July 07, 2021

During the COVID-19 pandemic, declining consumer confidence in the economy, which continued to contract as late as November and December of 2020, played a significant role in leading to the economic recession. Concerns about the health of the economy in the future can have drastic impacts on the economy today.

When households are faced with the potential for looming wage cuts or layoffs, new income for those not living paycheck-to-paycheck may be saved for a rainy day rather than spent. This is known as “precautionary saving,” which occurred in many countries during the Great Recession. This higher propensity to save rather than consume can slow the path to economic recovery, and in some instances, they can deepen a recession, especially if the future is uncertain.

At the same time, during times of crisis (e.g., bouts of high unemployment), households that face more significant financial strains often will increase their spending in order to meet their economic needs (e.g., paying for food and rent), boosting the fiscal multiplier, i.e., the effect of direct fiscal spending.

When Congress was debating the contents of the second Coronavirus Aid, Relief, and Economic Security (CARES) Act, one of the most contentious items was the provision of an additional round of “stimulus checks” or economic security cash payments to individuals and households on the basis of their income.

Congress was able to eventually negotiate a bipartisan bill, but the effort to appease deficit hawks came at the expense of larger stimulus payments. In the end, the bill included stimulus checks to the tune of $600, which began to taper off for individuals making more than $75,000 and phased out completely for individuals with incomes over $87,000. Heads of household earning less than $112,500 also qualified for $600, which phased out completely for those earning more than $124,500, and among married couples filing jointly, those earning up to $150,000 received $600 each, tapering out at an upper limit of $174,000.

This analysis uses data collected in two-week intervals between October 28, 2020 and May 10, 2021 by the US Census Bureau’s Household Pulse Survey. Our sample narrowed the survey down to include households and adults over 25 (born before 1996) across the United States. We analyze the changes in consumer sentiment — based on spending changes due to economic concerns or lack thereof — over the course of this period. This analysis particularly focuses on December 2020, when the second round of fiscal stimulus was passed (including $600 stimulus checks) as well as March 2021, when the American Recovery Plan (including $1,400 stimulus checks) was announced. The HPS Survey asks whether or not someone identifies as being “of Hispanic, Latino, or Spanish origin.” For purposes of this analysis, those self-identifying as being of Hispanic, Latino, or Spanish origin are identified as Hispanic in the results.

Self-reported spending changes — likely spending decreases — due to economic concerns, dip in the weeks following the passage of economic stimulus bills, both at the end of December 2020 and in mid-March 2021. While there is insufficient data to demonstrate a causal relationship between the provision of stimulus checks and a change in concern-related spending changes, the data supports the argument that fiscal stimulus spending had a meaningful impact on economic sentiment among households and individuals.

An effective economic recovery from the pandemic is dependent on the economic confidence of individuals and households. This analysis indicates that previous government support, in the forms of extended unemployment benefits, stimulus checks, and other fiscal spending, likely played a role in rebuilding Americans’ economic confidence.

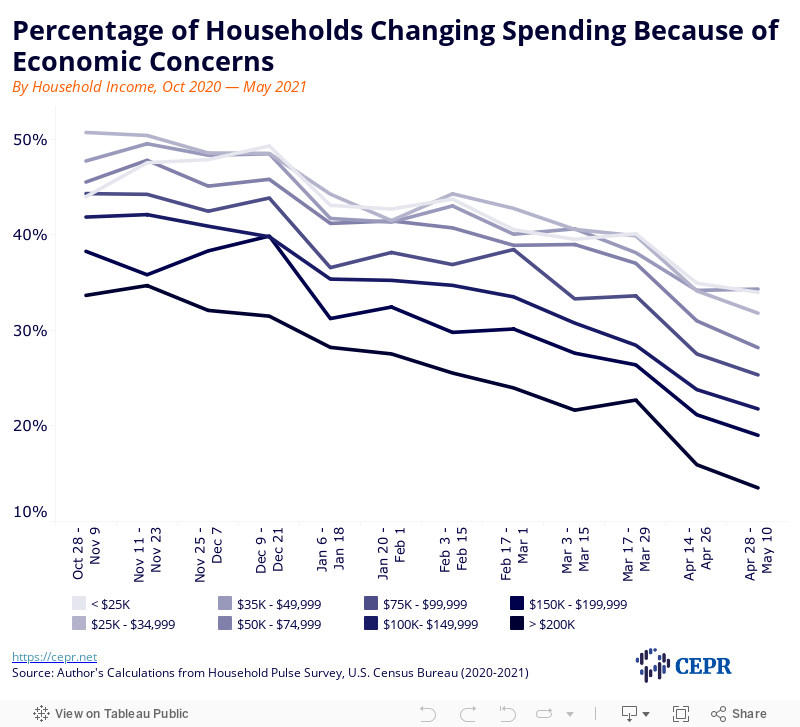

Figure 1

Between the end of 2020 (December 19–21) and the beginning of 2021 (January 6–18), the percentage of households that reported a change in spending due to “concerns about the economy” fell across the board for all income groups, as seen in Figure 1, above.

In part, shifting sentiments about the economy could be attributed to the transition to a Biden presidency. While the inauguration had not yet occurred during this decline in economic concerns, the new year signaled that health, economic, and policy changes were likely on the horizon — an indicator that helped assuage some people’s fears about a further receding economy. This time period also roughly coincided with the Food and Drug Administration’s emergency authorizations of the Pfizer and Moderna COVID-19 vaccines.

Across the different income groups, households earning between $150,000 and $199,999 actually experienced the greatest decline in spending changes due to economic fears. In late December 2020, nearly 40.0 percent of households in this group changed spending due to economic concerns, but by the beginning of January, this number had fallen to 31.2 percent.

In addition, this period between the end of December and the beginning of January coincided with the passage of the second round of economic security payments ($600 stimulus checks) as well as other economic protections including a continuation of supplemental unemployment benefits.

The second largest decrease in spending during this time period was for households earning between $75,000 and $99,999, many of which directly benefited from stimulus payments. The proportion of households changing their spending habits due to economic concerns among this group fell from 43.9 percent to 36.6 percent between the end of December and the beginning of January for a 7.3 percentage point decrease.

Households earning less than $25,000 and between $25,000 and $34,999 reported declines of 6.2 and 4.3 percentage points, respectively, while households with incomes between $35,000 and $49,999 and between $50,000 and $74,999 experienced respective decreases of 6.8 and 4.6 percentage points during the same period.

For these low- and middle-income households, fiscal stimulus spending — including direct cash payments to households and individuals, supplemental unemployment insurance, and assistance to renters — helped buoy consumer sentiment, reassuring families that economic support would be provided, to some extent, by the government. These payments and programs, coupled with the promise of additional support, namely President Biden’s pledge of additional checks to the tune of $2,000 (or $1,400 payments in addition to the existing $600), helped assuage some of the economic concerns held by households. These $1,400 payments eventually arrived in March 2021. In doing so, such government relief packages convinced fewer households to change spending due to economic concerns.

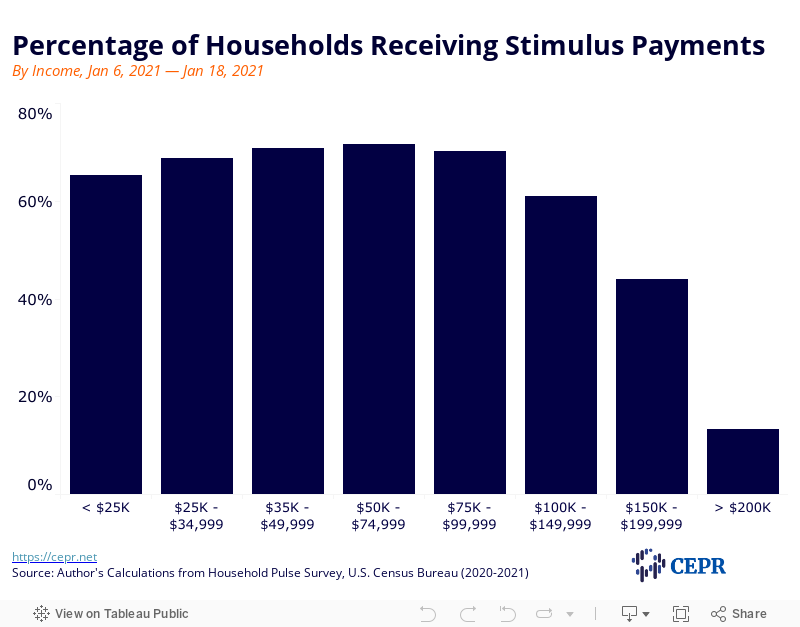

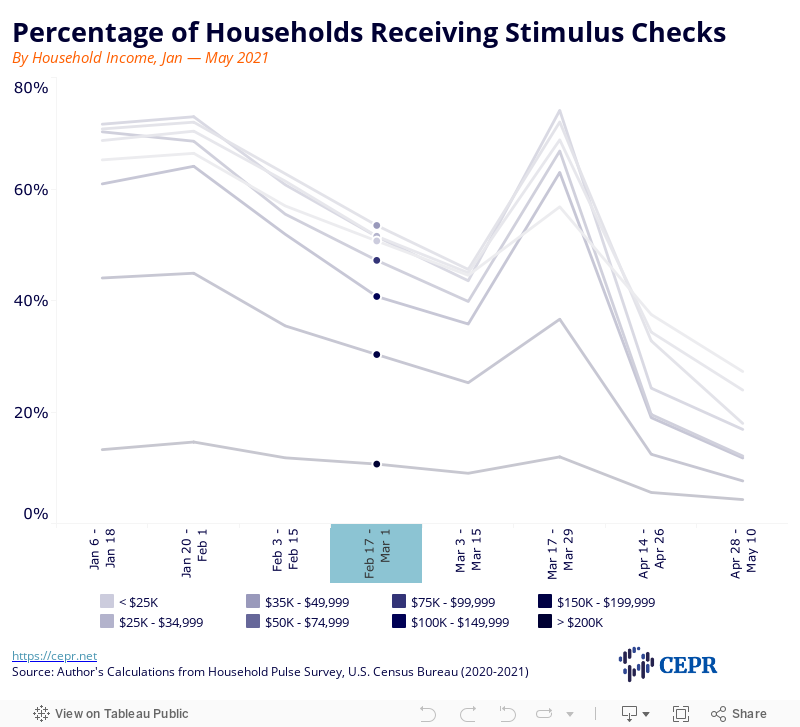

Meanwhile, households earning between $150,000 and $199,999 received stimulus payments at consistently lower rates than households with lower incomes, as seen in Figure 2.

Figure 2

In the first two weeks of January 2021, only 44.0 percent of these households reported receiving a stimulus check. As shown in Figure 3, households with incomes between $50,000 and $74,999 reported the highest rate (71.6 percent) of receiving the economic impact payments. Also, only 60.0 percent of lower-income households earning less than $25,000 received the payments, likely due to obstacles barring them from accessing the payments. Among these households, many were unable to access the checks due to a lack of stable housing or a permanent address, intermittent access to internet, and most importantly, many of these households were not required to file taxes in the prior year, which made it more difficult for them to receive the payments.

Figure 3

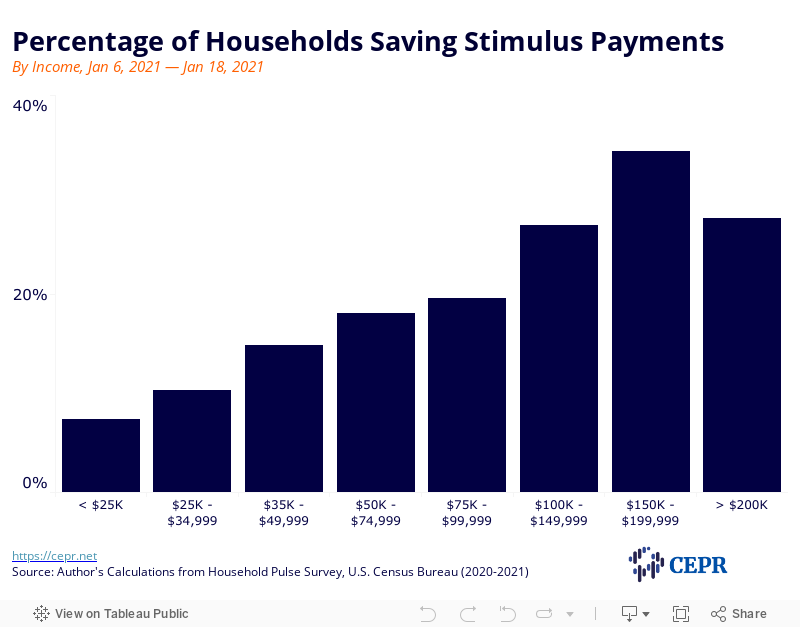

Despite the lower rates of stimulus receival among households earning between $150,000 and $199,999, they experienced the largest decline in spending changes attributable to economic concerns, which can, in part, be explained by their increased ability to save.

Families with higher incomes are better able to weather the financial and economic effects of the COVID-19 recession, and they have more disposable income to save while still fulfilling their spending needs on food, housing, and other essential goods and services. Because of this, these households were better situated to save throughout 2020 in case of further economic downturn.

Figure 4

In 2021, during the weeks between January 6–18, out of the households that received stimulus checks (up to $600), households with incomes between $150,000 through $199,999 reported the highest rates (34.4 percent) of saving the economic stimulus payments, compared to only 13.6 percent of households earning less than $25,000, as seen in Figure 4.

In addition, households with lower incomes may face credit constraints as well as economic barriers to saving, despite the possibility of job loss or wage cuts in the future. In other words, the sizable changes in the percentage of households adjusting spending due to economic concerns among families earning between $150,000 and $199,999 seen in Figure 1 is partially due to the flexibility with which they can choose to save or spend.

Figure 5

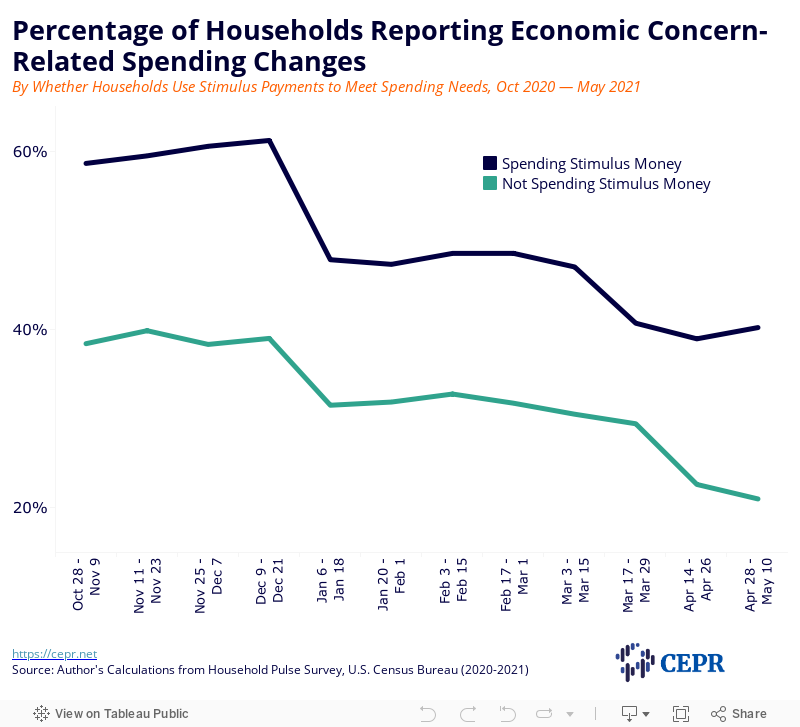

While it is not possible to wholly isolate the effect of stimulus payments alone, it is possible to assess the change in economic concerns for households that are using stimulus payments to meet their spending needs.

Figure 5 shows that throughout the period from the end of October 2020 to the end of March 2021, the most drastic decline in household concerns about the economy came at the turn of the new year between the periods of December 9–21 and January 6–18, which coincides with the passage of the $600 stimulus checks. The proportion of households not using stimulus payments to meet spending needs that expressed concerns fell by 7.5 percentage points, from 39.0 percent to 31.5 percent.

The decline among households that were using stimulus payments, however, was nearly double this amount. There was a 13.4 percentage point decrease (to 47.8 percent) in the percentage of stimulus-using households that reported economic concerns as a motivation for spending changes during this same period from between December 9–21 to between January 6–18 when the $600 checks were being sent out.

While this measure is an imperfect estimator, it illustrates that households relying on the stimulus checks, on average, experience higher overall rates of economic concern. At the same time, they experienced a more substantial decline in economic concerns around the time the second stimulus checks were approved at the end of the year.

Later in 2021, between the periods of March 3–15 and March 17–29, 6.3 percent of households (Figure 5) using stimulus payments to meet their spending needs reported a subsequent decrease in economic concerns, coinciding with the passage of the American Rescue Plan (ARP), which was signed on March 11, 2021, and the distribution of the $1,400 stimulus checks. During the same two periods, only 1.1 percent of households that were not using stimulus checks to meet their spending needs reported a change in spending due to economic concerns.

Like with the drastic changes around the new year, the March 2021 decline in economic concerns for families relying on stimulus payments likely is not attributable entirely to the effect of the $1,400 alone, but rather to a confluence of the various factors, including some components of the ARP such as support for state and local governments, extension of unemployment benefits, and additional rental and housing assistance. Nevertheless, it appears that vulnerable households — that is, those using stimulus payments — were noticeably convinced by the passage of the bill that “help was on the way.”

Figure 6

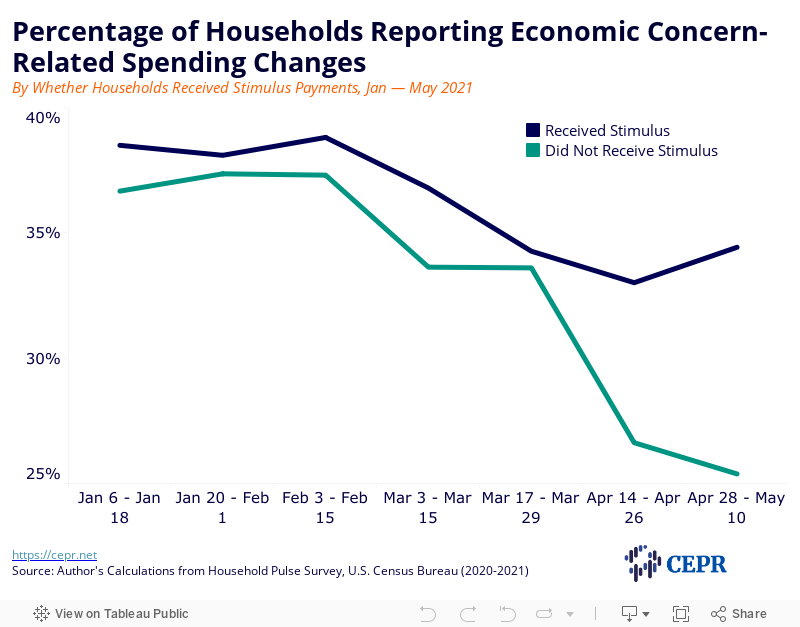

Starting in 2021, the Household Pulse Survey began asking households directly about whether or not they received economic impact payments (EIP), also known as stimulus payments. As such, it is not possible to discern any change in percentage of households adjusting spending due to economic concerns from before the $600 stimulus checks went out (in the last week of December 2021 and early weeks of January 2021) and afterwards.

It is, however, possible to look at the period in 2021 between the weeks of March 3–15 and March 17–29, in Figure 6, when the American Rescue Plan was passed and $1,400 checks began to be distributed.

Between these two periods in March 2021 when the ARP was passed, the percentage of households that received the $1,400 payments reporting economic concern-related spending changes decreased by 2.5 percentage points (to 34.2 percent) compared to no change among households not receiving stimulus checks.

Figure 7

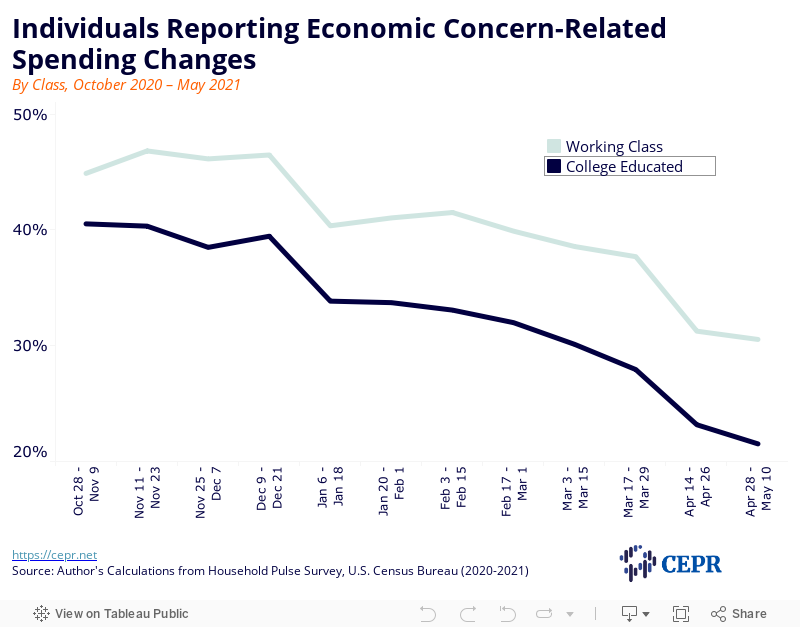

Figure 7 shows that working-class individuals — represented as people who have not completed a Bachelor’s degree — reported a slightly larger decline (compared to non-working-class individuals) in economic concern-driven spending changes of 6.1 percentage points between the period of December 9–21 and the period of January 6–18 when the $600 checks were being sent out (among other provisions in the end-of-year stimulus package). People with at least a Bachelor’s degree experienced a 5.6 percentage point decrease during the same period. Working-class individuals also consistently reported receiving stimulus payments at higher rates compared to their non-working-class counterparts, most likely due to a higher rate of eligibility.

That being said, a confluence of factors including the stimulus provisions — as well as the upcoming Biden inauguration and the FDA approval of vaccines — coincided with a significant dip in economic fears among both working-class and college educated people.

Still, working-class people consistently reported economic concern-related spending changes at higher rates than college educated workers. From December 9–21, 46.4 percent of working-class people reported such spending changes as opposed to 39.5 percent of college educated individuals.

In 2021, from April 28–May 10, there continued to be a 9.0 percentage point gap between college educated people (21.5 percent) and working-class people (30.5 percent) who cited economic concerns as a reason for their spending changes. This captures how, despite across-the-board declines in spending changes attributable to economic concerns, working-class individuals have felt (and continue to feel) the effects of the pandemic-induced recession more than their college educated counterparts.

In part, this is attributable to the fact that working-class people are often afforded less economic and job security, for instance, in short-term gig work or hourly-based wage work. In addition, working-class individuals employed in the service industry — including hospitality, leisure, and retail sectors — have reduced access to jobs conducive to remote work. Because of this, these laborers often experienced the brunt of pandemic-related job cuts and layoffs.

Figure 8

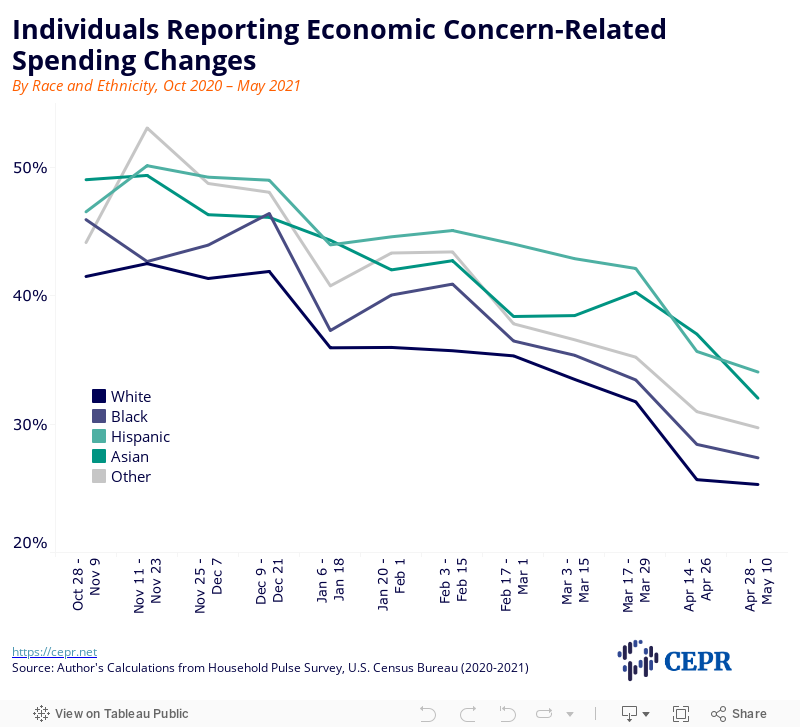

As with income groupings, individuals grouped by race and ethnicity reported decreases across the board when it came to spending changes attributable to economic concerns between the end of December 2020 and the beginning of January 2021, as seen in Figure 8. In particular, the percentage of Black survey respondents who reported spending changes due to economic concerns fell by 9.1 percentage points from 46.4 percent to 37.3 percent, the largest effect among racial groups. The fraction of white individuals and Hispanic individuals fell by 6.0 and 5.0 percentage points, respectively. Asian respondents experienced the smallest change, a 1.8 percentage point decrease.

Around the time of the American Rescue Plan in March 2021, many Americans similarly reported another, slightly smaller, decline in spending changes attributable to economic concerns. From the period in 2021 between March 3–15 to the period between March 17–29, the percentage of Black people who reported economic concerns fell 1.9 percentage points to 33.4 percent. White and Hispanic individuals experienced declines of 1.7 percentage points (to 31.7 percent), and 0.7 percentage points (to 42.1 percent) During this period, Asian respondents were the only group to report a higher incidence of spending changes due to economic concerns, an increase of 1.8 percentage points to 40.3 percent.

Figure 9

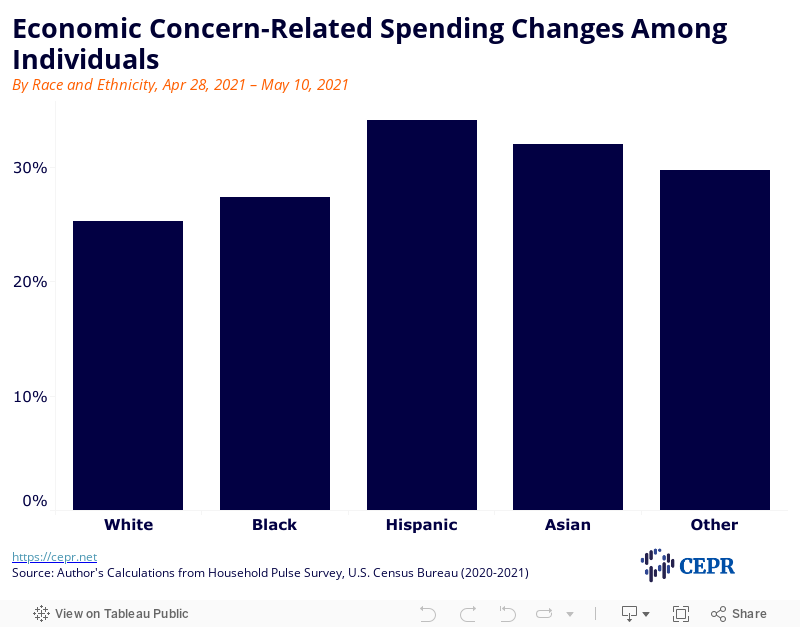

In addition, white survey respondents consistently reported the lowest rates of spending changes related to economic concerns. Figure 9 reveals that during the weeks between April 28 and May 10, 25.3 percent of white respondents reported such changes followed by 27.4 percent of Black respondents. During the same period, Asian and Hispanicindividuals reported significantly higher rates of 32.0 percent and 34.1 percent, respectively.

Figure 10

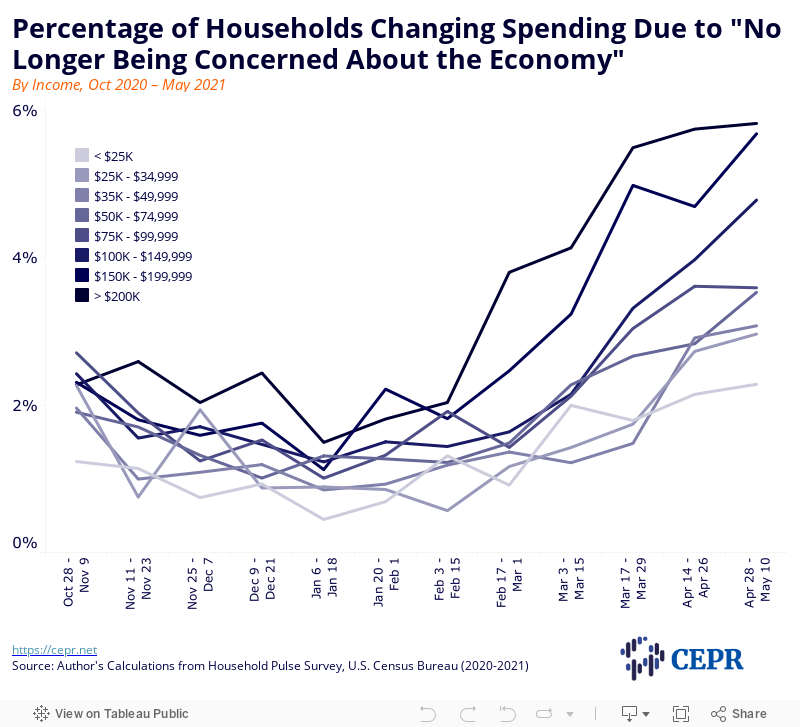

In addition to reports of economic concern, measures of economic optimism are also important in signalling a successful path to recovery. In particular, Figure 10 compares the percentage of households reporting spending changes while citing that they are “no longer feeling concerned about the economy.” This, in itself, is a variable of change and a proxy for recovery, representing the proportion of people who are changing their spending habits — likely increased spending — due to mitigated concerns.

Here, changes from period to period are significantly smaller compared to measures of economic concerns; this is likely attributable to the sentiment among many individuals and households that “we are out of the woods yet.”

Optimism about the economy, however, seems to be concentrated in the echelons of higher income households. Roughly 5.8 percent of households earning more than $200,000 reported spending changes due to no longer being concerned about the economy during the weeks in 2021 between April 28 and May 10, compared to a rate of 1.5 percent in the same year during the period of January 6–18, a 4.3 percentage point increase. Similarly, 5.7 percent of families earning between $150,000 and $199,999 reported the same between April 28 and May 28, a 4.6 percentage point increase.

Meanwhile, the proportion of households with incomes below $25,000 that reported such economic optimism grew by only 1.8 percentage points (to 2.3 percent). This change was only slightly greater for families earning between $25,000 and $34,999 and between $35,000 and $49,999, who experienced a rise of 2.0 (to 3.0 percent) and 2.2 (to 3.1 percent) percentage points, respectively.

Low-income households have been and continue to be the most economically vulnerable to the effects of the pandemic-induced recession. Oftentimes, these households are made up of workers in low-paying hourly jobs, which provide less job security and fewer benefits, rather than higher-paying salaried jobs with benefits. In addition, they report higher rates of job loss and reduced hours. While growing demand for labor and improving vaccination rates have driven some optimism for a path to economic recovery in 2021, few households, especially those with lower incomes, report economic optimism as a motivator behind spending changes.

Figure 11

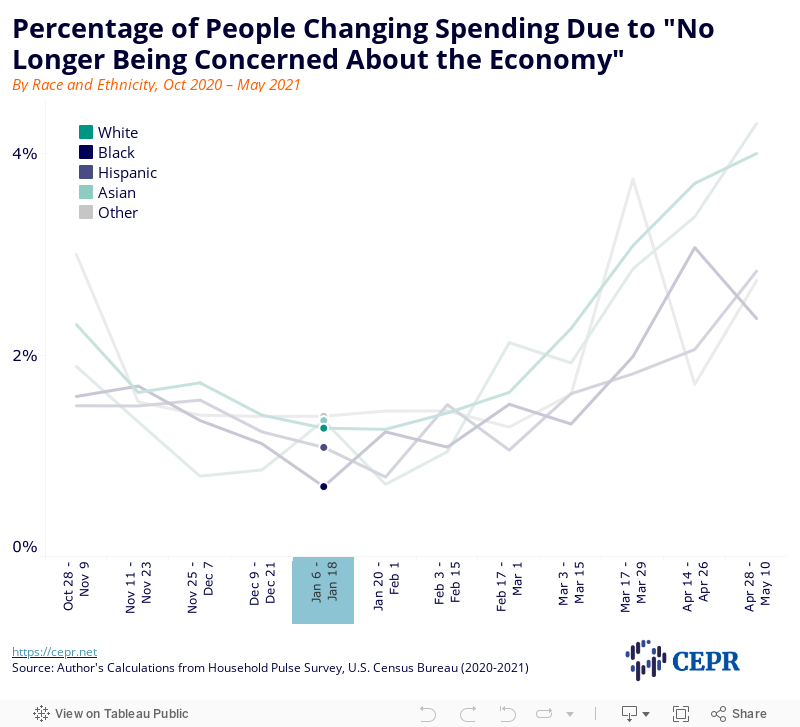

Similar to income group categorizations, stratifications on the basis of race and ethnicity in Figure 11 also show that gains in spending changes due to economic optimism is largely concentrated among white and Asian respondents. By the weeks of April 28 through May 10, 4.0 percent and 4.3 percent of white and Asian respondents, respectively, reported changing their spending due to no longer being concerned about the economy. Meanwhile, Black and Hispanic individuals reported such changes at lower rates of 2.4 percent and 2.8 percent, respectively.

While there is some evidence of a “U-shaped” recovery, the effects seem to largely be among high-income households as well as white and Asian people. Meanwhile, the proportion of low-income households, Black people, and Hispanic people reporting any spending changes due to mitigated economic concerns seems largely consistent with levels in October and November 2020, prior to Biden’s election and the provision of a viable COVID-19 vaccine.

Moving ahead, an equitable recovery requires addressing the economic concerns of all Americans, especially families and individuals that have been most drastically harmed by the effects of the pandemic and its subsequent recession. A successful recovery is not one that solely benefits high-income households and white individuals. Rather, a successful recovery is an equitable, fair recovery.

Acknowledgements: The author thanks Hayley Brown, Simran Kalkat, and Sarah Rawlins for contributing to research, analysis, and data visualization.