May 12, 2020

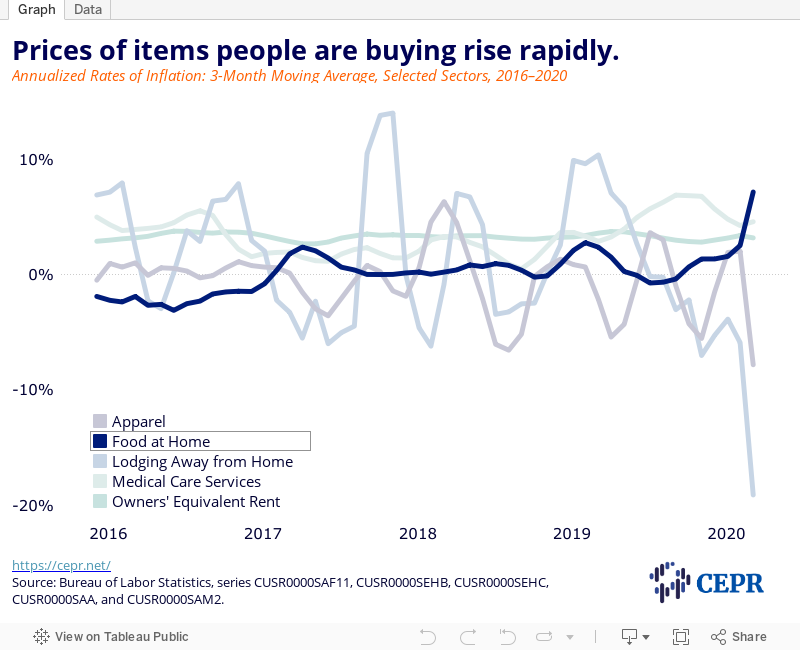

Food prices rose 2.6 percent in April, reflecting a large increase in store-bought food.

The overall Consumer Price Index (CPI) fell 0.8 percent in April, driven again by large price declines in sectors that were hit hard by pandemic-related shutdowns. Gas prices fell 20.6 percent, following a drop of 10.5 percent in March. They are now 32.0 percent below their year-ago level. Apparel prices had an extraordinary 4.7 percent decline, following a drop of 2.0 percent in March. Prices are now 5.7 percent below year-ago levels.

There were also huge declines in hotel prices and airfares, with the former dropping 8.1 percent and the latter dropping 15.2 percent. These April declines followed March price declines of 7.7 percent and 12.6 percent, respectively. These sharp price declines led to a drop of 0.4 percent in the core CPI, following a decline of 0.1 percent in March. This was the largest drop in the core CPI on record.

Much of the story in this report, as in the March report, is that we are seeing sharp declines in the price of items that people are not buying, while the prices of many of the items people are buying are rising rapidly. Because the CPI is a fixed-weight index, the impact on the index of drops in the price of items such as hotels, restaurants, and airfares is not affected by the fact that demand for these items is down by more than 50 percent from the pre-crisis level.

The most important item with a sharp increase in price is food purchased at home, for which prices increased 2.6 percent in April, following a 0.5 percent increase in March. The price of medical care services rose 0.5 percent in April, the same as its March increase. Prices are now up 5.8 percent over the last year.

There was a drop in the rate of inflation for both rent proper and owners’ equivalent rent with both showing 0.2 percent increases for the month, well below the pace of their respective 3.5 and 3.1 percent rises over the last year. (The slowing was even sharper if we remove the rounding, getting April increases of .196 percent and .175 percent, respectively.) This indicates that landlords are asking for lower rents to keep units occupied.

As we move forward, it will be interesting to see how rents may change across cities. One of the almost certain lasting effects of the pandemic will be an increased amount of telecommuting. Since it is as easy to telecommute from a place with low housing costs as a congested metropolitan area with high housing costs, we may see sharp reductions in rents in some of the high-priced cities.

In this respect, it is worth noting that the index for owners’ equivalent rent in San Francisco fell by 0.7 percent in April. While this could be the beginning of sharp declines in rent in the Bay area, this index is highly erratic (it rose 0.6 percent in February), so we definitely need more data before attaching much significance to this price drop.

In other areas, the price of new vehicles was flat in April after dropping 0.4 percent in March. The index is down by 0.6 percent from the year-ago level. Used car prices fell 0.4 percent, after rising 0.8 percent in March. There is clearly no free fall in car prices for now.

The college tuition index rose 0.2 percent in April, the same as in March, while tuition at technical schools rose 0.7 percent, following a 0.2 percent rise in March. This is perhaps a harbinger of a shift in demand.

The index for food away from home rose just 0.1 percent in April after rising 0.2 percent in March. Both increases lagged the much sharper rise in food purchased at home, reflecting the plunge in demand for restaurant meals.

The overall inflation picture from this report is confusing since it hugely overstates the importance of price declines in items that almost no one is buying, such as airplane tickets and hotel rooms. We are likely to see the reverse of this story as the economy starts to reopen this month and next. Restaurants, hotels, and airplanes are likely to be seeing much higher costs due to the measures necessary to limit the spread of the coronavirus. This means that they will be driving the overall CPI higher. This is not inflation that should concern the Fed, but we need not have any fears of a deflationary spiral.