August 10, 2018

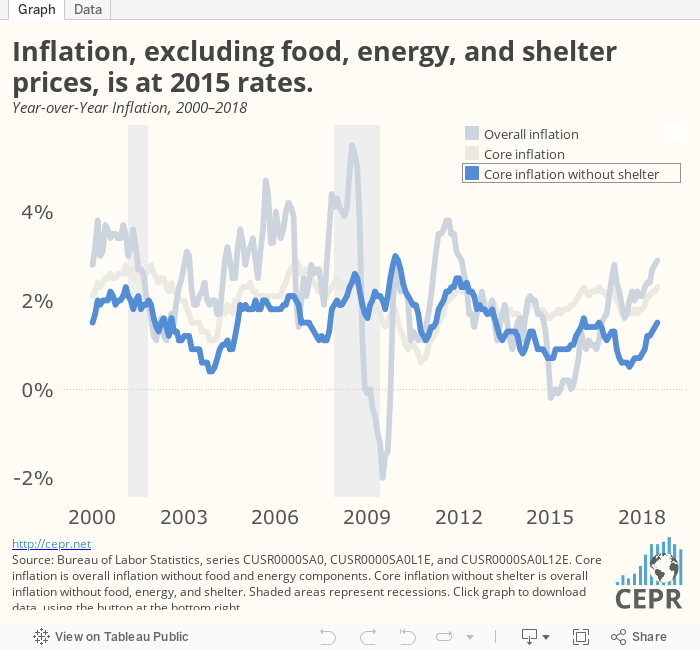

Over the last year, the overall CPI has risen 2.9 percent. The core CPI has risen 2.4 percent, while a core index that excludes shelter has risen just 1.5 percent. For more, check out the latest Prices Byte.

August 10, 2018

Over the last year, the overall CPI has risen 2.9 percent. The core CPI has risen 2.4 percent, while a core index that excludes shelter has risen just 1.5 percent. For more, check out the latest Prices Byte.