Jeffrey Sachs has played a useful role in challenging the economic orthodoxy in many areas over the last three years. However, when he tries to tell us that the current downturn is structural not cyclical he is way over his head in the quicksand of the orthodoxy.

Let’s start with his simple bold assertion:

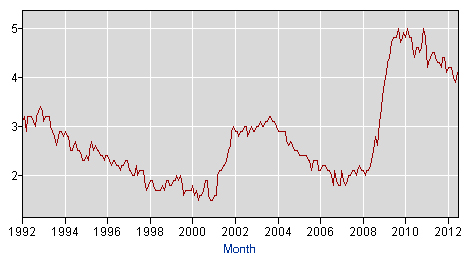

“Consider the new U.S. unemployment announcement. If you are a college graduate, there is no employment crisis. 72.7 percent of the college-educated population age-25 and over is working. The unemployment rate is 4.1 percent. Incomes are good.”

Umm, no, that’s not right. If we go back to 2007 we would see that the unemployment rate for college grads was 1.9 percent at its low that year, less than half of the current rate. It averaged 1.6 percent in 2000.

Unemployment Rate for College Grads, 25 years and Over

Source: Bureau of Labor Statistics.

Source: Bureau of Labor Statistics.

If the current unemployment in the U.S. economy were structural than we should expect to see lower than normal for these college grads whose labor is in short supply. Instead, we see that their unemployment rate is more than twice the pre-recession level and close two and half times its 2000 level.

We should also expect to see that real wages for college grads are rising rapidly. They aren’t. They have not even kept pace with inflation for the last dozen years.

In short, Sachs does not even have the beginning of an argument here. He’d better find some new data or give up his argument that the causes of unemployment are structural. His data indicate the opposite.

Jeffrey Sachs has played a useful role in challenging the economic orthodoxy in many areas over the last three years. However, when he tries to tell us that the current downturn is structural not cyclical he is way over his head in the quicksand of the orthodoxy.

Let’s start with his simple bold assertion:

“Consider the new U.S. unemployment announcement. If you are a college graduate, there is no employment crisis. 72.7 percent of the college-educated population age-25 and over is working. The unemployment rate is 4.1 percent. Incomes are good.”

Umm, no, that’s not right. If we go back to 2007 we would see that the unemployment rate for college grads was 1.9 percent at its low that year, less than half of the current rate. It averaged 1.6 percent in 2000.

Unemployment Rate for College Grads, 25 years and Over

Source: Bureau of Labor Statistics.

If the current unemployment in the U.S. economy were structural than we should expect to see lower than normal for these college grads whose labor is in short supply. Instead, we see that their unemployment rate is more than twice the pre-recession level and close two and half times its 2000 level.

We should also expect to see that real wages for college grads are rising rapidly. They aren’t. They have not even kept pace with inflation for the last dozen years.

In short, Sachs does not even have the beginning of an argument here. He’d better find some new data or give up his argument that the causes of unemployment are structural. His data indicate the opposite.

Read More Leer más Join the discussion Participa en la discusión

The NYT ran a lengthy story on the possibilities of manufacturing electronics in the United States. Near the end of the piece it discusses divisions in the Obama administration on measures to try to bring more manufacturing back to the United States.

On the one hand, it notes the view of Ron Bloom, who had been the president’s senior advisor on manufacturing policy, that the U.S. should take steps to push down the value of the dollar in order to make manufacturing in the United States more competitive. It then contrasts this view with that of Lawrence H. Summers, formerly the top economic adviser to Obama. The piece tells readers:

“along with many economists, Mr. Summers argued that an overly aggressive trade stance could hurt manufacturing — by, for instance, pushing up the price of imported steel used by carmakers — and over time, drive companies away. “

Actually, standard economic theory would argue that a lower valued dollar is exactly the mechanism through which the trade deficit should be brought down. In a system of floating exchange rates, the excess supply of currency on world markets from a deficit country like the United States is supposed to bring down the value of its currency. This makes its goods more competitive in world markets, reducing the size of its trade deficit.

The expected drop in the value of the currency is not taking place today with the dollar because a number of countries are buying up large amounts of dollars in order to prop up its value against their own currencies. By keeping the dollar over-valued they are able to sustain their trade surpluses with the United States.

It is worth noting that by definition, if the United States has a large trade deficit then the country has large negative national savings. This means that by supporting a policy that leads to a large trade deficit, Summers was arguing for either large budget deficits and/or large negative private savings, as we saw at the peak of the housing bubble. Perhaps Mr. Summers does not understand the implications of his position, but there is no logical way around it.

It is also worth noting that the over-valued dollar policy supported by Summers acts to redistribute income from workers who are exposed to international competition, like manufacturing workers, to workers who are largely protected from international competition, like doctors, lawyers and other highly educated professionals. In other words, it can be seen as one of the policies that redistributes money from the 99 percent to the one percent.

The NYT ran a lengthy story on the possibilities of manufacturing electronics in the United States. Near the end of the piece it discusses divisions in the Obama administration on measures to try to bring more manufacturing back to the United States.

On the one hand, it notes the view of Ron Bloom, who had been the president’s senior advisor on manufacturing policy, that the U.S. should take steps to push down the value of the dollar in order to make manufacturing in the United States more competitive. It then contrasts this view with that of Lawrence H. Summers, formerly the top economic adviser to Obama. The piece tells readers:

“along with many economists, Mr. Summers argued that an overly aggressive trade stance could hurt manufacturing — by, for instance, pushing up the price of imported steel used by carmakers — and over time, drive companies away. “

Actually, standard economic theory would argue that a lower valued dollar is exactly the mechanism through which the trade deficit should be brought down. In a system of floating exchange rates, the excess supply of currency on world markets from a deficit country like the United States is supposed to bring down the value of its currency. This makes its goods more competitive in world markets, reducing the size of its trade deficit.

The expected drop in the value of the currency is not taking place today with the dollar because a number of countries are buying up large amounts of dollars in order to prop up its value against their own currencies. By keeping the dollar over-valued they are able to sustain their trade surpluses with the United States.

It is worth noting that by definition, if the United States has a large trade deficit then the country has large negative national savings. This means that by supporting a policy that leads to a large trade deficit, Summers was arguing for either large budget deficits and/or large negative private savings, as we saw at the peak of the housing bubble. Perhaps Mr. Summers does not understand the implications of his position, but there is no logical way around it.

It is also worth noting that the over-valued dollar policy supported by Summers acts to redistribute income from workers who are exposed to international competition, like manufacturing workers, to workers who are largely protected from international competition, like doctors, lawyers and other highly educated professionals. In other words, it can be seen as one of the policies that redistributes money from the 99 percent to the one percent.

Read More Leer más Join the discussion Participa en la discusión

Catherine Rampell had an interesting discussion of the Fed’s likely course of action at its September meeting based on the July numbers. While the piece acknowledged the July jobs number from the establishment survey was somewhat better than expected, it concludes that the Fed is likely to move based on the weakness of the data from the household survey.

I’d have to disagree with that assessment. The household survey is far more erratic than the establishment survey. For example, it shows a jump of 422,000 jobs in May. Anyone remember that boom? Last June it reported a drop of 423,000. In August and September the household survey showed a combined gain of 657,000 jobs at a time when many news accounts were debating the likelihood of a double-dip recession.

It is easy to go back and find large one or even two month jumps or plunges in employment in the household survey that correspond to nothing that can be identified in the economy at the time. The Fed is surely aware of the household survey’s erratic pattern.

This means that when they sit down at their September meeting, the major news they will be considering on the labor market front will be the establishment survey. While the July data should warrant stronger steps to boost the economy (it will take 160 months of job growth at this pace to restore full employment), since they were not prepared to move before the July report, it is unlikely that a better than expected jobs number will prompt action.

Of course they will also have the August numbers by then.

Catherine Rampell had an interesting discussion of the Fed’s likely course of action at its September meeting based on the July numbers. While the piece acknowledged the July jobs number from the establishment survey was somewhat better than expected, it concludes that the Fed is likely to move based on the weakness of the data from the household survey.

I’d have to disagree with that assessment. The household survey is far more erratic than the establishment survey. For example, it shows a jump of 422,000 jobs in May. Anyone remember that boom? Last June it reported a drop of 423,000. In August and September the household survey showed a combined gain of 657,000 jobs at a time when many news accounts were debating the likelihood of a double-dip recession.

It is easy to go back and find large one or even two month jumps or plunges in employment in the household survey that correspond to nothing that can be identified in the economy at the time. The Fed is surely aware of the household survey’s erratic pattern.

This means that when they sit down at their September meeting, the major news they will be considering on the labor market front will be the establishment survey. While the July data should warrant stronger steps to boost the economy (it will take 160 months of job growth at this pace to restore full employment), since they were not prepared to move before the July report, it is unlikely that a better than expected jobs number will prompt action.

Of course they will also have the August numbers by then.

Read More Leer más Join the discussion Participa en la discusión

A piece that noted the slow pace of the recovery and compared it to other recessions never once mentioned the housing bubble. The fact that this recession was brought on by the collapse of a housing bubble, as opposed to the Fed raising interest rates to slow the economy, makes it qualitatively different from prior post-war recessions with the exception of the 2001 downturn that was brought on by the collapse of the stock bubble. It would have been worth making this point instead of turning the discussion into a he said/she said that concludes:

“‘The debate is unresolvable,’ said Douglas Holtz-Eakin, president of the American Action Forum, a center-right think tank, and the former director of the Congressional Budget Office. ‘We don’t have a lot of data points. We only have about a dozen recessions where we have a lot of data.'”

A piece that noted the slow pace of the recovery and compared it to other recessions never once mentioned the housing bubble. The fact that this recession was brought on by the collapse of a housing bubble, as opposed to the Fed raising interest rates to slow the economy, makes it qualitatively different from prior post-war recessions with the exception of the 2001 downturn that was brought on by the collapse of the stock bubble. It would have been worth making this point instead of turning the discussion into a he said/she said that concludes:

“‘The debate is unresolvable,’ said Douglas Holtz-Eakin, president of the American Action Forum, a center-right think tank, and the former director of the Congressional Budget Office. ‘We don’t have a lot of data points. We only have about a dozen recessions where we have a lot of data.'”

Read More Leer más Join the discussion Participa en la discusión

Binyamin Appelbaum has an interesting piece reminding readers of the importance of the seasonal adjustments in the job numbers that are released each month. It points out that July has the second largest positive seasonal adjustment, after January, of any month. (I don’t quite understand the chart, which seems to show positive seasonal adjustments for every month.) For example, last year the seasonal adjustment added 1.3 million jobs to the raw data, turning the seasonally adjusted number into a gain of 96,000 jobs, despite an unadjusted loss of 1.3 million jobs. Appelbaum’s point is that a small error in the size of the adjustment would have a huge impact on the jobs number reported for July.

The point is actually even more important than Appelbaum suggests. There are very large changes in employment month to month for seasonal factors that have nothing directly to do with the state of the economy. When these patterns change then the jobs numbers will give us a misleading picture of the state of the economy.

That is why the unusually warm winter weather gave an overly optimistic picture of the economy. Since this job growth was borrowed from the spring, the subsequent months gave us an overly pessimistic picture of the economy. Seasonal patterns can also change for reasons not directly related to weather. For example, stores now start holiday sales as early as October and the auto industry no longer shuts down all their factories in July for retooling.

Anyhow, Appelbaum is right to remind us about the importance of seasonal factors in the jobs numbers. We might not need a weatherman to know which way the wind blows, but we do need one to know how the economy is doing.

Binyamin Appelbaum has an interesting piece reminding readers of the importance of the seasonal adjustments in the job numbers that are released each month. It points out that July has the second largest positive seasonal adjustment, after January, of any month. (I don’t quite understand the chart, which seems to show positive seasonal adjustments for every month.) For example, last year the seasonal adjustment added 1.3 million jobs to the raw data, turning the seasonally adjusted number into a gain of 96,000 jobs, despite an unadjusted loss of 1.3 million jobs. Appelbaum’s point is that a small error in the size of the adjustment would have a huge impact on the jobs number reported for July.

The point is actually even more important than Appelbaum suggests. There are very large changes in employment month to month for seasonal factors that have nothing directly to do with the state of the economy. When these patterns change then the jobs numbers will give us a misleading picture of the state of the economy.

That is why the unusually warm winter weather gave an overly optimistic picture of the economy. Since this job growth was borrowed from the spring, the subsequent months gave us an overly pessimistic picture of the economy. Seasonal patterns can also change for reasons not directly related to weather. For example, stores now start holiday sales as early as October and the auto industry no longer shuts down all their factories in July for retooling.

Anyhow, Appelbaum is right to remind us about the importance of seasonal factors in the jobs numbers. We might not need a weatherman to know which way the wind blows, but we do need one to know how the economy is doing.

Read More Leer más Join the discussion Participa en la discusión

When it comes to tax plans, it’s all just so confusing. Or at least that’s what the NYT seems to be telling us.

The NYT ran an article that reports on a study by the Tax Policy Center that showed Governor Romney’s tax plan would lead to a large reduction in taxes for the wealthy, while raising taxes for everyone else. It then cites Romney’s claim that his tax plan is similar to the one developed by Morgan Stanley director Erskine Bowles and former Senator Alan Simpson, the co-chairs of President Obama’s deficit commission. The piece goes on to tell readers:

“The Simpson-Bowles plan called for reduced income tax rates, but it would have raised about $2 trillion more in tax revenues over 10 years, mostly from high-income taxpayers.”

Wow, this should really leave us scratching our heads. After all, if Romney’s plan is similar to the Bowles-Simpson plan, and the Bowles-Simpson plan would raise $2 trillion, mostly from high income taxpayers, then the Romney plan must also increase revenue from high income taxpayers. But, then the Tax Policy Center study would be wrong. What is a careful NYT reader to think?

The NYT could have resolved this seeming paradox by pointing out an important difference between the Romney plan and the Bowles-Simpson plan. Romney has explicitly said that he would not change any of the tax incentives for saving. This means that he has ruled out raising the tax rate on capital gains and dividends or curtailing some of the tax benefits for IRAs and 401(k)s. This makes his plan much more friendly to upper income taxpayers, who are the primary beneficiaries of these tax breaks.

Perhaps the NYT assumed that all its readers already knew about this difference between the Romney plan and the Bowles-Simpson plan, but it still would have been worth reminding them.

When it comes to tax plans, it’s all just so confusing. Or at least that’s what the NYT seems to be telling us.

The NYT ran an article that reports on a study by the Tax Policy Center that showed Governor Romney’s tax plan would lead to a large reduction in taxes for the wealthy, while raising taxes for everyone else. It then cites Romney’s claim that his tax plan is similar to the one developed by Morgan Stanley director Erskine Bowles and former Senator Alan Simpson, the co-chairs of President Obama’s deficit commission. The piece goes on to tell readers:

“The Simpson-Bowles plan called for reduced income tax rates, but it would have raised about $2 trillion more in tax revenues over 10 years, mostly from high-income taxpayers.”

Wow, this should really leave us scratching our heads. After all, if Romney’s plan is similar to the Bowles-Simpson plan, and the Bowles-Simpson plan would raise $2 trillion, mostly from high income taxpayers, then the Romney plan must also increase revenue from high income taxpayers. But, then the Tax Policy Center study would be wrong. What is a careful NYT reader to think?

The NYT could have resolved this seeming paradox by pointing out an important difference between the Romney plan and the Bowles-Simpson plan. Romney has explicitly said that he would not change any of the tax incentives for saving. This means that he has ruled out raising the tax rate on capital gains and dividends or curtailing some of the tax benefits for IRAs and 401(k)s. This makes his plan much more friendly to upper income taxpayers, who are the primary beneficiaries of these tax breaks.

Perhaps the NYT assumed that all its readers already knew about this difference between the Romney plan and the Bowles-Simpson plan, but it still would have been worth reminding them.

Read More Leer más Join the discussion Participa en la discusión

NPR told listeners that Standard & Poors downgrading of U.S. government debt caused the stock market plunge last summer:

“A year has passed since the debt ceiling debacle in Washington, D.C. The showdown cost the U.S. its AAA credit rating and sent the stock market and President Obama’s approval ratings plunging.”

Is that so? Let’s try a little logic 101 here. S&P downgraded U.S. government debt, meaning in principle that there was a greater risk that there would be a default on this debt. Let’s assume that the markets took S&P’s judgment seriously. What would we probably expect?

That’s right! We would expect the price of U.S. bonds to fall, this would cause the interest rate on U.S. debt to rise.

But, what actually happened was that U.S. bond prices soared and interest rates plummeted. This is 180 degrees at odds with the idea that the markets agreed with S&P’s assessment about the risk of holding U.S. bonds.

There is another factor that could explain both the jump in bond prices and the plunge in the stock market. This is the euro zone crisis, which became far more serious in early August as interest rates on Italian debt soared. That would cause investors to flee to U.S. bonds and make shareholders weary about the future of the economy.

That explanation logically fits the set of events that we saw in financial markets. Unfortunately it doesn’t fit the morality tale that NPR seems to want to give its listeners, so we apparently won’t get to hear it on the air.

NPR told listeners that Standard & Poors downgrading of U.S. government debt caused the stock market plunge last summer:

“A year has passed since the debt ceiling debacle in Washington, D.C. The showdown cost the U.S. its AAA credit rating and sent the stock market and President Obama’s approval ratings plunging.”

Is that so? Let’s try a little logic 101 here. S&P downgraded U.S. government debt, meaning in principle that there was a greater risk that there would be a default on this debt. Let’s assume that the markets took S&P’s judgment seriously. What would we probably expect?

That’s right! We would expect the price of U.S. bonds to fall, this would cause the interest rate on U.S. debt to rise.

But, what actually happened was that U.S. bond prices soared and interest rates plummeted. This is 180 degrees at odds with the idea that the markets agreed with S&P’s assessment about the risk of holding U.S. bonds.

There is another factor that could explain both the jump in bond prices and the plunge in the stock market. This is the euro zone crisis, which became far more serious in early August as interest rates on Italian debt soared. That would cause investors to flee to U.S. bonds and make shareholders weary about the future of the economy.

That explanation logically fits the set of events that we saw in financial markets. Unfortunately it doesn’t fit the morality tale that NPR seems to want to give its listeners, so we apparently won’t get to hear it on the air.

Read More Leer más Join the discussion Participa en la discusión

It used to be common for stories in the business press to make a big deal out of the weekly unemployment insurance claims numbers. And, it used to be common for me to beat up on them for exaggerating the importance of a weekly number that is highly erratic and subject to large revisions.

On the other hand, these numbers do provide information, especially when we see a trend over a number of weeks. That has been the case in the last five weeks as the average weekly claims number reached a recovery low.

For some reason the media no longer seems to be paying attention to these numbers. If they were, then they would not have been surprised by the 163,000 job growth reported for July.

It used to be common for stories in the business press to make a big deal out of the weekly unemployment insurance claims numbers. And, it used to be common for me to beat up on them for exaggerating the importance of a weekly number that is highly erratic and subject to large revisions.

On the other hand, these numbers do provide information, especially when we see a trend over a number of weeks. That has been the case in the last five weeks as the average weekly claims number reached a recovery low.

For some reason the media no longer seems to be paying attention to these numbers. If they were, then they would not have been surprised by the 163,000 job growth reported for July.

Read More Leer más Join the discussion Participa en la discusión

Read More Leer más Join the discussion Participa en la discusión

Patent monopolies raise the price of drugs from free market prices of $5-$10 per prescription to hundreds or even thousands of dollars per prescription. They have the same effect with medical devices.

The actual cost of using even the most advanced medical equipment is usually very low. After all, the machinery is already there, the only cost is a bit of electricity, the technicians’ time and possibly the time of a highly paid medical specialist. Even if we averaged the cost of manufacturing the machine over the number of uses, the cost is still likely to be relatively low. The big cost involved with medical equipment, as with prescription drugs, is the cost of the research that went into its development.

Using patent protection as a mechanism to recover these costs is incredibly inefficient, as Robert Samuelson inadvertently shows us in his column today. The piece is devoted to the results of a study that found that effective monitoring of the use of MRIs and greater cost-sharing with patients has led to a substantial reduction in the growth of their usage. As Samuelson reports, the study suggests that the main cost of this reduction in usage to patients may have been somewhat slower treatment of various aches and pains. It doesn’t have data on whether it might have had more serious effects in delaying the treatment of life-threatening conditions.

While it is certainly desirable to limit the unnecessary use of medical technology, it is worth noting that this problem comes about largely because of the patent monopoly provided for medical equipment. The article cited by Samuelson focuses on the fees paid to radiologists, one of the most highly paid medical specialties. However, even with their bloated pay of more than $500,000 a year, radiologists account for a small portion of the costs of an MRI. (Freeing up trade in radiological services could probably knock down this cost by 60-80 percent.)

With a typical radiologist able to perform more than 5000 MRIs a year, their fee would only account for around $100 of the cost of a scan. This means that most of the cost is going to pay for the overhead associated with buying the equipment, not the use of highly paid labor in the scan itself. Since this is a sunk cost (the machinery is already sitting there), we should want people to get scans anytime the expected benefit exceeds the $100 we have to pay the radiologist (until we get free trade), plus the pay to the other technicians and medical staff involved in providing the procedure.

Under this standard, we would probably want many of the people with aches and pains to be able to have access to the equipment. By contrast, devising and enforcing an effective system of controls like the one described in this column involves a considerable amount of time, much of it from highly paid professionals.

The alternative is to devise a mechanism for paying for research up front and letting the equipment be sold at its marginal cost of production. This would make MRI scans and the use of most other medical equipment cheap. It would also remove the incentive for providers to use this equipment in situations where it is not appropriate, since they would not be making the super-profits that patent monopolies allow.

There are alternatives to the current patent system. As Nobel winning economist Joe Stiglitz suggested with prescription drugs, we could have a patent buy-out system, where the government buys up useful patents and puts them in the public domain. Alternatively, the government could simply pay for research up front, perhaps doubling or tripling the $30 billion a year it now spends on research through the National Institutes of Health.

Patent monopolies raise the price of drugs from free market prices of $5-$10 per prescription to hundreds or even thousands of dollars per prescription. They have the same effect with medical devices.

The actual cost of using even the most advanced medical equipment is usually very low. After all, the machinery is already there, the only cost is a bit of electricity, the technicians’ time and possibly the time of a highly paid medical specialist. Even if we averaged the cost of manufacturing the machine over the number of uses, the cost is still likely to be relatively low. The big cost involved with medical equipment, as with prescription drugs, is the cost of the research that went into its development.

Using patent protection as a mechanism to recover these costs is incredibly inefficient, as Robert Samuelson inadvertently shows us in his column today. The piece is devoted to the results of a study that found that effective monitoring of the use of MRIs and greater cost-sharing with patients has led to a substantial reduction in the growth of their usage. As Samuelson reports, the study suggests that the main cost of this reduction in usage to patients may have been somewhat slower treatment of various aches and pains. It doesn’t have data on whether it might have had more serious effects in delaying the treatment of life-threatening conditions.

While it is certainly desirable to limit the unnecessary use of medical technology, it is worth noting that this problem comes about largely because of the patent monopoly provided for medical equipment. The article cited by Samuelson focuses on the fees paid to radiologists, one of the most highly paid medical specialties. However, even with their bloated pay of more than $500,000 a year, radiologists account for a small portion of the costs of an MRI. (Freeing up trade in radiological services could probably knock down this cost by 60-80 percent.)

With a typical radiologist able to perform more than 5000 MRIs a year, their fee would only account for around $100 of the cost of a scan. This means that most of the cost is going to pay for the overhead associated with buying the equipment, not the use of highly paid labor in the scan itself. Since this is a sunk cost (the machinery is already sitting there), we should want people to get scans anytime the expected benefit exceeds the $100 we have to pay the radiologist (until we get free trade), plus the pay to the other technicians and medical staff involved in providing the procedure.

Under this standard, we would probably want many of the people with aches and pains to be able to have access to the equipment. By contrast, devising and enforcing an effective system of controls like the one described in this column involves a considerable amount of time, much of it from highly paid professionals.

The alternative is to devise a mechanism for paying for research up front and letting the equipment be sold at its marginal cost of production. This would make MRI scans and the use of most other medical equipment cheap. It would also remove the incentive for providers to use this equipment in situations where it is not appropriate, since they would not be making the super-profits that patent monopolies allow.

There are alternatives to the current patent system. As Nobel winning economist Joe Stiglitz suggested with prescription drugs, we could have a patent buy-out system, where the government buys up useful patents and puts them in the public domain. Alternatively, the government could simply pay for research up front, perhaps doubling or tripling the $30 billion a year it now spends on research through the National Institutes of Health.

Read More Leer más Join the discussion Participa en la discusión