GDP Falls at a 0.9 Percent Rate, Driven by Slower Inventory Growth and Falling Housing Construction

Recession-fearing households increased spending on hotels and restaurants at a 13.5 percent annual rate in Q2.

GDP declined at a 0.9 percent annual rate in the second quarter, as a slower pace of inventory accumulation subtracted 2.01 percentage points from the quarter’s growth. A 14.0 percent rate of decline in residential construction subtracted 0.71 percentage points from GDP growth. Final sales of domestic products to domestic purchasers fell at a 0.3 percent rate, after rising at a 2.0 percent rate in the first quarter.

Even with Slower Growth, Inventories Still Accumulated at a Healthy Pace

Inventories still rose at a $81.6 billion annual rate, somewhat faster than pre-pandemic normal. This was nonetheless a drag on growth, since they grew at a $188.5 billion rate in the first quarter. This healthy rate of accumulation is a positive going forward, since it means stores are, for the most part, well-stocked after the pandemic supply chain problems. This will put downward pressure on prices.

Farm inventories are an exception. They fell at a $44.6 billion annual rate, continuing a downward trend that has been in place since the third quarter of 2015.

Consumption Grew at a Modest 1.0 Percent Rate, as the Switch Back to Services Continues

Consumption of services rose at a 4.1 percent annual rate in the second quarter, while consumption of goods fell at a 4.4 percent rate. Goods consumption as a share of nominal spending is still 3.6 percent higher than its pre-pandemic share, with service spending down by the same amount. The goods share in real terms is 3.2 percentage points higher, with services down by 2.4 percentage points (real shares won’t sum to 100 percent).

Spending on a wide range of goods is still considerably higher than its pre-pandemic level. The biggest drop in nominal shares on the service side are in health care services, down 1.4 percentage points, recreational services down 0.6 percentage points, housing down 0.5 percentage points, and transportation services (much of this is commuting) down 0.4 percentage points.

The Saving Rate is Holding Up

The inflation hawks have been raising the alarm that people are spending down pandemic savings, leading to an overheated economy. They cite the reported saving rate, which was 5.2 percent in the second quarter, down from an average 7.5 percent in the three years preceding the pandemic.

This is misleading. Saving was lower in the last two quarters because tax payments have risen. Since there was not an increase in tax rates in 2022, this is presumably because people are paying capital gains taxes on recent stock sales.

The sum of savings plus taxes as a share of personal income was 18.9 percent in the second quarter. This is higher than the 18.5 percent figure in 2018 and the 18.7 percent share in 2019.

In short, there is no story of excessive levels of consumption overheating the economy. On the other side, hotel and restaurant spending rose at a 13.5 percent annual rate in the second quarter. This is not consistent with the widely expressed recession fears reported by the media.

Inflation Slows Sharply in Quarter

Inflation, as measured by the core Personal Consumption Expenditures (PCE) deflator (the Fed’s main inflation gauge), fell to a 4.4 percent annual rate in the second quarter from a 5.2 percent rate in the first quarter. This is still considerably higher than the Fed’s target of a 2.0 percent average rate, but it should help to alleviate concerns of a 1970s-type wage-price spiral. While it is just a single quarter’s data — and these numbers have been especially erratic in the pandemic — the pace of inflation looks to be slowing rather than increasing.

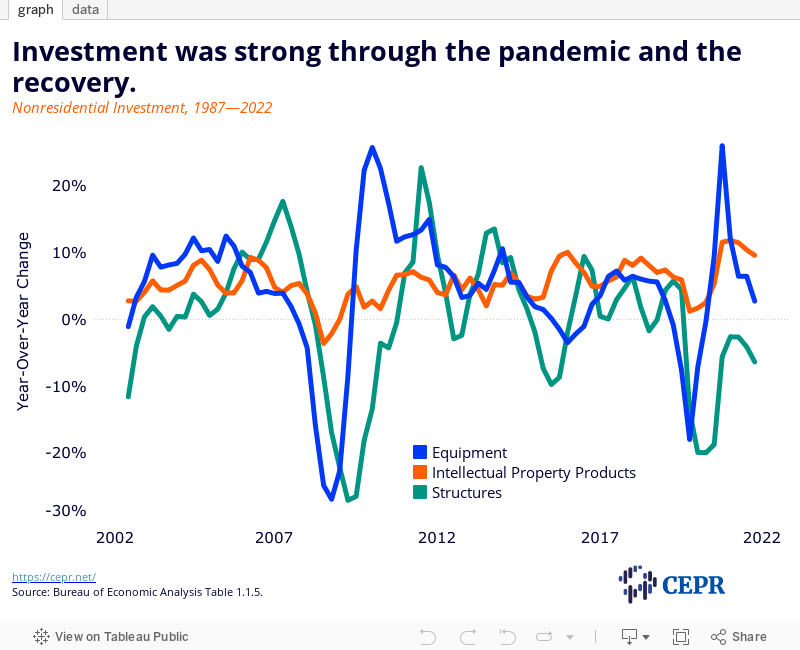

Investment Remains Healthy

Nonresidential investment fell at a 0.1 percent annual rate in the quarter, driven mostly by an 11.7 percent rate of decline in structure investment. Structure investment has been falling sharply throughout the pandemic and recovery as there is less need for office space and traditional retail space. It was 24.7 percent below its pre-pandemic level in the second quarter.

Investment in intellectual products remains solid, rising at 9.2 percent rate in the quarter, putting it 20.0 percent above its level in the fourth quarter of 2019. Equipment investment fell at a 2.7 percent rate, but is still 9.0 percent higher than in the fourth quarter of 2019.

Residential Investment Falls Sharply

The drop in housing was largely expected and pretty much what the Fed presumably wanted to see as a result of its interest rate hikes. The sharp rise in mortgage interest rates took the air out of an incipient housing bubble, with sales falling sharply.

The higher rates have also led to a drop in construction, which is unfortunate since the country needs more housing. However, residential construction was still 9.9 percent above its pre-pandemic level in the quarter. It is also important to remember that fees associated with mortgage issuance are included in this category of spending. Mortgage refinancing has largely disappeared in the last two months, with applications down close to 80 percent from year-ago levels.

Slowing Nondefense Federal Spending is Drag on Quarter’s Growth

Nondefense federal spending fell at a 10.5 percent annual rate in the second quarter, slowing the quarter’s growth by 0.3 percentage points. State and local government spending also declined at a 1.2 percent rate, knocking 0.13 percentage points off growth.

Net Exports Were a Big Boost to Growth in the Quarter

An 18.0 percent rise in exports, coupled with a much slower 3.1 percent rise in imports, caused trade to add 1.43 percentage points to second quarter growth. We are not likely to see similar gains in future quarters, as weaker growth in our trading partners is likely to diminish demand for US exports.

On the Whole, This is a Positive Report

The modest drop in GDP reported for the quarter is not good news, but it was hardly a surprise. It also was entirely due to inventory quirks, which will not be repeated in future quarters. Consumption is still growing at a respectable pace, as is investment.

The Fed has been raising interest rates ostensibly out of concern that the economy was growing too fast, causing inflation. This report should help to stem those fears. While people are apparently not so concerned about a recession to keep themselves from taking trips and going to restaurants, they are still not spending down their pandemic savings. The sharp drop in the inflation rate reported in the core PCE deflator should also alleviate concerns about a wage-price spiral.

CEPR produces same-day analyses of government data on inflation, employment, GDP and other topics. Follow @DeanBaker13 on Twitter to get his quick-take analysis of government data immediately upon release.