January 31, 2012

January 31, 2012 (Housing Market Monitor)

By Dean Baker

Those taking advantage of the first-time buyers credit in Atlanta might have lost more than $50,000.

The seasonally adjusted Case-Shiller 20-City index fell 0.7 percent in November, its seventh consecutive monthly decline. The index has now fallen in 17 of the last 18 months. The rate of price decline appears to be accelerating modestly in recent months, with prices dropping at a 7.9 percent annual rate over the last three months compared to a 3.7 percent decline over the last year.

The price declines were broadly based with only Phoenix, Minneapolis, and Denver bucking the downward trend. Some of the sharpest price declines were in West Coast cities where the bubbles have not yet fully deflated. Los Angeles, Portland, and San Francisco saw price declines of 0.9 percent, 1.1 percent and 1.3 percent, respectively. Over the last three months, prices in these cities have dropped at respective annual rates of 11.0 percent, 3.1 percent and 8.9 percent. All three cities have seen sharper price declines over the last year than the 20-City index as a whole.

Other cities with large price declines in November include Atlanta, with a 1.2 percent drop; Detroit, with a 1.3 percent decline; and Chicago, with a 2.1 percent drop. Each of these cities has a very different story. Atlanta’s price decline was driven in large part by a collapse at the bottom end of the market. Prices for homes in the bottom third of the market have fallen by 50 percent since the end of 2009.

This is clearly a story in which the first-time buyers tax credit had a substantial impact. House prices had been falling sharply for homes in the bottom tier in 2008 and in the first months of 2009, then they turned around and began to rise. Once the credit ended in 2010, they began to fall sharply. This path could imply a story where the credit put $8,000 in the pocket of someone who bought a home at the end of 2009 for $120,000. Today that home would be worth a bit less than $60,000, implying a loss of more than $60,000 on the house price. There are similar stories in other cities, albeit not quite as dramatic.

Chicago looks to be one of the bubble cities where prices are destined to over-correct. At its peak in March of 2007, inflation-adjusted house prices in Chicago had risen by almost 50 percent from their 1996 level. With the November data, inflation-adjusted prices are 12.1 percent below their 1996 level and in real terms just 59.2 percent of their bubble peak.

The decline in Detroit is likely an anomaly. Its prices had cratered in late 2010 and have mostly been rising in the last year.

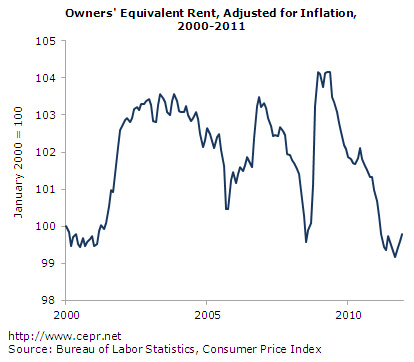

It is interesting to compare the path of house prices with the owners’ equivalent rent (OER) index in the CPI to get an assessment of underlying conditions in the housing market. (OER excludes utilities and therefore provides a better comparison than the rental index with sales prices as a measure of the value of housing.) The real value of this index largely peaked with a 4 percent rise in 2002. It then remained flat through the peak bubble years and has since fallen back to its pre-bubble level. This suggests that there is zero evidence of any upward pressure on prices coming from the rental segment of the market as some have claimed.

This is consistent with the vacancy data. While there is some drift downward from the record vacancy rates in 2010, the vacancy rate in the fourth quarter was still higher than any recorded level in the pre-bubble years.

There is little reason to expect that house prices will stop their decline any time soon, the best path would be a slowing of the rate of decline with prices perhaps leveling off by the end of 2012. There is still likely considerably air in the bubbles in several markets. There is nothing that should be done to prevent them from deflating. However, it would be desirable to see prices stabilize and possibly rise somewhat in markets where the bubble has fully deflated and the market is overshooting on the down side.