Okay, that is not exactly what he said, but if Chrystia Freeland’s account of Summers’ comments at Davos is to be believed Summers is badly misinformed about the state of the U.S. economy in 1993, when he was one of the top advisers in the Clinton administration. According to Freeland Summers said:

“In 1993, here’s what the situation was: Capital costs were really high, the trade deficit was really big, and if you looked at a graph of average wages and the productivity of American workers, those two graphs lay on top of each other. So, bringing down the deficit, reducing capital costs, raising investment, spurring productivity growth, was the right and natural central strategy for spurring growth. That was what Bob Rubin advised Bill Clinton, that was the advice Bill Clinton followed, and they were right.”

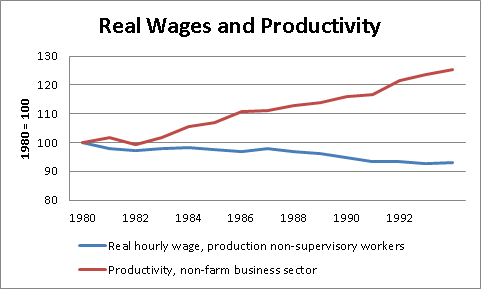

This is not what the data say. Here’s the story on real wages and productivity.

Source: Bureau of Labor Statistics.

There are some measurement issues that would reduce the gap somewhat, but anyone who could see these two as laying “on top of each other” needs some new glasses. The sharp divergence between productivity and wages began in the 1980s. It would be really scary if Larry Summers, Robert Rubin and the rest did not know this in 1993.

The other parts of Summers’ story are also wrong. The trade deficit was less than 1.0 percent of GDP in 1993. By comparison it was almost 4.0 percent of GDP when Clinton left office in 2000. The interest rate on ten-year Treasury bonds was 6.6 percent in January of 1993. Coupled with an inflation rate of around 3.0-3.5 percent, this gave a real interest rate in the neighborhood of 3.1-3.6 percent. This is perhaps a bit higher than desirable, but actually not much different than what we saw through most of the Clinton years.

In short, Summers is describing a history that does not exist. He either has a very poor memory or is just making things up.

Okay, that is not exactly what he said, but if Chrystia Freeland’s account of Summers’ comments at Davos is to be believed Summers is badly misinformed about the state of the U.S. economy in 1993, when he was one of the top advisers in the Clinton administration. According to Freeland Summers said:

“In 1993, here’s what the situation was: Capital costs were really high, the trade deficit was really big, and if you looked at a graph of average wages and the productivity of American workers, those two graphs lay on top of each other. So, bringing down the deficit, reducing capital costs, raising investment, spurring productivity growth, was the right and natural central strategy for spurring growth. That was what Bob Rubin advised Bill Clinton, that was the advice Bill Clinton followed, and they were right.”

This is not what the data say. Here’s the story on real wages and productivity.

Source: Bureau of Labor Statistics.

There are some measurement issues that would reduce the gap somewhat, but anyone who could see these two as laying “on top of each other” needs some new glasses. The sharp divergence between productivity and wages began in the 1980s. It would be really scary if Larry Summers, Robert Rubin and the rest did not know this in 1993.

The other parts of Summers’ story are also wrong. The trade deficit was less than 1.0 percent of GDP in 1993. By comparison it was almost 4.0 percent of GDP when Clinton left office in 2000. The interest rate on ten-year Treasury bonds was 6.6 percent in January of 1993. Coupled with an inflation rate of around 3.0-3.5 percent, this gave a real interest rate in the neighborhood of 3.1-3.6 percent. This is perhaps a bit higher than desirable, but actually not much different than what we saw through most of the Clinton years.

In short, Summers is describing a history that does not exist. He either has a very poor memory or is just making things up.

Read More Leer más Join the discussion Participa en la discusión

The NYT told us that Bank of America made $5.7 billion from “trading” last year. It then added:

“For the sake of clarity and consistency, it makes sense to relabel this type of revenue “market-making.” That’s because it mainly represents the gain Bank of America makes when it buys securities and sells them on to clients at a higher price.”

Really? The NYT knows that it just turned out that the price of assets rose by $5.7 billion between the time when Bank of America acquired them and when they passed them on to their clients? That sounds like some pretty good luck for BoA. After all, we would expect that roughly half of the time when BoA buys an asset for a client and when it actually passes the asset on to the client the price would fall. If the net in this story came to a plus $5.7 billion that would seem like a remarkable streak of good luck for BoA.

Let’s try an alternative hypothesis. Let’s imagine that BoA was trading on its account, deliberately trying to find assets that would rise in price. If BoA has well-informed people doing its buying and selling, then it might not be too hard to believe that it could clear $5.7 billion on this sort of trading.

Of course trading on its own account would likely violate the law. This is exactly what the Volcker Rule intended to prevent. So it would be very helpful if people thought that BoA made this $5.7 billion from market-making.

Addendum:

In response to a question below, let me clarify the meaning of “trading on its own account.” A market maker must be prepared to take positions on assets for at least short periods of time in order to service its clients. This means, for example, if a client wants to sell shares of stock or some other asset, then the market maker has to be prepared to buy and hold the asset until another buyer comes along. In principle, they will pay somewhat below the market price at the time to cover the risk that the price will fall before they can offload the stock and to cover the cost of their services.

By contrast, if a bank is trading on its account it is deliberately taking a directional bet on the asset. It is not always easy to distinguish between a trade where a bank is simply acting as a market maker and a trade where it is consciously making a bet that an asset will rise or fall in price. When the Volcker Rule is firmly in place the latter will not be legal for banks like Bank of America that have government guaranteed deposits.

It is entirely possible that BoA’s $5.7 billion in trading profits were entirely due to market making activities, however that does seem unlikely since it is a substantial amount of profit on what would be a relatively small portion of the bank’s revenue. In any case, rather than assuring readers that BoA is acting in a manner that would be in full compliance with the Volcker Rule, it would seem more appropriate to simply report its claims and let the readers make this assessment, unless the NYT has actually investigated the bank’s trading practices and feels comfortable making this assurance to readers.

The NYT told us that Bank of America made $5.7 billion from “trading” last year. It then added:

“For the sake of clarity and consistency, it makes sense to relabel this type of revenue “market-making.” That’s because it mainly represents the gain Bank of America makes when it buys securities and sells them on to clients at a higher price.”

Really? The NYT knows that it just turned out that the price of assets rose by $5.7 billion between the time when Bank of America acquired them and when they passed them on to their clients? That sounds like some pretty good luck for BoA. After all, we would expect that roughly half of the time when BoA buys an asset for a client and when it actually passes the asset on to the client the price would fall. If the net in this story came to a plus $5.7 billion that would seem like a remarkable streak of good luck for BoA.

Let’s try an alternative hypothesis. Let’s imagine that BoA was trading on its account, deliberately trying to find assets that would rise in price. If BoA has well-informed people doing its buying and selling, then it might not be too hard to believe that it could clear $5.7 billion on this sort of trading.

Of course trading on its own account would likely violate the law. This is exactly what the Volcker Rule intended to prevent. So it would be very helpful if people thought that BoA made this $5.7 billion from market-making.

Addendum:

In response to a question below, let me clarify the meaning of “trading on its own account.” A market maker must be prepared to take positions on assets for at least short periods of time in order to service its clients. This means, for example, if a client wants to sell shares of stock or some other asset, then the market maker has to be prepared to buy and hold the asset until another buyer comes along. In principle, they will pay somewhat below the market price at the time to cover the risk that the price will fall before they can offload the stock and to cover the cost of their services.

By contrast, if a bank is trading on its account it is deliberately taking a directional bet on the asset. It is not always easy to distinguish between a trade where a bank is simply acting as a market maker and a trade where it is consciously making a bet that an asset will rise or fall in price. When the Volcker Rule is firmly in place the latter will not be legal for banks like Bank of America that have government guaranteed deposits.

It is entirely possible that BoA’s $5.7 billion in trading profits were entirely due to market making activities, however that does seem unlikely since it is a substantial amount of profit on what would be a relatively small portion of the bank’s revenue. In any case, rather than assuring readers that BoA is acting in a manner that would be in full compliance with the Volcker Rule, it would seem more appropriate to simply report its claims and let the readers make this assessment, unless the NYT has actually investigated the bank’s trading practices and feels comfortable making this assurance to readers.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

Okay, I’m stealing from Paul Krugman today. Brooks’ column today points out that modest redistributional measures implemented by Obama don’t amount to a hill of beans next to the enormous upward redistribution going on in before-tax income. The restoration of Clinton era tax rates at best take away 2-3 years of growing inequality of before tax income.

Where Brooks is out to lunch is when he tells readers:

“On the one side, there is the meritocracy, which widens inequality.”

That one is more than a few million miles far of the mark. When Erskine Bowles earned $340k as a director of Morgan Stanley as it was pursuing practices that would have landed it in bankruptcy had it not been saved by a government bailout, was that due to meritocracy? Did all the CEOs who got tens of millions of dollars in compensation as they tanked their companies get their pay due to meritocracy? Is the reason that our doctors get twice as much as doctors in Western Europe meritocracy?

The list here is very long, yes it’s my book about Loser Liberalism, but you have to be pretty blind to realities in the United States today to think that the story of inequality is primarily about meritocracy — although it might be useful for some people to think this.

Okay, I’m stealing from Paul Krugman today. Brooks’ column today points out that modest redistributional measures implemented by Obama don’t amount to a hill of beans next to the enormous upward redistribution going on in before-tax income. The restoration of Clinton era tax rates at best take away 2-3 years of growing inequality of before tax income.

Where Brooks is out to lunch is when he tells readers:

“On the one side, there is the meritocracy, which widens inequality.”

That one is more than a few million miles far of the mark. When Erskine Bowles earned $340k as a director of Morgan Stanley as it was pursuing practices that would have landed it in bankruptcy had it not been saved by a government bailout, was that due to meritocracy? Did all the CEOs who got tens of millions of dollars in compensation as they tanked their companies get their pay due to meritocracy? Is the reason that our doctors get twice as much as doctors in Western Europe meritocracy?

The list here is very long, yes it’s my book about Loser Liberalism, but you have to be pretty blind to realities in the United States today to think that the story of inequality is primarily about meritocracy — although it might be useful for some people to think this.

Read More Leer más Join the discussion Participa en la discusión

A NYT article on the Republicans’ latest plans in upcoming budget debates told readers:

“Republicans have made clear that they are willing to let the government shut down at that time to force deep spending cuts or changes to Medicare and Social Security that would bring down deficits in the long run.”

The Republicans are interested in cutting these programs, that is how their plans would bring down deficits. While a “cut” can be termed a change, in the same way that a punch to a person’s head can be described as a “change” in their circumstances, this is not the way such actions would typically be described.

It is understandable that the Republicans would prefer to use euphemisms to describe their plans for these very popular programs. However newspapers are supposed to try to convey information to readers. It is not their job to try to advance the agenda of a political party.

A NYT article on the Republicans’ latest plans in upcoming budget debates told readers:

“Republicans have made clear that they are willing to let the government shut down at that time to force deep spending cuts or changes to Medicare and Social Security that would bring down deficits in the long run.”

The Republicans are interested in cutting these programs, that is how their plans would bring down deficits. While a “cut” can be termed a change, in the same way that a punch to a person’s head can be described as a “change” in their circumstances, this is not the way such actions would typically be described.

It is understandable that the Republicans would prefer to use euphemisms to describe their plans for these very popular programs. However newspapers are supposed to try to convey information to readers. It is not their job to try to advance the agenda of a political party.

Read More Leer más Join the discussion Participa en la discusión

I didn’t have a clue and I suspect that 99 percent of other NYT readers also didn’t have a clue. This raises the question of why did the NYT use this number, referring to the size of the income tax cuts being proposed by Kansas Governor Sam Brownback, without any context?

Kansas 2013 budget was $13.4 billion, making the proposed tax cut equal to 6.3 percent of last year’s budget. Most NYT readers would have a reasonably good sense of the meaning of 6.3 percent.

I didn’t have a clue and I suspect that 99 percent of other NYT readers also didn’t have a clue. This raises the question of why did the NYT use this number, referring to the size of the income tax cuts being proposed by Kansas Governor Sam Brownback, without any context?

Kansas 2013 budget was $13.4 billion, making the proposed tax cut equal to 6.3 percent of last year’s budget. Most NYT readers would have a reasonably good sense of the meaning of 6.3 percent.

Read More Leer más Join the discussion Participa en la discusión

Yes, we have a mismatch of jobs and skills. The problem is that it seems to be on the side of the managers who can’t seem to figure out how to get good help. An excellent review of Peter Cappelli’s new book by Trey Popp.

Yes, we have a mismatch of jobs and skills. The problem is that it seems to be on the side of the managers who can’t seem to figure out how to get good help. An excellent review of Peter Cappelli’s new book by Trey Popp.

Read More Leer más Join the discussion Participa en la discusión

Deficits throughout the euro zone were relatively modest prior to the economic collapse in 2008 according to data from the IMF. In fact, some euro zone countries, like Spain and Ireland, were even running budget surpluses. This didn’t stop Reuters from telling readers in the first line of an article picked up by the NYT:

“Public debt levels in the euro zone neared their projected peak last year after more than a decade of huge borrowing.”

This is seriously misleading since it implies that large deficits were a longstanding problem as opposed to an outgrowth of the economic crisis.

Deficits throughout the euro zone were relatively modest prior to the economic collapse in 2008 according to data from the IMF. In fact, some euro zone countries, like Spain and Ireland, were even running budget surpluses. This didn’t stop Reuters from telling readers in the first line of an article picked up by the NYT:

“Public debt levels in the euro zone neared their projected peak last year after more than a decade of huge borrowing.”

This is seriously misleading since it implies that large deficits were a longstanding problem as opposed to an outgrowth of the economic crisis.

Read More Leer más Join the discussion Participa en la discusión

There were numerous news stories and columns touting the liberal agenda that President Obama put forward in his second inaugural address yesterday (e.g. here and here). While the speech certainly hit on several issues that have historically been important to liberals, the failure to mention full employment was a major omission.

The fact that the economy is still more than 9 million jobs below its trend growth path implies enormous suffering. Not only are millions of people unnecessarily unemployed or underemployed, high levels of unemployment mean that most workers lack bargaining power. As a result they are unable to raise their wages and get their share of productivity growth. This means that income is likely to continue to be redistributed upward.

There are not easy political paths to full employment at this point. Government stimulus (i.e. larger deficits) is the most obvious path, but that seems out of the question in a context where deficit reduction is dominating the policy debate. If the dollar dropped, it would make U.S. goods more competitive, thereby increasing net exports, but Obama has made little commitment in this direction and the process would take time in any case.

The best prospect is probably increased use of worksharing. Germany has used worksharing to lower its unemployment rate by more than 2 percentage points below its pre-recession level, even though its growth has been no better than growth in the United States. Worksharing does enjoy bipartisan support in the United States and is an option in the unemployment insurance systems in 25 states, but the takeup rate has been extremely low. It’s possible that a major presidential push could substantially increase the use of worksharing.

Anyhow, it is striking that a speech that touched on many liberal themes did not make a commitment to full employment. This should have been noted in the coverage.

There were numerous news stories and columns touting the liberal agenda that President Obama put forward in his second inaugural address yesterday (e.g. here and here). While the speech certainly hit on several issues that have historically been important to liberals, the failure to mention full employment was a major omission.

The fact that the economy is still more than 9 million jobs below its trend growth path implies enormous suffering. Not only are millions of people unnecessarily unemployed or underemployed, high levels of unemployment mean that most workers lack bargaining power. As a result they are unable to raise their wages and get their share of productivity growth. This means that income is likely to continue to be redistributed upward.

There are not easy political paths to full employment at this point. Government stimulus (i.e. larger deficits) is the most obvious path, but that seems out of the question in a context where deficit reduction is dominating the policy debate. If the dollar dropped, it would make U.S. goods more competitive, thereby increasing net exports, but Obama has made little commitment in this direction and the process would take time in any case.

The best prospect is probably increased use of worksharing. Germany has used worksharing to lower its unemployment rate by more than 2 percentage points below its pre-recession level, even though its growth has been no better than growth in the United States. Worksharing does enjoy bipartisan support in the United States and is an option in the unemployment insurance systems in 25 states, but the takeup rate has been extremely low. It’s possible that a major presidential push could substantially increase the use of worksharing.

Anyhow, it is striking that a speech that touched on many liberal themes did not make a commitment to full employment. This should have been noted in the coverage.

Read More Leer más Join the discussion Participa en la discusión

Morning Edition’s top of the hour news segment (sorry, no link) told listeners that the Nikkei dropped in response to the Bank of Japan’s commitment to support stimulus. The Wall Street Journal said the opposite, pointing out that the bank’s asset purchase plans were quite modest. According to the WSJ, the decline in Japan’s stock market and rise in the yen was due to the concern that the bank was insufficiently committed to stimulus.

Morning Edition’s top of the hour news segment (sorry, no link) told listeners that the Nikkei dropped in response to the Bank of Japan’s commitment to support stimulus. The Wall Street Journal said the opposite, pointing out that the bank’s asset purchase plans were quite modest. According to the WSJ, the decline in Japan’s stock market and rise in the yen was due to the concern that the bank was insufficiently committed to stimulus.

Read More Leer más Join the discussion Participa en la discusión