December 18, 2013

The effects of fiscal policy on growth and employment are central to the debate on deficit reduction and stimulus. Unfortunately, there are sharp divisions among economists over the size of fiscal multipliers.

A major problem is identifying deliberate changes in fiscal policy, since the size of the budget deficit is in large part dependent on the state of the economy. Therefore it is necessary to find a way to distinguish between changes in the deficit that are the result of cyclical fluctuations and changes that are attributable to conscious policy.

Several identification schemes have been used to resolve the issue of endogeneity regarding the business cycle in fiscal multiplier estimations, among them a measure of the cyclically adjusted budget deficit, the cyclically adjusted primary balance (CAPB) in event studies (Alesina and Ardagna 2010), as well as the recursive approach (Fatás and Mihov 2001) and the one by Blanchard and Perotti (2002) in structural vector autoregressive (SVAR) models. However, adjusting for business cycle movements may not be enough in the presence of pronounced asset and credit market movements that influence the budget and GDP over and above what is generally recognized as business cycle swings.

For example, surges in stock market prices in the United States in the 1990s or housing prices in the last decade, can have a substantial impact on lowering deficits beyond what would be predicted in a standard cyclical adjustment. This would lead a measure of fiscal policy that relied on the CAPB to overstate the size of the fiscal tightening policy in the upswing of a bubble and to overstate the size of the fiscal expansion in the period when a bubble deflates. This measurement could lead to a bias toward underestimating the impact of fiscal stimulus in standard models.

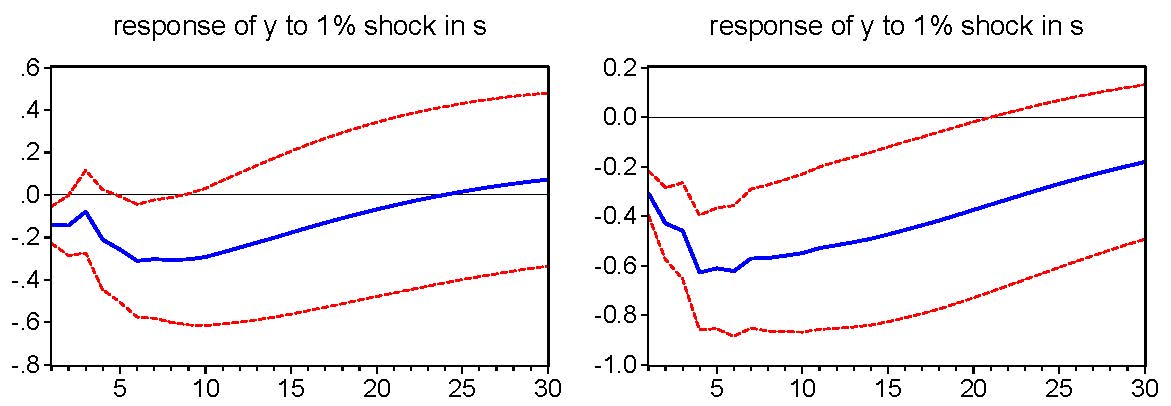

A new study by Gechert and Mentges (2013) finds evidence for US data supporting the hypothesis of Guajardo et al. (2011), who argue that the CAPB is a biased measure of the actual fiscal stance and leads to downward biased estimations of fiscal multipliers. They use the CAPB in a recursive VAR and add the private wealth-to-debt ratio as an additional variable to account for financial market swings. They find multipliers more than twice as high, as without the additional variable. Figure 1 compares the impulse response functions of the VAR without the private wealth-to-debt ratio (on the left) and with the additional variable (on the right). The figures display the impact of a reduction in the budget deficit equal to 1 percent of GDP. This contraction has a far more negative impact on GDP when accounting for asset and credit market swings.

Figure 1

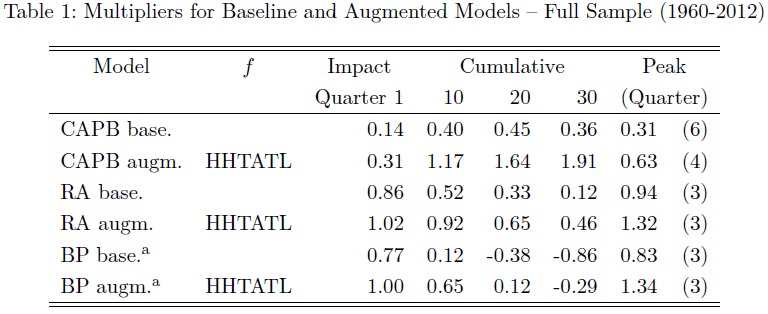

They observed similar results for government spending shocks. Table 1 shows the results for the different approaches, comparing multipliers in baseline models and augmented models where RA is the recursive approach and BP the one based on Blanchard and Perotti (2002).

These findings are robust to alternative specifications. They imply that deficit reduction is more likely to be contractionary and could be more harmful to growth than expected from the results of some of the existing literature. The argument of Gechert and Mentges complements another empirical finding (Batini, Callegari and Melina 2012) according to which austerity is more harmful in a depressed economy, where monetary policy is up against the zero lower bound giving the central bank less ability to counteract the impact of deficit reduction.

Alesina, A. and S. Ardagna (2010). Large changes in fiscal policy: taxes versus spending. NBER/Tax Policy & the Economy 24 (1), 35–68.

Batini, N., G. Callegari, and G. Melina (2012). Successful Austerity in the United States, Europe and Japan. IMF Working Paper WP/12/190.

Blanchard, O. and R. Perotti (2002). An Empirical Characterization of the Dynamic Effects of Changes in Government Spending and Taxes on Output. Quarterly Journal of Economics, 117 (4), 1329–1368.

Fatás, A. and I. Mihov (2001). The Effects of Fiscal Policy on Consumption and Employment: Theory and Evidence. CEPR Discussion Papers 2760.

Gechert, S. and R. Mentges (2013). What Drives Fiscal Multipliers? The Role of Private Wealth and Debt. IMK Working Paper 117.

Guajardo, J., D. Leigh, and A. Pescatori (2011). Expansionary Austerity: New International Evidence. IMF Working Paper WP/11/158.