A NYT piece on shortages in Venezuela told readers:

“Venezuela was long one of the most prosperous countries in the region, with sophisticated manufacturing, vibrant agriculture and strong businesses, making it hard for many residents to accept such widespread scarcities.”

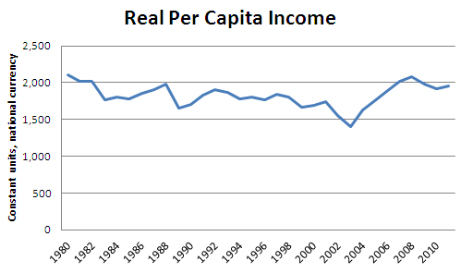

This may give the impression that Venezuela’s economy was strong before Hugo Chavez came to power in 1998. This is not true. According to the I.M.F., per capita income was actually 11.8 percent lower in 1998 than it had been 18 years earlier in 1980. Since Chavez came to power per capita income has risen by 4.9 percent. While this is hardly robust growth, since it was accompanied by greater equality in the distribution of income there can be little doubt that most Venezuelans have fared better under Chavez than under his predecessors.

Source: International Monetary Fund.

A NYT piece on shortages in Venezuela told readers:

“Venezuela was long one of the most prosperous countries in the region, with sophisticated manufacturing, vibrant agriculture and strong businesses, making it hard for many residents to accept such widespread scarcities.”

This may give the impression that Venezuela’s economy was strong before Hugo Chavez came to power in 1998. This is not true. According to the I.M.F., per capita income was actually 11.8 percent lower in 1998 than it had been 18 years earlier in 1980. Since Chavez came to power per capita income has risen by 4.9 percent. While this is hardly robust growth, since it was accompanied by greater equality in the distribution of income there can be little doubt that most Venezuelans have fared better under Chavez than under his predecessors.

Source: International Monetary Fund.

Read More Leer más Join the discussion Participa en la discusión

In its top of the hour news segment, Morning Edition told listeners that weekly unemployment claims fell last week (sorry, no link). This is sort of true, since claims were reported at 386,000 compared to 388,000 the prior week.

However the more important news here was that this was the second consecutive week in which claims were above 380,000 after hovering near 360,000 for the last two months. The number from two weeks ago was also revised upward with the release of yesterday’s data from 380,000 to 388,000. Almost every report in the last year has been revised upward the following week.

In this context, the latest release was not good news about the state of the economy.

In its top of the hour news segment, Morning Edition told listeners that weekly unemployment claims fell last week (sorry, no link). This is sort of true, since claims were reported at 386,000 compared to 388,000 the prior week.

However the more important news here was that this was the second consecutive week in which claims were above 380,000 after hovering near 360,000 for the last two months. The number from two weeks ago was also revised upward with the release of yesterday’s data from 380,000 to 388,000. Almost every report in the last year has been revised upward the following week.

In this context, the latest release was not good news about the state of the economy.

Read More Leer más Join the discussion Participa en la discusión

In search of good news in yesterday’s data releases, the Washington Post told readers that the median price for existing homes was 2.5 percent above its year ago level. While this is accurate, it is worth noting that the monthly price numbers are highly erratic.

The median sales price in March was more than 5 percent above the median price in February. This sort of month to month increase reflects the mix of homes sold and reporting error. It is not plausible that the price of a typical home actually rose 5 percent in a single month.

In search of good news in yesterday’s data releases, the Washington Post told readers that the median price for existing homes was 2.5 percent above its year ago level. While this is accurate, it is worth noting that the monthly price numbers are highly erratic.

The median sales price in March was more than 5 percent above the median price in February. This sort of month to month increase reflects the mix of homes sold and reporting error. It is not plausible that the price of a typical home actually rose 5 percent in a single month.

Read More Leer más Join the discussion Participa en la discusión

Politicians always like to give things to small businesses (many of which seem to be quite large). While the economics makes no sense, there is great politics to taxing workers to give even the most incompetent, greedy and corrupt people money, if they happen to own a business.

This is fairly obviously the logic of a Republican tax cut bill approved by the House which would give some small businesses a tax cut of 20 percent. While the bill was obviously a political gesture in an election year, since there was no chance that the Senate would approve it or that President Obama would sign it, it still may have been useful for the media to provide some explanation of what the bill would do.

The Post failed in this task, most importantly by not pointing out that the bill would only reduce taxes on businesses that are incorporated as separate entities and therefore pay the corporate income tax. This is important because the vast majority of small businesses are proprietorships or partnerships that do not pay the corporate income tax. These small businesses would not benefit from the Republican tax cut.

Politicians always like to give things to small businesses (many of which seem to be quite large). While the economics makes no sense, there is great politics to taxing workers to give even the most incompetent, greedy and corrupt people money, if they happen to own a business.

This is fairly obviously the logic of a Republican tax cut bill approved by the House which would give some small businesses a tax cut of 20 percent. While the bill was obviously a political gesture in an election year, since there was no chance that the Senate would approve it or that President Obama would sign it, it still may have been useful for the media to provide some explanation of what the bill would do.

The Post failed in this task, most importantly by not pointing out that the bill would only reduce taxes on businesses that are incorporated as separate entities and therefore pay the corporate income tax. This is important because the vast majority of small businesses are proprietorships or partnerships that do not pay the corporate income tax. These small businesses would not benefit from the Republican tax cut.

Read More Leer más Join the discussion Participa en la discusión

No one expects great economic analysis from the Post, especially on its opinion page, but the conclusion of David M. Smirk’s piece on the euro crisis must have left millions scratching their heads. The column told readers:

“Inflation, of course, is a highly regressive ‘tax’ on already stagnating wages and salaries. No wonder European governments are dropping like flies.”

Actually, most wages follow in step with inflation, although some workers do see declines in real wages when inflation rises. However, the biggest losers are creditors who are almost by definition wealthy, since people owe them money. If a creditor has lent out $100 million at 2 percent interest (e.g. buying a 10-year U.S. or German government bond) and the inflation rate rises from 2 percent to 4 percent, this creditor has lost an amount equal to 100 percent of his expected income or 2 percent of his wealth. This is a far larger loss than any worker could experience as a result of this increase in the inflation rate.

Also, most workers are debtors to some extent. They are likely to have mortgage debt, credit card debt, student loan debt and or car debt. A higher rate of inflation means that they can repay this debt in money that is worth less than the money they borrowed.

The other strange part of this assertion is that inflation is the reason “European governments are dropping like flies.” Of course the euro zone has very low inflation right now, even though many economists advocate a higher rate of inflation. It therefore makes no sense that inflation is causing governments to fall.

The piece also bizarrely includes Mexico on a list of countries that have experienced a boom following a bout of austerity. Mexico’s economy has had very weak growth, especially for a developing country, over the last two decades.

Finally, the piece includes the assertion:

“some of the periphery countries in the area of fiscal policy have, to put it bluntly, a history of cooking the books. They deserve the bitter medicine [austerity].”

This is an interesting moral position. The vast majority of workers, students and retirees in countries like Greece and Spain who are suffering from unemployment, higher tuition and pension cuts had no idea that their leaders were cooking the books.

By contrast, highly paid global financial policy strategists like Mr. Smirk might have been expected to recognize the asset bubbles that were driving the U.S. and European economies. They should have warned political leaders and the public at large that these economies were moving into dangerous terrain. If someone “deserves” to suffer we might think the people responsible for reckless policies would be the most obvious candidates, not ordinary workers and retirees.

Addendum:

For the folks who think that inflation leads to lower wages, here is a series showing the average real (inflation adjusted) hourly compensation (wages plus benefits) and the rate of inflation.

These series give the basic story, although they are not perfect for reasons that you do not want to hear about. If you can see a negative relationship (i.e. higher inflation leads to lower real wage growth) you have better eyesight than me.

No one expects great economic analysis from the Post, especially on its opinion page, but the conclusion of David M. Smirk’s piece on the euro crisis must have left millions scratching their heads. The column told readers:

“Inflation, of course, is a highly regressive ‘tax’ on already stagnating wages and salaries. No wonder European governments are dropping like flies.”

Actually, most wages follow in step with inflation, although some workers do see declines in real wages when inflation rises. However, the biggest losers are creditors who are almost by definition wealthy, since people owe them money. If a creditor has lent out $100 million at 2 percent interest (e.g. buying a 10-year U.S. or German government bond) and the inflation rate rises from 2 percent to 4 percent, this creditor has lost an amount equal to 100 percent of his expected income or 2 percent of his wealth. This is a far larger loss than any worker could experience as a result of this increase in the inflation rate.

Also, most workers are debtors to some extent. They are likely to have mortgage debt, credit card debt, student loan debt and or car debt. A higher rate of inflation means that they can repay this debt in money that is worth less than the money they borrowed.

The other strange part of this assertion is that inflation is the reason “European governments are dropping like flies.” Of course the euro zone has very low inflation right now, even though many economists advocate a higher rate of inflation. It therefore makes no sense that inflation is causing governments to fall.

The piece also bizarrely includes Mexico on a list of countries that have experienced a boom following a bout of austerity. Mexico’s economy has had very weak growth, especially for a developing country, over the last two decades.

Finally, the piece includes the assertion:

“some of the periphery countries in the area of fiscal policy have, to put it bluntly, a history of cooking the books. They deserve the bitter medicine [austerity].”

This is an interesting moral position. The vast majority of workers, students and retirees in countries like Greece and Spain who are suffering from unemployment, higher tuition and pension cuts had no idea that their leaders were cooking the books.

By contrast, highly paid global financial policy strategists like Mr. Smirk might have been expected to recognize the asset bubbles that were driving the U.S. and European economies. They should have warned political leaders and the public at large that these economies were moving into dangerous terrain. If someone “deserves” to suffer we might think the people responsible for reckless policies would be the most obvious candidates, not ordinary workers and retirees.

Addendum:

For the folks who think that inflation leads to lower wages, here is a series showing the average real (inflation adjusted) hourly compensation (wages plus benefits) and the rate of inflation.

These series give the basic story, although they are not perfect for reasons that you do not want to hear about. If you can see a negative relationship (i.e. higher inflation leads to lower real wage growth) you have better eyesight than me.

Read More Leer más Join the discussion Participa en la discusión

Readers will no doubt be asking if Japan can be saved from the Washington Post after reading Fred Hiatt’s column titled (in the print edition) “Can Japan Save Itself?” The column slams readers with large masses of inaccuracy that pass for conventional wisdom in Washington.

The fun begins in the second paragraph which tells readers:

“Much of Europe has spent itself into near-bankruptcy.”

This is of course not true. While Greece and Portugal did have serious pre-crisis deficit problems, Europe’s real problem was that the European Central Bank was building the Maginot Line against inflation and ignoring the massive asset bubbles and resulting imbalances that would eventually lead to the economic crisis in 2008. If we had seen the same budget paths not accompanied by the economic crisis, governments would have relatively little difficulty dealing with their fiscal problems.

The next sentence tells readers that:

“In Washington, Simpson-Bowles has come and gone.”

Actually, Simpson-Bowles never came. The co-chairs’ report did not get the votes needed to be approved as a report of the commission. As folks outside Washington say, the Moment of Truth is a lie.

Then we get Japan’s big crisis. Japan’s debt to GDP ratio is 230 percent of GDP. While this is indeed a huge number, its interest burden last year was less than 1.0 percent of its GDP. This is because its short-term interest rate is near zero and even its 10-year bond rate is just 1.0 percent.

Japan’s major problem is not its debt, but rather a lack of demand. It still has not found a way to make up the demand lost from the collapse of its stock and housing bubble in 1989-1990. The proposal to double the value added tax from 5 percent to 10 percent, which Hiatt applauds, would go in the wrong direction.

This tax increase would reduce demand, lowering growth and decreasing employment. If Hiatt knows a way that this tax increase could boost growth he would probably win a Nobel prize in economics if he shared it with readers.

The piece also referred to Japan negotiating a “free-trade” agreement with the United States. This is wrong. Japan is negotiating a “trade” agreement with the United States. It cannot accurately be called a “free-trade” agreement since it will almost certainly result in an increase in some forms of protectionism, most notably patent and copyright protection.

Readers will no doubt be asking if Japan can be saved from the Washington Post after reading Fred Hiatt’s column titled (in the print edition) “Can Japan Save Itself?” The column slams readers with large masses of inaccuracy that pass for conventional wisdom in Washington.

The fun begins in the second paragraph which tells readers:

“Much of Europe has spent itself into near-bankruptcy.”

This is of course not true. While Greece and Portugal did have serious pre-crisis deficit problems, Europe’s real problem was that the European Central Bank was building the Maginot Line against inflation and ignoring the massive asset bubbles and resulting imbalances that would eventually lead to the economic crisis in 2008. If we had seen the same budget paths not accompanied by the economic crisis, governments would have relatively little difficulty dealing with their fiscal problems.

The next sentence tells readers that:

“In Washington, Simpson-Bowles has come and gone.”

Actually, Simpson-Bowles never came. The co-chairs’ report did not get the votes needed to be approved as a report of the commission. As folks outside Washington say, the Moment of Truth is a lie.

Then we get Japan’s big crisis. Japan’s debt to GDP ratio is 230 percent of GDP. While this is indeed a huge number, its interest burden last year was less than 1.0 percent of its GDP. This is because its short-term interest rate is near zero and even its 10-year bond rate is just 1.0 percent.

Japan’s major problem is not its debt, but rather a lack of demand. It still has not found a way to make up the demand lost from the collapse of its stock and housing bubble in 1989-1990. The proposal to double the value added tax from 5 percent to 10 percent, which Hiatt applauds, would go in the wrong direction.

This tax increase would reduce demand, lowering growth and decreasing employment. If Hiatt knows a way that this tax increase could boost growth he would probably win a Nobel prize in economics if he shared it with readers.

The piece also referred to Japan negotiating a “free-trade” agreement with the United States. This is wrong. Japan is negotiating a “trade” agreement with the United States. It cannot accurately be called a “free-trade” agreement since it will almost certainly result in an increase in some forms of protectionism, most notably patent and copyright protection.

Read More Leer más Join the discussion Participa en la discusión

It seems that the NYT disapproves of the decision by Argentine president Cristina Kirchner to nationalize YPF, the country’s major oil company. At least that would be the impression of an article on reactions to this decision.

The article begins by telling us about a “fiery” speech in which Ms. Kirchner justified her decision to nationalize the company, which is currently owned by Repsol, a Spanish oil company. The piece concludes with a critical comment from Daniel Altman, who is identified as “an expert on Argentina’s economy at the Stern School of Business at New York University.” Altman is probably better known as a former New York Times business reporter, who did not specialize in coverage of Latin America.

In between the article gives us the views of many people who do not approve of the decision, although the article does point out that the company was just privatized back in the 90s and also that most other Latin American countries with substantial energy resources have a state owned oil company.

The article includes a bizarre paragraph telling readers:

“Yet in Brazil, where Petrobras’s achievement of energy independence and huge offshore oil discoveries have made it a model for oil companies in other developing nations, the YPF expropriation served as an opportunity to draw important contrasts with the situation in Argentina.

“As recently as 2000, Brazil still relied on oil imports from Argentina to meet energy needs, buying about 74,000 barrels of a day from its neighbor.

“Now the tables are turned. Petrobras, through its acquisition of Perez Companc, an independent Argentine oil company, has aggressively expanded in Argentina to the point where concerns have emerged here as to Petrobras’s exposure if Mrs. Kirchner opts to expand her nationalizations.”

It is not clear what “important contrasts” readers are expected to draw from this comparison. The piece seems to be describing the operations of a highly successful state-owned oil company which appears to be gaining ground at the expense of the privately-owned company in Argentina. This would be exactly the sort of argument that someone would make to justify the nationalization of YPF, although it is not clear if this is the conclusion the reader is expected to reach.

The reality is that there are examples of successful state-run companies, as this article shows. There are also many examples of poorly run government enterprises, just as there are many examples of poorly run private companies.

Whether or not Argentina will be able to improve the operation of YPF if it carries through the nationalization of the company remains to be seen. While there is evidence that might shed insight on this question, the article does not present any.

It seems that the NYT disapproves of the decision by Argentine president Cristina Kirchner to nationalize YPF, the country’s major oil company. At least that would be the impression of an article on reactions to this decision.

The article begins by telling us about a “fiery” speech in which Ms. Kirchner justified her decision to nationalize the company, which is currently owned by Repsol, a Spanish oil company. The piece concludes with a critical comment from Daniel Altman, who is identified as “an expert on Argentina’s economy at the Stern School of Business at New York University.” Altman is probably better known as a former New York Times business reporter, who did not specialize in coverage of Latin America.

In between the article gives us the views of many people who do not approve of the decision, although the article does point out that the company was just privatized back in the 90s and also that most other Latin American countries with substantial energy resources have a state owned oil company.

The article includes a bizarre paragraph telling readers:

“Yet in Brazil, where Petrobras’s achievement of energy independence and huge offshore oil discoveries have made it a model for oil companies in other developing nations, the YPF expropriation served as an opportunity to draw important contrasts with the situation in Argentina.

“As recently as 2000, Brazil still relied on oil imports from Argentina to meet energy needs, buying about 74,000 barrels of a day from its neighbor.

“Now the tables are turned. Petrobras, through its acquisition of Perez Companc, an independent Argentine oil company, has aggressively expanded in Argentina to the point where concerns have emerged here as to Petrobras’s exposure if Mrs. Kirchner opts to expand her nationalizations.”

It is not clear what “important contrasts” readers are expected to draw from this comparison. The piece seems to be describing the operations of a highly successful state-owned oil company which appears to be gaining ground at the expense of the privately-owned company in Argentina. This would be exactly the sort of argument that someone would make to justify the nationalization of YPF, although it is not clear if this is the conclusion the reader is expected to reach.

The reality is that there are examples of successful state-run companies, as this article shows. There are also many examples of poorly run government enterprises, just as there are many examples of poorly run private companies.

Whether or not Argentina will be able to improve the operation of YPF if it carries through the nationalization of the company remains to be seen. While there is evidence that might shed insight on this question, the article does not present any.

Read More Leer más Join the discussion Participa en la discusión

Remarkably this fact did not appear in a Washington Post article discussing U.S. trade with China, which did find room to tell readers that:

“But U.S. exports to China, whose growing affluence has increased the appetite for American goods, are now reaching record levels.“

While it is true that exports to China have reached a record high, this is true of imports as well, if we compare the same months of 2012 with the corresponding months of 2011. (In other words, we are controlling for seasonal effects.) The failure to note the record level of imports is especially surprising since our imports from China matter much more than out exports to China.

We are importing goods and services from China at the rate of more than $400 billion a year, whereas our exports are just a bit over $100 billion a year. This means that imports have close to four times the impact in reducing growth and employment as exports have in the opposite direction.

In discussing the issue of the relative value of the dollar and the Chinese currency it would have been useful to point out that important interests in the United States do not want to see China increase the value of the yuan. For example, Walmart has devoted considerable resources to developing a low-cost supply chain in China and other developing countries. This gives it an enormous advantage over its competitors.

Walmart is not anxious to have this advantage eroded by an increase in the value of the yuan relative to the dollar. The same is true of many companies that have established manufacturing operations in China for the purpose of exporting goods back to the United States and other countries.

This means that the debate over the relative value of the yuan and the dollar is not simply a debate between China and the United States. It is also a debate that pits different groups in the United States against each other.

Remarkably this fact did not appear in a Washington Post article discussing U.S. trade with China, which did find room to tell readers that:

“But U.S. exports to China, whose growing affluence has increased the appetite for American goods, are now reaching record levels.“

While it is true that exports to China have reached a record high, this is true of imports as well, if we compare the same months of 2012 with the corresponding months of 2011. (In other words, we are controlling for seasonal effects.) The failure to note the record level of imports is especially surprising since our imports from China matter much more than out exports to China.

We are importing goods and services from China at the rate of more than $400 billion a year, whereas our exports are just a bit over $100 billion a year. This means that imports have close to four times the impact in reducing growth and employment as exports have in the opposite direction.

In discussing the issue of the relative value of the dollar and the Chinese currency it would have been useful to point out that important interests in the United States do not want to see China increase the value of the yuan. For example, Walmart has devoted considerable resources to developing a low-cost supply chain in China and other developing countries. This gives it an enormous advantage over its competitors.

Walmart is not anxious to have this advantage eroded by an increase in the value of the yuan relative to the dollar. The same is true of many companies that have established manufacturing operations in China for the purpose of exporting goods back to the United States and other countries.

This means that the debate over the relative value of the yuan and the dollar is not simply a debate between China and the United States. It is also a debate that pits different groups in the United States against each other.

Read More Leer más Join the discussion Participa en la discusión

I would make fun of the part of this Thomas Friedman column that calls for cutting entitlements to put the budget on a sustainable footing (the problem is not “entitlements,” the problem is a broken health care system that raises the cost of public sector health care programs like Medicare and Medicaid), but I don’t believe this piece is genuine. Yesterday, Atrios proclaimed Thomas Friedman the “Wanker of the Decade,” referring to the first decade of his blog’s existence.

I suspect some sort of side arrangement. Friedman is clearly trying to publicize this designation by writing exactly the sort of inane centrist, above-the-political-fray column that earned him this award. He can’t fool me.

I would make fun of the part of this Thomas Friedman column that calls for cutting entitlements to put the budget on a sustainable footing (the problem is not “entitlements,” the problem is a broken health care system that raises the cost of public sector health care programs like Medicare and Medicaid), but I don’t believe this piece is genuine. Yesterday, Atrios proclaimed Thomas Friedman the “Wanker of the Decade,” referring to the first decade of his blog’s existence.

I suspect some sort of side arrangement. Friedman is clearly trying to publicize this designation by writing exactly the sort of inane centrist, above-the-political-fray column that earned him this award. He can’t fool me.

Read More Leer más Join the discussion Participa en la discusión

The Federal Reserve Board’s data on industrial production are often badly misinterpreted. The error occurs for two reasons. First, there are often large revisions to the monthly data and second, the aggregate index is often moved by large changes in mining or utility output.

The data for March released yesterday gave us examples of both. Therefore the NYT missed the story when it gave us the ominous news that:

“A Federal Reserve report showed American industrial output was flat for a second consecutive month in March, held back by a 0.2 percent drop in manufacturing.”

While the manufacturing index did show a 0.2 percent decline in March, its February reading was revised up by 0.5 percent. Therefore the March reading stood 0.3 percent from the advanced report for February and 0.6 percent above the February level. The reason that the industrial production index as a whole was flat over this period was a decline in mining output of approximately 3.8 percent.

The Federal Reserve Board’s data on industrial production are often badly misinterpreted. The error occurs for two reasons. First, there are often large revisions to the monthly data and second, the aggregate index is often moved by large changes in mining or utility output.

The data for March released yesterday gave us examples of both. Therefore the NYT missed the story when it gave us the ominous news that:

“A Federal Reserve report showed American industrial output was flat for a second consecutive month in March, held back by a 0.2 percent drop in manufacturing.”

While the manufacturing index did show a 0.2 percent decline in March, its February reading was revised up by 0.5 percent. Therefore the March reading stood 0.3 percent from the advanced report for February and 0.6 percent above the February level. The reason that the industrial production index as a whole was flat over this period was a decline in mining output of approximately 3.8 percent.

Read More Leer más Join the discussion Participa en la discusión