July 26, 2011

July 26, 2011 (Housing Market Monitor)

By Dean Baker

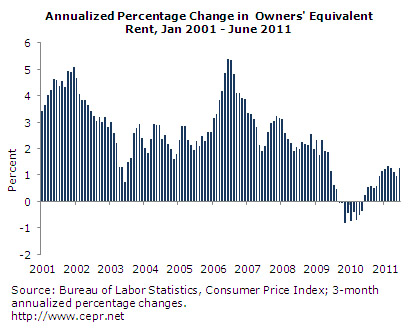

Rents are showing little sign of acceleration.

The Case-Shiller 20-City index rose by 1.0 percent in May, the second consecutive increase after eight months of decline. Seventeen of the 20 cities showed increases in May, with only Tampa Bay, Las Vegas, and Detroit showing declines.

The biggest increases were in Washington, D.C., Minneapolis, and Boston, with price rises of 2.4 percent, 2.6 percent, and 2.7 percent, respectively. The jump in Minneapolis is the most surprising since prices had been falling sharply in the city. However, this raises the possibility that the increase is simply a result of quirks in measurement. Prices fell by 16.8 percent from July of 2010 until March of this year. If this decline was overstated, then it would be expected that the data would now be showing increases.

The pattern of rising prices in Washington, D.C. continued. Prices have now risen at a 10.7 percent annual rate over the last three months and are up 1.3 percent over the last year. It is the only one of the 20 cities in the index with a year-over-year price increase.

Prices in Las Vegas declined 0.9 percent. They have declined at a 10.5 percent rate over the quarter and are now down 6.6 percent over the last year. With nominal prices in the city down to the December, 1998 level, this is a clear case where the bubble has deflated and prices are now overshooting on the downside.

In Tampa, where prices fell 0.6 percent in May and are now down 9.5 percent year-over-year, it is likely that the bubble still has room left to deflate. Prices in real terms are still about 10 percent above their mid-90s level. Prices in Detroit are reflecting the city’s depopulation. Nominal prices in the city have fallen back to their May, 1993 level. To put this in perspective, the Consumer Price Index has risen by more than 50 percent over this period.

The explanation for the sudden turnaround in prices is not obvious. Prices for homes in the bottom tier still seem to be showing the effect of the ending of the first-time buyers tax credit. For example, in Minneapolis, prices for homes in the bottom tier rose by just 1.3 percent. They have fallen at a 30 percent annual rate over the last three months, compared with a 4.9 percent decline for the market as a whole. There is a similar story in Chicago where prices for homes in the bottom tier rose 0.4 percent in May, compared with 1.7 percent for the city as a whole. Over the last quarter, prices for homes in the bottom tier fell at a 42.6 percent rate compared with a 4.3 percent rate for the market as a whole. However, there are several cities where the bottom-tier prices are rising as fast or faster than the rest of the market, indicating that the effect of pulling purchases forward may come to an end soon.

One possible explanation for the strengthening of prices is that the pace of foreclosures has slowed somewhat in recent months. This would translate into a decrease in supply, which could be having a positive effect on prices.

It is interesting to note that both the new and existing home sales data also have shown increases in prices in June. Both series are highly erratic, so monthly movements generally have little meaning, but they are consistent with the strengthening of the market shown in the Case-Shiller data.

The Census Department will release data on vacancy rates later this week, which will give us more information on the overall state of supply and demand in the housing market. The recent movement in rents provides no reason for believing that there is any underlying tightening of the market. Owners’ equivalent rent is rising at just over a 1.0 percent annual rate. (This series differs from some realtors’ series showing rising rents, because it measures changes in rent for the same units over time. It does not compare the rent of different units.) This is up compared with the declining rents of 2010, but there is no clear upward momentum. It is likely that oversupply will exert further downward pressure on prices.