.

The problem of not enough young people is a problem of lack of supply — too few young people to provide the goods and services the country needs. This should manifest itself in a labor shortage. Companies are trying to get workers but cannot find them. There will be large numbers of jobs going unfilled with wages rising rapidly as employers bid against each other to hire the workers who are available.

By contrast the high unemployment rate, even for university grads, is evidence of lack of demand. In this situation there is no shortage of available workers, the problem in the economy is not enough demand. In this story, if Italy had a few more million centenarians, who were spending pensions without working, then it could create the demand needed to employ the young.

Of course the world is more complicated. Because of the failed policies of the European Central Bank, prices in southern Europe got out of line with prices in northern Europe. As a result, much of the demand created by the elderly in Italy goes to Germany rather than Italy. But this is a story of incompetent central bankers, not demographics.

Read More Leer más Join the discussion Participa en la discusión

That minor detail was missing from Wonkblog’s discussion of the proposed E.U.-U.S. trade agreement and the Trans-Pacific Partnership. The piece begins by telling readers in the first sentence:

“Nailing down complicated international trade agreements, with a zillion different interests and moving parts, is no easy feat.”

It then adds that the Obama administration will be trying to do two deals at once and that it will have to contend with opposition in Congress.

Of course there is no reason the deals have to be complicated. If the trade deals focused on removing traditional trade barriers such as tariffs and quotas, there would not be “a zillion different interests and moving parts.” There would be some formulaic wording written into the agreement that specified the rate at which these restrictions would be pared back.

The reason there are a zillion moving parts is because the Obama administration went to the oil and gas industries to ask how they can use the trade agreement to get around environmental restrictions on drilling. It went to the food and agricultural industries to ask how they could get around food safety rules. It went to the pharmaceutical industry to ask it how it can use these deals to increase patent protections and jack up drug prices. It went to the entertainment industry and asked how it can use these deals to strengthen copyright enforcement and require Internet intermediaries to take responsibility (and incur expenses) to help enforce copyrights.

That is why these deals have a zillion moving parts instead of being simple agreements focused on reducing barriers to trade. It would have been helpful if Wonkblog had explained this fact to readers.

That minor detail was missing from Wonkblog’s discussion of the proposed E.U.-U.S. trade agreement and the Trans-Pacific Partnership. The piece begins by telling readers in the first sentence:

“Nailing down complicated international trade agreements, with a zillion different interests and moving parts, is no easy feat.”

It then adds that the Obama administration will be trying to do two deals at once and that it will have to contend with opposition in Congress.

Of course there is no reason the deals have to be complicated. If the trade deals focused on removing traditional trade barriers such as tariffs and quotas, there would not be “a zillion different interests and moving parts.” There would be some formulaic wording written into the agreement that specified the rate at which these restrictions would be pared back.

The reason there are a zillion moving parts is because the Obama administration went to the oil and gas industries to ask how they can use the trade agreement to get around environmental restrictions on drilling. It went to the food and agricultural industries to ask how they could get around food safety rules. It went to the pharmaceutical industry to ask it how it can use these deals to increase patent protections and jack up drug prices. It went to the entertainment industry and asked how it can use these deals to strengthen copyright enforcement and require Internet intermediaries to take responsibility (and incur expenses) to help enforce copyrights.

That is why these deals have a zillion moving parts instead of being simple agreements focused on reducing barriers to trade. It would have been helpful if Wonkblog had explained this fact to readers.

Read More Leer más Join the discussion Participa en la discusión

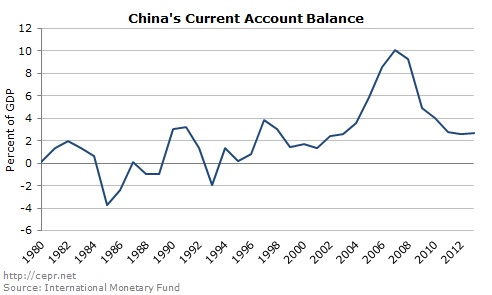

Wonkblog has an interesting interview with Patrick Chovanec, an economics professor at Tsinghua University’s School of Economics and Management in Beijing on China’s current economic problems. At one point Mr. Chovanec refers to:

“China’s growth model for the last 30 years, which has been a classic export-led growth model.”

Actually China’s growth over the last three decades has not been consistently export led, or at least not to the same degree as was the case in the 10 years leading up to the economic crisis.

As can be seen, until 1997, the year of the East Asian financial crisis, China had relatively balanced trade. It did run substantial surpluses in several years, but its trade surplus averaged just 0.3 percent of GDP from 1980 to 1996. By contrast, in the years from 1997 to 2008 the surplus averaged 4.5 percent of GDP. There clearly was a qualitatively different story of growth in the period from the East Asian financial crisis to the 2008 world economic crisis. It is misleading to imply that the Chinese economy had the same dynamic over this whole period.

Wonkblog has an interesting interview with Patrick Chovanec, an economics professor at Tsinghua University’s School of Economics and Management in Beijing on China’s current economic problems. At one point Mr. Chovanec refers to:

“China’s growth model for the last 30 years, which has been a classic export-led growth model.”

Actually China’s growth over the last three decades has not been consistently export led, or at least not to the same degree as was the case in the 10 years leading up to the economic crisis.

As can be seen, until 1997, the year of the East Asian financial crisis, China had relatively balanced trade. It did run substantial surpluses in several years, but its trade surplus averaged just 0.3 percent of GDP from 1980 to 1996. By contrast, in the years from 1997 to 2008 the surplus averaged 4.5 percent of GDP. There clearly was a qualitatively different story of growth in the period from the East Asian financial crisis to the 2008 world economic crisis. It is misleading to imply that the Chinese economy had the same dynamic over this whole period.

Read More Leer más Join the discussion Participa en la discusión