August 31, 2010

August 31, 2010 (Housing Market Monitor)

By Dean Baker

Lower home sales will likely knock 0.6 percentage points off third quarter GDP growth.

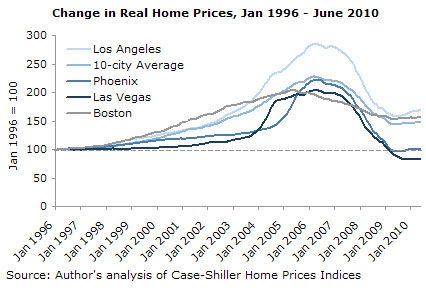

The Case-Shiller 20-City index rose by 1.0 percent in June, bringing its annual rate of increase over the last three months to 13.6 percent. Prices rose in 18 of the 20 cities, with Las Vegas as the only city with a price decline of the second consecutive month. Prices in Phoenix were flat.

The biggest price increases this time were all in Midwest cities, with Minneapolis, Detroit and Chicago all showing gains of 2.5 percent. This is the third consecutive month of sharply rising prices in Minneapolis. Prices have risen at a 32.7 percent annual rate over the last quarter and are now 10.7 percent above levels a year ago. Price increases in Chicago and Detroit have been more modest over the last three months, rising at 18.5 percent and 14.7 percent annual rates, respectively. Prices in both cities are virtually unchanged from levels a year ago.

Washington, DC and Atlanta were also big gainers last month with 1.7 percent price increases. Over the last three months, prices have risen at a 25.7 percent annual rate in Washington and a 25.3 percent annual rate in Atlanta. Prices in Washington are up 7.3 percent from year-ago levels, while they are up by just 2.0 percent in Atlanta.

It is clear that this rise in prices was driven by the homebuyers tax credit since so much of the increase in prices occurred in the bottom third of the housing market. For example, in Seattle, prices in the bottom tier rose at a 16.0 percent rate over the last three months, while prices in the middle and top tiers rose at 5.1 percent and 8.2 percent rates, respectively. In Portland, prices in the bottom tier rose at a 23.2 percent annual rate over the quarter, while prices overall rose at a 15.0 percent rate.

In New York, prices for homes in the bottom tier rose at an 18.6 percent annual rate compared to an 8.6 percent rate overall over the last three months. In Boston, prices for homes in the bottom tier increased at a 30.3 percent rate, while prices overall rose at an 18.1 percent rate.

The largest effect of the tax credit would be expected at the bottom end of the market both because the credit is a larger portion of the house prices and also because first-time buyers who benefit from the credit will disproportionately be buying lower-end homes.

This is important to recognize in making future predictions on house prices. As noted previously, home sales plunged immediately after the end of the tax credit. This was first noticeable in May, as the Mortgage Bankers Association’s purchase mortgage application index fell through the floor. The drop was also reflected in the 32.7 percent drop in May new home sales that the Commerce Department reported in June. Somehow, the drop in July in existing home sales (which were mostly contracted in May) caught housing analysts by surprise.

However, the effect of this plunge in sales on prices should be clear. With the demand side of the market having largely collapsed with the end of the tax credit, it is virtually certain that prices will resume their decline, completing the deflation of the bubble. While the bubble has fully deflated in some cities such as Las Vegas and Phoenix, it still has a considerable way to go in others like New York and Los Angeles. In the 20-City index, we can still expect a further decline of 15-20 percent.

The weakness in the housing market in the second half of 2010 will be another source of drag on the economy. The housing sector added almost 0.6 percentage points to GDP growth in the second quarter, most of which was due to the fees associated with home sales. It is likely to subtract as least this much from growth in the third quarter, given the decline in house sales this quarter.

More importantly, the further decline in house prices will destroy any illusions that homeowners had about house prices returning to their bubble-inflated peaks. The negative wealth effect should lead homeowners to further curtail consumption, bringing saving rates back towards their historic average of 8.0 percent, if not higher due to the country’s skewed demographics.