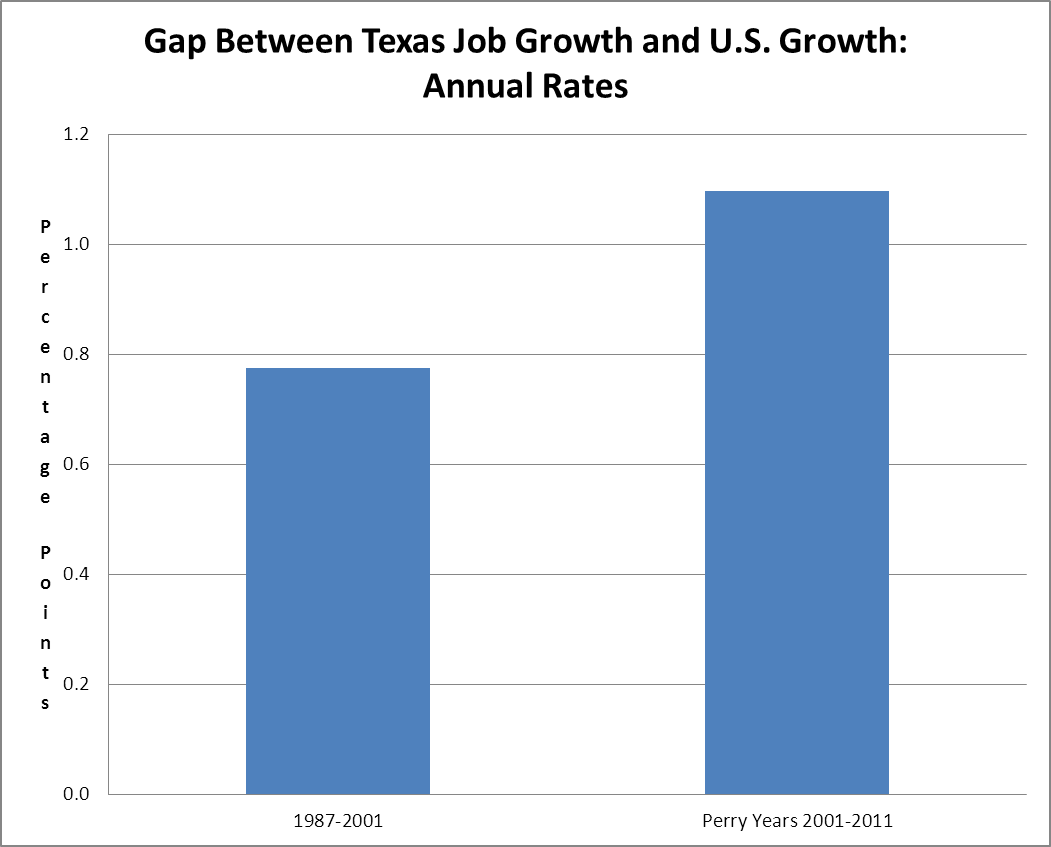

Sorry, folks I made a very bad mistake on this one. (Lesson: always double-check your commands in an Excel spreadsheet.) It turns out that Texas maintained and actually increased the gap between its rate of job growth and the rest of the country during the Perry years.

Over the years from 1987 to 2001, annual job growth in Texas averaged 2.8 percent. This is 0.8 percentage points higher than the growth rate for the economy as a whole. In the ten years since Governor Perry took office job growth has averaged just over 1.0 percent annually, during a period in which employment in the country as a whole actually shrank slightly. This makes the gap in the Perry years just under 1.1 percent. This means that, at least by the measure of job growth, Perry does have something to show in Texas.

(If you’re looking for me, I’m the guy wearing a paper bag over his head. Thanks to Sam123 for prompting me to recheck my numbers.)

Source: Bureau of Labor Statistics and author’s calculations.

Sorry, folks I made a very bad mistake on this one. (Lesson: always double-check your commands in an Excel spreadsheet.) It turns out that Texas maintained and actually increased the gap between its rate of job growth and the rest of the country during the Perry years.

Over the years from 1987 to 2001, annual job growth in Texas averaged 2.8 percent. This is 0.8 percentage points higher than the growth rate for the economy as a whole. In the ten years since Governor Perry took office job growth has averaged just over 1.0 percent annually, during a period in which employment in the country as a whole actually shrank slightly. This makes the gap in the Perry years just under 1.1 percent. This means that, at least by the measure of job growth, Perry does have something to show in Texas.

(If you’re looking for me, I’m the guy wearing a paper bag over his head. Thanks to Sam123 for prompting me to recheck my numbers.)

Source: Bureau of Labor Statistics and author’s calculations.

Read More Leer más Join the discussion Participa en la discusión

The NYT had a piece on the decision of four European countries to ban short selling. One of the rationales was that traders were spreading negative rumors about banks and profiting from them by shorting their stocks. Insofar as this is happening, this is a form of market manipulation which is a violation of security laws everywhere.

In principle, regulators should be able to track down and punish manipulators, however as a practical matter manipulation will often be difficult to detect. It is possible that outlawing short sales for a period of time can prevent manipulation, but the real issue is manipulation not short sales. Manipulation also takes place on the upside (e.g. rumors of exaggerated corporate profits) and is every bit as harmful to the proper working of the market and the economy.

The NYT had a piece on the decision of four European countries to ban short selling. One of the rationales was that traders were spreading negative rumors about banks and profiting from them by shorting their stocks. Insofar as this is happening, this is a form of market manipulation which is a violation of security laws everywhere.

In principle, regulators should be able to track down and punish manipulators, however as a practical matter manipulation will often be difficult to detect. It is possible that outlawing short sales for a period of time can prevent manipulation, but the real issue is manipulation not short sales. Manipulation also takes place on the upside (e.g. rumors of exaggerated corporate profits) and is every bit as harmful to the proper working of the market and the economy.

Read More Leer más Join the discussion Participa en la discusión

In the list of people most responsible for the economy’s wreckage, Robert Rubin is the only person who can rival Alan Greenspan for the top spot. As Treasury Secretary he pushed the over-valued dollar policy which led to the massive U.S. trade deficits.

These trade deficits are the fundamental imbalance in the U.S. and world economy. A trade deficit implies that either or both the government or private sector has negative savings. In other words, because we have a large trade deficit we must have a budget deficit or the sort of asset bubble-driven consumption boom that we had during the stock and housing bubbles.

Rubin also was a big proponent of removing government restrictions on the financial system. He helped to push through the repeal of Glass-Steagall. He also nixed Brooksley Born’s efforts to regulate derivatives like credit default swaps.

After his years in the Clinton administration he took a top position at Citigroup where he earned over $100 million. When he left the bank in 2008 it was on government provided life support. It had been at the center of the subprime crisis, securitizing hundreds of billions of dollars of subprime mortgages.

Presenting Rubin as just a wise man who used to be Treasury Secretary, as this NYT article does, is like presenting the Unabomber as simply a man who lived in a small cabin in Montana.

In the list of people most responsible for the economy’s wreckage, Robert Rubin is the only person who can rival Alan Greenspan for the top spot. As Treasury Secretary he pushed the over-valued dollar policy which led to the massive U.S. trade deficits.

These trade deficits are the fundamental imbalance in the U.S. and world economy. A trade deficit implies that either or both the government or private sector has negative savings. In other words, because we have a large trade deficit we must have a budget deficit or the sort of asset bubble-driven consumption boom that we had during the stock and housing bubbles.

Rubin also was a big proponent of removing government restrictions on the financial system. He helped to push through the repeal of Glass-Steagall. He also nixed Brooksley Born’s efforts to regulate derivatives like credit default swaps.

After his years in the Clinton administration he took a top position at Citigroup where he earned over $100 million. When he left the bank in 2008 it was on government provided life support. It had been at the center of the subprime crisis, securitizing hundreds of billions of dollars of subprime mortgages.

Presenting Rubin as just a wise man who used to be Treasury Secretary, as this NYT article does, is like presenting the Unabomber as simply a man who lived in a small cabin in Montana.

Read More Leer más Join the discussion Participa en la discusión

The Post seems to think that this may be the case. In reference to a provision of the Dodd-Frank financial reform bill that requires companies to publish the ratio of top executive pay to the pay of an ordinary worker it reported that “businesses have argued that this proposal would be costly and impractical to implement.”

This would only be true if businesses had no clue about either how much they pay their top executives or their ordinary workers. While it certainly seems to be the case that the top management of many corporations is not very competent, it is difficult that so many people earning 7 and 8 figure salaries could be that incompetent.

The Post seems to think that this may be the case. In reference to a provision of the Dodd-Frank financial reform bill that requires companies to publish the ratio of top executive pay to the pay of an ordinary worker it reported that “businesses have argued that this proposal would be costly and impractical to implement.”

This would only be true if businesses had no clue about either how much they pay their top executives or their ordinary workers. While it certainly seems to be the case that the top management of many corporations is not very competent, it is difficult that so many people earning 7 and 8 figure salaries could be that incompetent.

Read More Leer más Join the discussion Participa en la discusión

The folks at Morning Edition may not know that this is what they said, but in fact, this is exactly what a Planet Money segment on the dollar’s status as a reserve currency implied. The segment told listeners that it was a good thing that foreigners demanded large amounts of dollars to use and hold as a reserve currency.

If foreigners increase their holdings of dollars then this means that the United States has a trade deficit. This is a logical implication of foreigners’ efforts to acquire more dollars. In order to get more dollars, they have to sell more to the United States than they buy from the United States. There is no way around this.

If the United States has a trade deficit then it means that the country as a whole is a net borrower. That means that the combination of private and public savings must be negative. Again, this is an accounting identity, it must be true, just like 2+2 will always be equal to 4.

Generally private savings are roughly equal to private investment. The main exception is when asset bubbles like the stock market bubble or the housing bubble lead to a consumption boom and thereby depress private saving. (The housing bubble did also lead to a boom in construction, which as a component of investment allowed private investment to exceed savings, until the bubble burst.)

If the country has a trade deficit and private saving is equal to private investment, then the country must have a budget deficit. This means that in general circumstances, Morning Edition was telling us that budget deficits are good, since it told us that we should be happy that the dollar is the world’s reserve currency.

There was another important aspect to this issue that the piece failed to mention. Even if the dollar is used as a reserve currency the amount that a country needs to support a given level of trade can vary enormously. The amount of reserves that developing countries hold soared in the wake of the East Asian financial crisis. This is usually attributed to the fact that the terms of the bailout imposed by the IMF on the countries of the region were viewed as being so harsh that developing countries wanted to make sure that they would never be put in the same situation. This meant accumulating massive amounts of reserves (i.e. U.S. dollars) as an insurance policy.

This was the origin of the massive trade deficits that the United States has been running in recent years. It would have been useful to make this point in this segment.

The folks at Morning Edition may not know that this is what they said, but in fact, this is exactly what a Planet Money segment on the dollar’s status as a reserve currency implied. The segment told listeners that it was a good thing that foreigners demanded large amounts of dollars to use and hold as a reserve currency.

If foreigners increase their holdings of dollars then this means that the United States has a trade deficit. This is a logical implication of foreigners’ efforts to acquire more dollars. In order to get more dollars, they have to sell more to the United States than they buy from the United States. There is no way around this.

If the United States has a trade deficit then it means that the country as a whole is a net borrower. That means that the combination of private and public savings must be negative. Again, this is an accounting identity, it must be true, just like 2+2 will always be equal to 4.

Generally private savings are roughly equal to private investment. The main exception is when asset bubbles like the stock market bubble or the housing bubble lead to a consumption boom and thereby depress private saving. (The housing bubble did also lead to a boom in construction, which as a component of investment allowed private investment to exceed savings, until the bubble burst.)

If the country has a trade deficit and private saving is equal to private investment, then the country must have a budget deficit. This means that in general circumstances, Morning Edition was telling us that budget deficits are good, since it told us that we should be happy that the dollar is the world’s reserve currency.

There was another important aspect to this issue that the piece failed to mention. Even if the dollar is used as a reserve currency the amount that a country needs to support a given level of trade can vary enormously. The amount of reserves that developing countries hold soared in the wake of the East Asian financial crisis. This is usually attributed to the fact that the terms of the bailout imposed by the IMF on the countries of the region were viewed as being so harsh that developing countries wanted to make sure that they would never be put in the same situation. This meant accumulating massive amounts of reserves (i.e. U.S. dollars) as an insurance policy.

This was the origin of the massive trade deficits that the United States has been running in recent years. It would have been useful to make this point in this segment.

Read More Leer más Join the discussion Participa en la discusión

The WSJ has a nice piece that looks at the track record of the rating agencies in predicting defaults on government debt. It ain’t pretty.

The WSJ has a nice piece that looks at the track record of the rating agencies in predicting defaults on government debt. It ain’t pretty.

Read More Leer más Join the discussion Participa en la discusión

The NYT decided to have a special dialogue around a letter to the editor that called on President Obama to take “decisive action” on the economy. Remarkably, only one item on the list of decisive actions, investing in infrastructure, would have any positive impact on jobs and even this would be limited. While investing in infrastructure is a very good idea, there are not very many people who can be usefully employed on infrastructure projects in the next two years.

It takes time to plan a project and many projects, like building high speed rail, are only going to be built over many years. This means that even the most aggressive infrastructure program will only have a limited impact on jobs in the rest of 2011, 2012, and even 2013. If we want to see substantial reductions in unemployment over the next two years we will need more decisive action than this.

The rest of the items in the letter all involve reducing the deficit. While some of the proposals are very reasonable, like ending the war in Afghanistan and raising taxes on the wealthy, these will certainly not help create jobs. The list also contains two profoundly silly proposals, means-testing Social Security and raising the age of Medicare eligibility to 67.

The idea of cutting Social Security is especially off-base since the latest projections from the Congressional Budget Office show that the program is fully funded through the year 2038 with no changes whatsoever. Even after this date, the program would always be able to pay more than 80 percent of scheduled benefits. Given the overall health of the program, proposals for cuts are effectively taking away benefits that people have already paid for.

In addition to the fact that such cuts would be unnecessary and arguably unfair it also is worth noting that means-testing is an especially bad way to make cuts. While investment banker Peter Peterson likes to go around the country boasting that he doesn’t need his Social Security, the reality is that there are very few rich elderly people like Mr. Peterson. In order to have any noticeable impact on the program’s finances, a means-test would have to hit very middle income people — people with incomes in the neighborhood of $40,000 a year.

Even then the impact would be very limited. To have a major impact on the program’s expenses it would probably be necessary to move the means-test down to people with incomes around $30,000 a year. This would not fit most people’s definition of rich.

The proposal to raise the age of Medicare eligibility is also incredibly misguided. It is extremely expensive for seniors to get health care insurance. Many workers struggle to stay on jobs until age 65 when they can first qualify for Medicare. This proposal would push the bar out two years. Those who lose their jobs or can’t find jobs will generally not be able to afford insurance, which could easily exceed $20,000 a year for those with even minor pre-existing conditions.

Rather than looking to reduce benefits the more obvious way to go with Medicare is to reduce the cost of care. The United States pays more than twice as much per person for its health care as the average for other wealthy countries. If we could get our costs down to those of other countries we would be facing huge long-run budget surpluses, not deficits. One way to get lower costs would be to allow Medicare beneficiaries to buy into the more efficient health care systems in other countries. The enormous potential savings could be split between the government and the beneficiary.

It is perverse that the NYT thinks it is reasonable to have major cuts to programs that affect retirees or near retirees. These people were especially hard hit by the collapse of the housing bubble. Many of them saw most of their life’s savings disappear as their house price plummeted. Insofar as we need revenue (which we clearly do not now), the most obvious place would be to tax the people who profited most from the bubble, the Wall Street crew.

A tax on financial speculation could easily raise more than $100 billion a year. Congress could also instruct the Federal Reserve Board to hold onto the $3 trillion in assets that it has acquired as part of its quantitative easing program. This could save the government more than $100 billion a year in interest payments later in the decade. In short, it is not difficult to find money for people who are not afraid of going after the rich and powerful.

The NYT decided to have a special dialogue around a letter to the editor that called on President Obama to take “decisive action” on the economy. Remarkably, only one item on the list of decisive actions, investing in infrastructure, would have any positive impact on jobs and even this would be limited. While investing in infrastructure is a very good idea, there are not very many people who can be usefully employed on infrastructure projects in the next two years.

It takes time to plan a project and many projects, like building high speed rail, are only going to be built over many years. This means that even the most aggressive infrastructure program will only have a limited impact on jobs in the rest of 2011, 2012, and even 2013. If we want to see substantial reductions in unemployment over the next two years we will need more decisive action than this.

The rest of the items in the letter all involve reducing the deficit. While some of the proposals are very reasonable, like ending the war in Afghanistan and raising taxes on the wealthy, these will certainly not help create jobs. The list also contains two profoundly silly proposals, means-testing Social Security and raising the age of Medicare eligibility to 67.

The idea of cutting Social Security is especially off-base since the latest projections from the Congressional Budget Office show that the program is fully funded through the year 2038 with no changes whatsoever. Even after this date, the program would always be able to pay more than 80 percent of scheduled benefits. Given the overall health of the program, proposals for cuts are effectively taking away benefits that people have already paid for.

In addition to the fact that such cuts would be unnecessary and arguably unfair it also is worth noting that means-testing is an especially bad way to make cuts. While investment banker Peter Peterson likes to go around the country boasting that he doesn’t need his Social Security, the reality is that there are very few rich elderly people like Mr. Peterson. In order to have any noticeable impact on the program’s finances, a means-test would have to hit very middle income people — people with incomes in the neighborhood of $40,000 a year.

Even then the impact would be very limited. To have a major impact on the program’s expenses it would probably be necessary to move the means-test down to people with incomes around $30,000 a year. This would not fit most people’s definition of rich.

The proposal to raise the age of Medicare eligibility is also incredibly misguided. It is extremely expensive for seniors to get health care insurance. Many workers struggle to stay on jobs until age 65 when they can first qualify for Medicare. This proposal would push the bar out two years. Those who lose their jobs or can’t find jobs will generally not be able to afford insurance, which could easily exceed $20,000 a year for those with even minor pre-existing conditions.

Rather than looking to reduce benefits the more obvious way to go with Medicare is to reduce the cost of care. The United States pays more than twice as much per person for its health care as the average for other wealthy countries. If we could get our costs down to those of other countries we would be facing huge long-run budget surpluses, not deficits. One way to get lower costs would be to allow Medicare beneficiaries to buy into the more efficient health care systems in other countries. The enormous potential savings could be split between the government and the beneficiary.

It is perverse that the NYT thinks it is reasonable to have major cuts to programs that affect retirees or near retirees. These people were especially hard hit by the collapse of the housing bubble. Many of them saw most of their life’s savings disappear as their house price plummeted. Insofar as we need revenue (which we clearly do not now), the most obvious place would be to tax the people who profited most from the bubble, the Wall Street crew.

A tax on financial speculation could easily raise more than $100 billion a year. Congress could also instruct the Federal Reserve Board to hold onto the $3 trillion in assets that it has acquired as part of its quantitative easing program. This could save the government more than $100 billion a year in interest payments later in the decade. In short, it is not difficult to find money for people who are not afraid of going after the rich and powerful.

Read More Leer más Join the discussion Participa en la discusión

A front page piece in the NYT compared the current turmoil in financial markets with the situation in the fall of 2008. It referred to the 2008 crisis as being a subprime crisis. While subprime mortgages took the biggest hit, prime mortgages also defaulted at rates that were many times higher than expected.

The piece also said that the Federal Reserve Board is largely out of ammunition in terms of its ability to counter a crisis. This is not true. The Fed could take far more aggressive measures to counter the downturn. For example, it could target a longer-term interest, committing itself to keep the 5-year Treasury bond rate to 1.0 percent for the next year.

Also, it could target a higher rate of inflation (3-4 percent), a policy that Bernanke himself had advocated for Japan when he was still a professor at Princeton. This would reduce the real interest rate, giving firms more incentive to borrow and also reduce the indebtedness of homeowners as house prices would presumably rise in step with inflation.

It is irresponsible for the NYT to make unsupported assertions about the lack of Fed power. The Fed is one of the main tools for affecting the economy and it is wrong to tell readers that it cannot do anything.

A front page piece in the NYT compared the current turmoil in financial markets with the situation in the fall of 2008. It referred to the 2008 crisis as being a subprime crisis. While subprime mortgages took the biggest hit, prime mortgages also defaulted at rates that were many times higher than expected.

The piece also said that the Federal Reserve Board is largely out of ammunition in terms of its ability to counter a crisis. This is not true. The Fed could take far more aggressive measures to counter the downturn. For example, it could target a longer-term interest, committing itself to keep the 5-year Treasury bond rate to 1.0 percent for the next year.

Also, it could target a higher rate of inflation (3-4 percent), a policy that Bernanke himself had advocated for Japan when he was still a professor at Princeton. This would reduce the real interest rate, giving firms more incentive to borrow and also reduce the indebtedness of homeowners as house prices would presumably rise in step with inflation.

It is irresponsible for the NYT to make unsupported assertions about the lack of Fed power. The Fed is one of the main tools for affecting the economy and it is wrong to tell readers that it cannot do anything.

Read More Leer más Join the discussion Participa en la discusión

The NYT has a good editorial outlining the weak U.S. growth prospects, although the double-dip discussion is silly – we’re looking at too slow growth, not a double-dip. The piece makes another serious error at the end when it argues that Germany, like China, should reduce its trade surplus.

China and Germany are in fundamentally different positions in the world economy. China is an extremely fast growing developing country. It would be expected that China would have a large trade deficit. By contrast, Germany is a very slow growing wealth country with a stagnant or declining labor force. It should be expected that Germany would have a large trade surplus as it sends capital to countries where it can be better used.

The NYT has a good editorial outlining the weak U.S. growth prospects, although the double-dip discussion is silly – we’re looking at too slow growth, not a double-dip. The piece makes another serious error at the end when it argues that Germany, like China, should reduce its trade surplus.

China and Germany are in fundamentally different positions in the world economy. China is an extremely fast growing developing country. It would be expected that China would have a large trade deficit. By contrast, Germany is a very slow growing wealth country with a stagnant or declining labor force. It should be expected that Germany would have a large trade surplus as it sends capital to countries where it can be better used.

Read More Leer más Join the discussion Participa en la discusión

Time to beat up on really really bad news reporting. The stock market doesn’t tell people why it does what it does. We have commentators who bloviate on what they think caused the market to rise or fall, but they don’t really know and they could be completely wrong.

That is why it was incredibly irresponsible for NPR to tell listeners in its top of the hour news segment that the market plunged because Standard and Poor’s downgrade of U.S. debt. NPR does not know this to be true and it certainly is not obviously the case.

The market that should have been most immediately affected by the S&P downgrade was the U.S. bond market. However bond prices soared in the trading immediately following the downgrade and continued to rise through Wednesday. If there was greater fear that the U.S. would default because of the downgrade, then bond prices should have plunged as investors demanded a higher risk premium. This did not happen.

The most obvious alternative explanation for the plunge in the market is the risk that the euro could break up as the debt crisis spread from relatively small countries like Greece and Ireland, to the euro zone giants, Spain and Italy. The prospect of a euro zone break-up raises a real risk of a Lehman-type freeze up of the world financial system. It is far more plausible that this prospect led to the plunge in the stock market than the downgrade by one of three major credit rating agencies.

This point is important because many political actors, including National Public Radio, are trying to use the debt downgrade as an argument for cutting Social Security and Medicare. Their argument will be furthered if they can claim that the downgrade had enormous consequences for the stock market, since so many people involved in political debates (i.e. columnists, policy wonks, reporters, congressional staffers) have substantial amounts of money invested in the stock market.

Time to beat up on really really bad news reporting. The stock market doesn’t tell people why it does what it does. We have commentators who bloviate on what they think caused the market to rise or fall, but they don’t really know and they could be completely wrong.

That is why it was incredibly irresponsible for NPR to tell listeners in its top of the hour news segment that the market plunged because Standard and Poor’s downgrade of U.S. debt. NPR does not know this to be true and it certainly is not obviously the case.

The market that should have been most immediately affected by the S&P downgrade was the U.S. bond market. However bond prices soared in the trading immediately following the downgrade and continued to rise through Wednesday. If there was greater fear that the U.S. would default because of the downgrade, then bond prices should have plunged as investors demanded a higher risk premium. This did not happen.

The most obvious alternative explanation for the plunge in the market is the risk that the euro could break up as the debt crisis spread from relatively small countries like Greece and Ireland, to the euro zone giants, Spain and Italy. The prospect of a euro zone break-up raises a real risk of a Lehman-type freeze up of the world financial system. It is far more plausible that this prospect led to the plunge in the stock market than the downgrade by one of three major credit rating agencies.

This point is important because many political actors, including National Public Radio, are trying to use the debt downgrade as an argument for cutting Social Security and Medicare. Their argument will be furthered if they can claim that the downgrade had enormous consequences for the stock market, since so many people involved in political debates (i.e. columnists, policy wonks, reporters, congressional staffers) have substantial amounts of money invested in the stock market.

Read More Leer más Join the discussion Participa en la discusión